BPI has now released its final results for the year ended 2015.

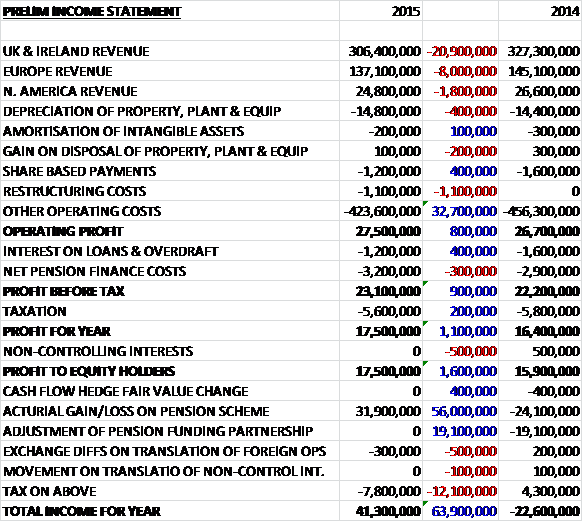

Revenues declined when compared to 2014, reflecting lower average polymer costs for the year and the impact of currency translation on the European sales with a £20.9M fall in UK & Ireland revenue, an £8M decrease in Europe revenue and a £1.8M fall in North America revenue. Depreciation increased by £400K but this was offset by a £400K decline in share based payments and we also see £1.1M-worth of restructuring costs but other operating expenses fell by £32.7M to give an operating profit £800K above that of last year. Bank interest on loans fell by £400K reflecting the favourable borrowing terms negotiated last year but this was offset by a £300K increase in net pension finance costs and after a modest decline in tax, the profit for the year came in at £17.5M, a growth of £1.6M year on year.

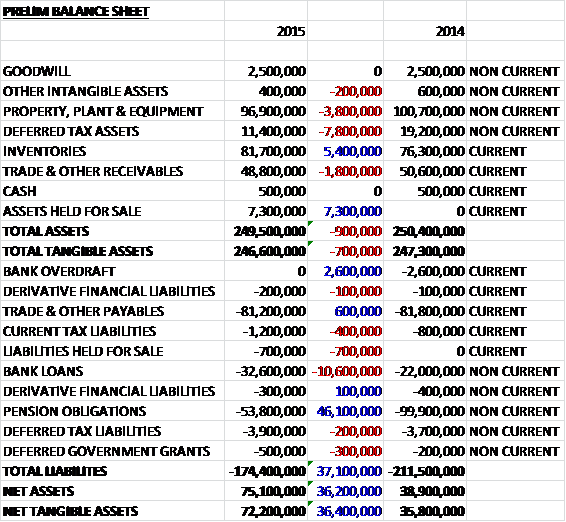

When compared to the end point of last year, total assets declined by £900K driven by a £7.8M fall in deferred tax assets relating to the reduction in the pension deficit, a £3.8M decrease in property, plant & equipment and a £1.8M decline in receivables, partially offset by a £7.3M growth in assets held for sale relating to the Chinese subsidiary, and a £5.4M increase in inventories. Total liabilities also declined during the year as a £46.1M fall in pension obligations relating to the change in inflation index, and a £2.6M decrease in the bank overdraft was partially offset by a £10.6M increase in bank loans. The end result is a net tangible asset level of £72.2M, a growth of £36.4M year on year.

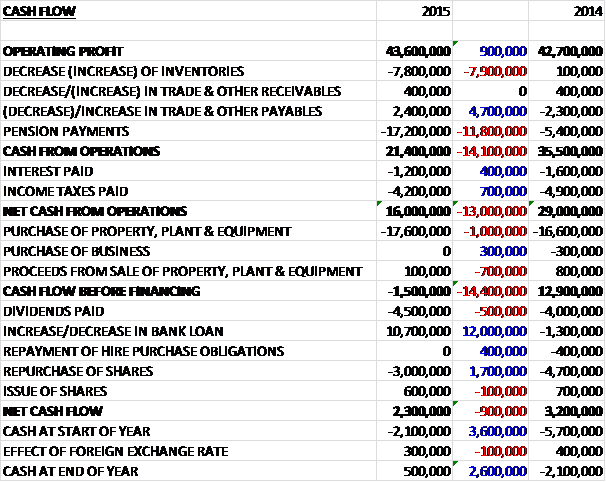

Before movements in working capital, cash profits increased by £900K to £43.6M but there was a sizeable growth in inventories and an £11.8M increase in pension payments which meant that after both interest and tax declined modestly, the net cash from operations was £16M, a decline of £13M year on year. This did not cover the £17.5M of capex (which is expected to remain broadly similar next year) so that before financing there was a cash outflow of £1.5M. The group also paid out £4.5M in dividends and spent £3M on their own shares and after a £10.7M increase in the bank loan there was a cash flow of £2.3M for the year and a cash level of £500K at the year-end.

Total volumes reduced by about 1% to 272,000 tonnes, reflecting reduced demand from certain sectors in the UK, including the loss of an unprofitable contract to supply refuse sacks to a major retailer. Within these numbers, the group saw an increase in demand for silage stretchwrap of just over 2%.

The operating profit in the UK and Ireland was £11.6M, a growth of £400K year on year as a result of a strong performance from the recycling operations. The operating profit in Mainland Europe was £15.7M, a decline of £600K when compared to last year, reflecting the impact of turbulent raw material costs in the first half of the year and detrimental movements in foreign exchange. The operating profit in North America was £1.3M compared to a loss of £800K in 2014 as previously reported difficulties with plant installation were rectified.

In October the group sold their Promopack reprographic business at Henor to Reprographic Systems for £200K as it has failed to make a return for a number of years. Also, in November they announced the closure of a stretchfilm plant in Widnes with the transfer of production to a larger plant in Leominster; and they reduced numbers employed at WMB, the consumer facility at Worcester and in the films business in Sevenoaks in order to align staffing levels against current demand at these locations. These actions resulted in a restructuring charge of £1.1M this year and should enhance future profits by around £500K.

During the year the company agreed with the trustees of the pension scheme to change the index used to revalue pensions in payment from RPI to CPI. This resulted in a reduction in the present value of scheme liabilities of £27.6M and to increase the security of pensions for scheme members (and no doubt to get the agreement of the trustees) the group also made a one off payment of £11.2M into the scheme.

A continuing problem for the group is the price of polymer, the main raw material. Polymer costs increased by some 50% between early March and the end of June, the greatest short term increase that the industry has ever seen. This had an impact on short term margins in the summer and although polymer prices have eased back, they remain 20% above their position in last February. Middle East polymer producers continue to favour Far East markets, partly as a result of duty when importing products into Europe and extra capacity in North America has not yet come on stream. The board believe that European polymer producers may be able to take advantage of the current market position, particularly if there are any further plant outages so it sounds as if the raw material pressures are not yet over.

After the year-end, the group signed an agreement to sell its Chinese subsidiary to Amcor Investment, an Australian based packaging group. The disposal is expected to complete in Q2 2016. The consideration is estimated to be about £9.4M with an estimated £6.4M upon completion with the balance payable in instalments following the agreement of working capital and satisfaction of certain post completion arrangements, all of which are expected to take place within the next year. The proceeds will be used to reduce borrowings. The estimated gain on disposal will be about £4M reflecting property and forex gains and this year the business made a small loss.

Going forward, 2016 has started well and the group’s investment programme in new plant, and action taken to bring facilities in line with demand are both designed to assist improved operating performance. They also expect continued success in supplying agricultural film markets. In addition, the recent weakness of sterling should enhance results through translation of the overseas earnings and improving the competitiveness of the UK business. The board continue to review a number of acquisition opportunities in the UK and mainland Europe but it remains to be seen whether they can bring any of these to conclusion. The board are confident that 2016 will deliver further progress.

At the current share price the shares are trading on a PE ratio of 11.3 which falls to 9.8 on next year’s consensus forecast. After a 12.5% increase in the annual dividend, the shares are now yielding 2.5% which increases to 2.6% on next year’s forecast.

Overall then, this year seems to have been a solid one for the group. Profits increased and net assets improved considerably due to the changes made to the pension scheme. The operating cash flow did fall but this was due to the increased cash payment into the pension scheme and an increase in inventories with cash profits increasing year on year. The group didn’t generate any free cash, however, mainly as a result of the pension payment.

The UK business performed well due to a strong performance from the recycling operations, and the North American business returned to profit as last year’s difficulties with the plant installation were rectified. Profits fell in Europe, however, due to the issued with polymer raw material and the weak Euro, both of which have partially been rectified so far this year. The polymer situation remains a cause for concern, however, as it sounds as though some volatility will remain this year.

With a forward PE of 9.8 and a dividend yield of 2.6% these shares look pretty good value to me, polymer issues and sluggish top line growth notwithstanding, and the recent weakness in sterling can only be good for the group going forward. I am tempted to take a position here.

BPI have released their annual report which gives a much more detailed account of how the year has gone operationally so I have revisited the shares.

Passing through the polymer price increased was challenging and the group’s margins were squeezed. Prices of the raw material eased between August and October but rose again in the final two months of the year. Euro prices reduced in January and February in Europe and the outlook for prices in the year should be downward but the supply position remains very tight. The same level of reduction was nor seen in the UK due to the recent weakness in Sterling. North America also saw reductions in January and February but prices still remain too high in relation to feedstock costs and Far Eastern prices.

Significant capacity additions have been approved in North America on the back of a plentiful supply of shale gas but this capacity is unlikely to arrive before 2017 and will result in North America becoming a significant exporter of polymer.

Lower oil and gas prices resulted in reduced energy costs in Belgium, Holland and Canada but while the UK wholesale electricity costs reduced reflecting the lower oil and gas prices, the group saw minimal benefit due to increasing energy taxes and environmental levies. The cost of manufactured tonne in the UK remains significantly higher than in the group’s European and Canadian operations but even the European prices put the group at a competitive disadvantage in global terms.

The European operating profit fell by £600K to £15.7M but in euro terms increased by €1.4M on volumes that were 4% ahead at 75,400 tonnes. The sales mix continued to improve and the business benefited from investment in new equipment and product development. Sales volumes saw growth in both silage and industrial products but margins were squeezed by the raw material price increases in Q2.

Total sales of silage products increased by 4.5% with reasonable growing conditions and low levels of carry-over stock in most markets. This increase arose against a background of cold but wet weather in Northern Europe and consistent hot and dry weather in Central Europe from April onwards resulting in lower volumes in the second half. Sales of the advanced silage products SilotitePro and Baletite increased by 14% with market feedback continuing to be positive. Sales of these products now account for over 22% of the total silage volumes and this is expected to increase each year. Baletite is a replacement for traditional round bale netting and SilotitePro is a new generation of silage film with improved economics and environmental properties and both will reinforce the group’s market leading position in silage wrap.

The significant polymer price increase in Q2 resulted in a very difficult pricing environment with margins suffering and falling below those of 2014. The reduction in polymer prices in early 2016 may delay the start of the new season and result in anther difficult year with further pressure on margins. Volume sales of printed film for the food industry grew by 9% with growth in both French Fries and vegetable markets. A new replacement printing press to replace two older units and enable greater production efficiencies and a small increase in capacity was installed in H2 and is running well.

Demand in pallet protection film and general purpose film remained reasonable despite some competitive pricing but sales of stretch hoods increased. Sales of Bontite, an industrial stretch product, again showed an increase as new legislation on load stability offered additional opportunities. At Roselare, total extrusion production was 20,000 tonnes with growth in all three of the group’s strategic products: stretch hoods, feedstock for printing and thinner insulation films. These products now account for 67% of production as sales volumes of the new thinner products for the insulation industry increased by 24% while stretch hoods were up 35%.

Sales from the industrial film plant in Hardenberg in Holland increased by over 7% and sales of other FFS products grew by 16% as they benefited from the installation late last year of a replacement eight colour printing press. Growth was achieved from the building, chemical and fertilizer sectors. Volumes of bags were maintained but customers do continue to move to FFS products. The board approved an upgrade of the extrusion equipment in their heavy duty factory at Hardenberg and the building work was completed and the first extruder installed. They have also authorised the installation of an additional extruder for FFS to meet growing demand in the petrochemical sector as they secure additional business.

Production fixed costs and labour costs per tonne improved with lower scrap and quality complaints. The European business remains well invested with clear strategic plans at each site which will enable further growth. Zele in Belgium will continue to focus on silage stretch products and printed film for the food industry. Roeselare in Belgium will focus on a reduced number of products, including stretch hoods, feedstock for printing and a range of pre-stretched thinner products for the insulation industry. Hardenberg in Holland is focused on industrial products and is a leading supplier of FFS to the petrochemical and other industries.

The business has achieved strong results for the last few years and with further investment in new capacity, combined with the development of new and improved products, should deliver similar or better returns in future years.

The operating profit in the UK and Ireland business was £11.6M, a growth of £400K year on year despite very challenging conditions due to the extreme volatility in polymer prices particularly in Q2 and the impact of sterling strengthening against the euro. The group also saw no relief from the very high energy costs despite lower oil and gas costs as taxes continued to increase.

Sales volumes reduced to 188,700 tonnes as the group exited some low margin retail refuse sack business and saw reduced demand in a number of sectors. Total sales to the more resilient sectors reduced slightly to 67% of the total due to lower demand arising from the competitive pressures in the retail food sector.

Sales of collation shrinkwrap, which are mainly to the food and drink industries, reduced marginally in 2015, despite volume from some new customers, as demand remained flat and the soft drink sector faced difficult trading conditions. Converter volumes improved despite demand being patchy as the group were successful in winning new customers but downgauging continued, restricting growth in volumes. Intra-group sales were down reflecting lower demand from some of the food retailers and their suppliers. Margins suffered from the polymer price increases in Q2, however. The group have strengthened their sales team to focus on delivering volume growth.

The group’s sites continue to operate efficiently with a focus on reducing scrap and operating costs. Their plan to upgrade new extrusion lines at Bromborough has continued with three coextrusion lines now fully operational and performing well with good outputs and gauge profiles, and a five-layer coextrusion line has been ordered for delivery in early 2016. These new lines will increase coextrusion capacity, produce thinner films and offer customers tighter tolerances with improved performance. At Sevenoaks, the group began the process of transferring mono work to the lower cost site at Bromborough so they can focus on the high quality coextrusion market at Sevenoaks which resulted in a number of redundancies. The site at Winsford continued to perform well, although volumes were slightly below those of 2014.

External volume sales of silage stretchwrap were just below last year despite good growth in the UK and Norwegian markets. In the UK the group continue to position themselves as suppliers to the leading co-operatives and agricultural merchants. The Irish market remains the lowest priced in Europe and while the group focus on a restricted range of customers, their market share reduced on pricing pressure. Margins were lower due to the combination of resin price increases and adverse exchange rates. Sales of the prestretched Wrapsmart Ultra continue to grow and were 13% ahead of last year. Sales of cast industrial stretchwrap were lower than 2014 as it continues to be imported from the Middle East and Far East.

Widnes produced a range of blown machine reels and hand rolls for the packaging industry and, despite strong competition in the conversion sector and a continuing move to prestretch products, volumes increased by 16% as the group benefited from the rationalisation of the product range and secured additional customers. In November they announced the closure of the facility with production being moved to Leominster which will reduce their cost base and offer customers higher quality products.

At Leominster the programme of investment to upgrade older extrusion equipment and improve output and quality continued. Output at the site showed a small improvement and scrap was in line with last year. All conversion for Wrapsmart, including the machines acquired in 2014 from STC, was moved to a new hall at the end of 2014 which resulted in increased efficiency and lower scrap in 2014. A new multi-layer extrusion line was authorised for installation in Q1 2016. The building work has been completed and all equipment delivered with a target start date for production of April 2016. Labour and production costs remained well controlled on all sites.

Recycling remained a challenged with the continued lack of availability of clean waste scrap. Total recycling volumes were down on 2014 with washed volumes and dry recycling both reduced. The group have begun an investment programme based on a new generation of recycling equipment. The first new machine was delivered and installed in December 2014 and this has enabled the group to increase efficiencies and reduce maintenance, labour and energy costs. The machine is performing well and allowing them to access waste which they previously would have considered wash grade. The washing plant installed in 2013 to remove paper contamination from waste plastic, most of which was exported to the Far East, continues to perform well.

Availability of scrap continues to be a key issue and the group are now bringing in packaging scrap from Europe. Scrap prices reduced during the year as demand from the Far East lessened. The agricultural recycling volumes reduced to the poor availability of scrap in the UK and Ireland so the group continue to target alternative supplies in mainland Europe. A number of new start-up recycling facilities in the UK have now ceased trading but there remains strong competition for scrap from mainland Europe.

The group’s construction films experienced a slow start to the year and volumes were lower in 2015. The group did continue to target strong growth in their structural water proofing and gas protection range of products, however, and they were able to achieve good growth in market share and in a flat market, increased sales by 7%. Total tonnage of refuse sacks fell by 7% over 2014 as they exited some low margin business in the retail sector. Pressure on margins in all sectors remained intense and the group are required to continually develop new and improved products to remain competitive. In the healthcare sector, the group continued to supply a range of downgauged waste sacks to the NHS and secured additional apron business in the second half of the year. At the beginning of 2015, they secured refuse and clinical waste sacks from the Scottish Health Service, replacing an overseas supplier. Volumes to the local authority sector continued to reduce as councils move to wheelie bins or stop providing sacks.

Volumes reduced in the retail sector as the group exited a number of underperforming lines. Margin pressure remains intense but they continue to supply a number of the larger national food retailers and develop downgauged products. They intend to launch their own-branded Visqueen Ultimate product through both retailers and online platforms. The supply chain sector continues to perform well with good growth at some customers but the sector is highly competitive with intense margin pressure.

There was considerable focus at Heanor on operational improvements in production which resulted in lower scrap and manning levels. A first coextrusion line was installed in December 2014 and has enabled the group to offer an improved range of products. A second line has now been ordered for delivery in June. A new three lane bag machine has also been ordered to uprate their capacity on standard sizes and replace an old conversion machine.

The group’s industrial activities at Ardeer and Greenock saw volumes reduce due to lower demand from the construction and animal feed sectors. Construction volumes were down, reflecting low demand in the market at the start of the year and in the summer with a number of customers experiencing reduction in activity levels and then reducing stock levels. Volumes of the more complex printed cement sacks saw further growth in the year due to additional customer wins, including some export business and the board anticipates further growth as more packing lines are installed.

Sales volumes of compost sacks for consumer packaging for retail horticulture increased as the group secured more business from their existing customers. Volumes to the animal feed sector were down due to unseasonably mild winters at both ends of the year. Packaging volumes for furniture and carpets, industrial packaging and garment film for online retailers were broadly maintained. Pallet stretch hooding volumes were in line with 2014 but, as they secure new customers, volumes should grow in 2016.

The Ardeer site continues to improve its operational performance and is benefiting from the new extrusion investment for heavy duty sacks. These new lines have delivered higher outputs, improved film quality and reduced scrap and energy costs. The year further benefited from a third line which was installed during Q4 2014. Two further extrusion lines for other products were installed towards the end of the year and are running at anticipated outputs and will benefit the coming year. A replacement eight-colour printing press was installed in the second half of 2015 and is performing well. Greenock continued to perform well with lower scrap rates and reduced costs.

The small site at Flint is focused on products requiring hygiene accreditation and continued to perform well with steady volumes and improved efficiencies. The small trading operation in Norwich also continued to perform well despite lower sales.

The operational performance of the wide line at Ardeer continued to progress with improved utilisation. This line manufactures a range of agricultural and horticultural film products that are sold in the UK and certain European markets. Total volume sales showed a small increase over 2014 with growth in silage sheet in both the UK and Europe replacing reduced volumes to North America following the installation of the new line in Canada. A new seven layer wide line has been authorised to increase capacity and develop more advanced products. Horticultural sales improved with some growth in the UK and exports despite pressure from the weaker euro.

In the consumer sector, at Worcester, sales volumes reduced as the sector remained under pressure throughout the year due to the difficult trading conditions at the major supermarkets. Margin pressure remained intense as supermarkets and their suppliers attempted to continue to reduce costs. All this against a background of increasing raw material prices resulted in lower margins. A number of redundancies were made in December to align staff levels with demand. The business strategy remains to broaden the customer and product base and an experienced sales director was appointed to develop new markets and products. While success will not be immediate, the group are quoting a number of new customers and are confident in securing additional volume. A new fast changeover printing press has been ordered for delivery in March.

The plant in China manufactures aprons and a range of bags including refuse, swing and pedal, food and freezer. The group installed in 2014 further extrusion equipment and an additional eight colour printing press to increase capacity for the production of packaging for bread and fresh produce. Total volumes increased year on year with some growth in Wrapsmart, bread bags and healthcare products. Margins showed some recovery as raw material prices fell in the Far East. Progress on increasing sales to Oceania by supplying the bread and produce markets was slower than expected and led to the decision to sell the business following an approach.

It was a difficult year for Jordan Plastics as sales volumes reduced and margins were impacted by the strength of sterling for sales in to Ireland. The pre-press and plate making business provided artwork, origination and printing plates to group businesses and external customers. The business continued to suffer from flat demand and due to the need for reinvestment, it was sold in Q4.

The total capex in the UK business was more than £12M as the group invested to replace older equipment, increase efficiencies and reduce scrap and maintenance, energy and labour. New extrusion lines were installed at Bromborough, Ardeer and Heanor and a printing press at Ardeer. Planned expenditure for 2016 includes extrusion equipment for Bromborough, Ardeer and Heanor and a fast changeover printing press for Worcester. The UK business is now well positioned and will continue to see further operational improvements and will benefit from capex projects and the current weakening of sterling against the euro.

The North American business saw an operating profit of £1.3M compared to a loss of £800K last year with the new extrusion line in full production and running well with the loss last year attributable to delays and problems with the installation of the line. Total product sold fell, however, as the group withdrew from the manufacture of low margin overwintering film in the horticulture sector.

Sales in agricultural products were nearly 2% below last year as the business experienced offshore low cost competition at the start of the year, some drought conditions in certain areas and crop yields that were below average. Sales of horticultural products fell by 2.5M pounds as the group discontinued the manufacture of overwintering film and focussed on greenhouse films.

Polymer prices continued at high levels in the region despite low feedstock costs and this, combined with a strong US dollar, encouraged the import of lower priced material impacting on volumes and margins. The new extrusion line performed as expected with good running speeds and operating at lower scrap and cost levels. Unfortunately a number of power outages adversely impacted the running of the line, resulting in higher than expected scrap and maintenance costs but the line is now running well again at the start of 2016. They also installed a new rewinding line late in the year that will be operational for 2016.

The business was restored to profit in the year and they are now developing new agricultural and horticultural products on the new seven layer extrusion line which will bring benefits in future years. With supportive weather conditions, further progress should be made in the coming year.

The current economic outlook remains uncertain following the collapse in the oil price and outlook for the global economy. The recent weakness of sterling will be helpful, however. The group have taken action to eliminate loss-making units, reducing their cost base and moving the business towards more resilient and growing markets and the board look forward to 2016 with confidence.

Overall then, the main take-away from all of this is that most end markets seem to be a little difficult and the group’s margins are under pressure due to erratic polymer pricing with the high cost of electricity not helping in the UK. In Europe, silage products did well, although volumes were lower in the second half in this weather-dependent product. The business also performed well in its other product areas in the region.

In the UK and Ireland it is quite difficult to ascertain exactly where the decent performance came from with most of the group’s end markets struggling. The higher profit against lower sales suggests that the investments made in the plants are improving margins despite the raw material difficulties. The North American business returned to profit after the problems with the new extrusion line were (mostly) rectified, although here too the group’s markets seem to be struggling.

The group seems to be struggling to increase sales with instead profits coming from improvements in production efficiency and product mix so the business could be ex-growth. The depreciation in sterling no doubt helps, however, and the shares do look cheap. They could be worth a go for the dividend?

On the 27th April the group confirmed the completion of the sale of its Chinese subsidiary to Amcor for a total consideration of £9.7M and the initial consideration of £6.4M has now been received. The balance will be paid in instalments following the agreement of closing working capital and satisfaction of certain post completion arrangements. The working capital, estimated at £2M, is expected to be payable in June with instalments of £300K in H2 2016 and the final instalment of £1M payable in early 2017 with the proceeds being used to reduce borrowings. The gain on disposal is now estimated to be over £5M.

Also it was announced that the trading performance n Q1 has been strong and ahead of management expectations having benefited from lower energy costs and favourable currency translation effects. This all seems quite positive and now the furore around the results has died down I have decided to take a position here.

On the 10th May the group released a trading update covering the first four months of the year. Trading was strong and ahead of management expectations having benefited from lower energy costs and favourable currency translation effects. Polymer prices, which eased slightly in Q1, now seem to be firming again and although the group will be passing these increases on to their customers, there will be the usual lag in doing so.

They also announced the closure of their films plant at Sevenoaks. Production of high quality films will be moved to a larger, more modern facility at Bromborough. This site has faster production rates and has recently been upgraded by a significant capital expenditure programme, making it the largest speclialised film plant in the country.

Closure costs at Sevenoaks will be around £1M and the board currently anticipate an increased contribution from the Bromborough plant of over £1M per annum from 2017. These closure costs will be offset by the gain on disposal of the Chinese subsidiary of over £5M as previously announced. In all, the board remain confident of the outcome for 2016.

Steady progress seems to be being made here then and I have bought into the company for the first time.

On the 9th June the group announced that it had received a cash and share offer for the company from RPC. Under the terms of the offer, each shareholder will receive 470p in cash and 0.60141 new RPC shares. This offer values BPI at about 940p per share based on the closing price of 781.5p for RPC. The offer represents a premium of about 30% on the closing price of BPI shares. Based on RPC’s closing price of 815.5p, however, the offer values each BPI share at 960.4p.

So far RPC have received irrevocable undertakings and a letter of intent with respect of nearly 21% of BPI shares and the board recommend the offer. This seems decent enough to me, although a bit of a shame to see the company go. Nonetheless, this has been a decent profitable trade for me.