Real Good Food has now released its final results for the year ended 2016.

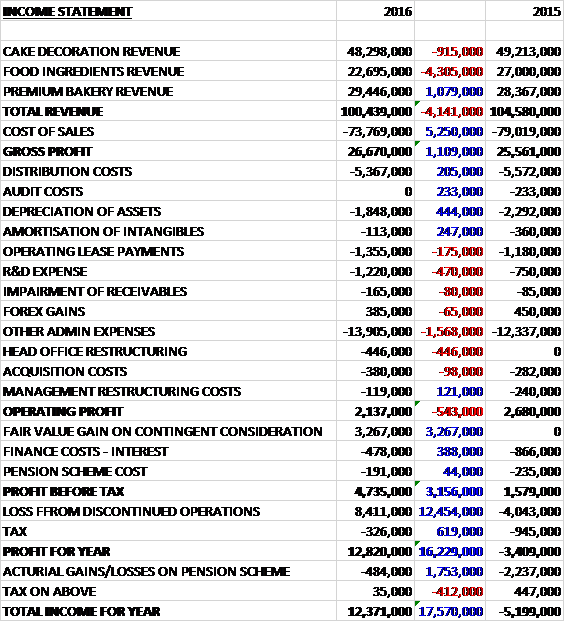

Revenues declined when compared to last year as a £1.1M growth in premium bakery revenue was more than offset by a £4.3M fall in food ingredients revenue reflecting low prices and a £915K decrease in cake decoration revenue due to the move away from low margin contract business. Cost of sales also decreased, however, so the gross profit was up £1.1M. Distribution costs were down modestly, as was depreciation and amortisation but there was a £470K growth in R&D expenses not capitalised and other admin costs grew by £1.6M which meant that the operating profit was down £543K. The group received a £3.3M fair value gain on contingent consideration as the contingent conditions were not met, and interest costs were down £388K which meant that after tax charges also reduced, down £619K, the profit for continuing operations for the year was £4.4M, a growth of £3.8M year on year.

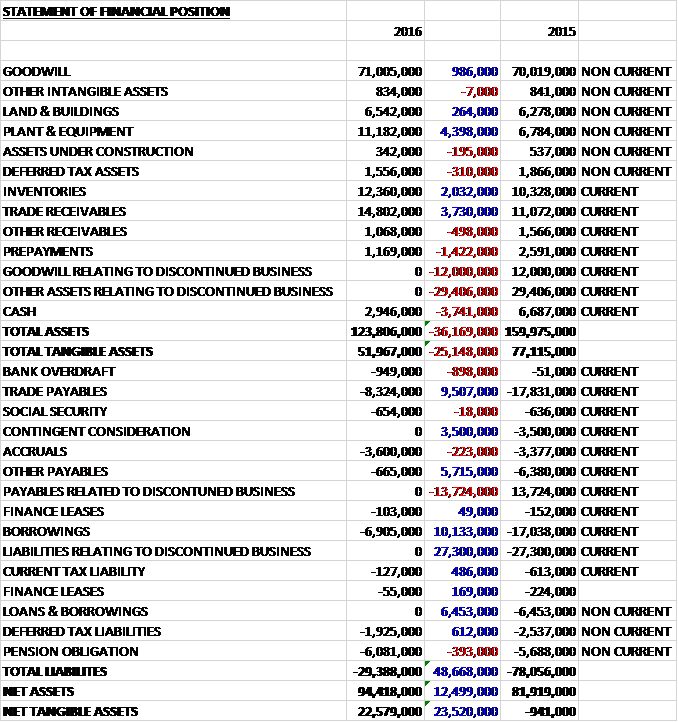

When compared to the end point of last year, total assets declined by £36.2M driven by a £41.4M decline in assets held for sale, a £3.7M fall in cash and a £1.4M decrease in prepayments, partially offset by a £4.4M increase in the value of plant & equipment, a £3.7M growth in trade receivables and a £2M increase in inventories. Total liabilities also declined during the year as contingent consideration payments fell by £3.5M and borrowings were down £16.5M. The end result was a net tangible asset level of £22.6M, a growth of £23.5M year on year.

Before movements in working capital, cash profits increased by £3M to £4.2M. There was a large cash outflow from working capital, however, due to an increase in inventories and receivables so that after tax payments were also up, there was a net cash outflow of £4.2M from operations, a detrimental movement of £7.8M year on year. The group also spent £6.4M on property, plant and equipment reflecting the modernisation of the group’s factories, of which £2.4M included the new group innovation centre, along with £1.7M on acquisitions but they received £37.2M from the disposal so that before financing there was a cash flow of £25.1M. This was used to repay borrowings to give a cash outflow of £4.6M for the year and a cash level of £2M at the year-end.

The operating profit in the Cake Decoration business was £6.5M, a growth of £979K year on year on sales revenue that was slightly down as Renshaw removed a manufacturing contact and Renshaw Europe lost a private label contract. Export sales outside Europe showed good growth. At Rainbow Dust Colours sales of Progel food colouring and metallic food paints in particular showed good growth. As the market matures, opportunities are appearing in more mainstream retailers such as Hobbycraft and John Lewis.

The new focus on developing a global branded range will take share during the course of 2016. A relaunch of the core sugarpaste range in upgraded packaging is already having a strong impact on the market as is the introduction of Renshaw Extra, a firmer and more elastic product designed for European tastes and also more effective in hotter climates. Further significant product initiatives will be launched in early 2017. At Rainbow Dust Colours, a number of major product initiatives are also in place; a relaunch of the food art pens, an upgraded recipe on matt food paints and new multi-lingual packs on Progel.

The operating loss in the Food Ingredients business was £451K, a detrimental movement of £711K when compared to last year as revenues were significantly down due to unprecedented commodity price deflation, particularly in sugar and dairy. Both these markets experienced record low levels of prices with sugar affected by the ending of quotas in Europe in 2017 and dairy impacted by the Russian export ban. Garrett Ingredients increased its traded dairy volumes but sugar sales fell slightly.

The acquisition of ISO2 Nutrition generated a modest amount of sales but set up costs led to a small overall loss in the year. Sales volume was slightly ahead of the previous year at R&W Scott but again price deflation led to a marginal revenue decline. Investment in management teams at both businesses led to higher costs and a decline in profits but they are now fully equipped to run on a stand-alone basis and develop their growth plans.

Garrett Ingredients is well placed to benefit from any upturn in sugar and dairy pricing and will build sales in sports nutrition. At R&W Scott a number of product initiatives such as soft fillings, fruit fillings, curds, mallows and premium jams have been developed and are being sold across all channels. The investment in jam capacity, which caused some disruption last year, should now begin to yield benefits. The business will also significantly increase its supply into other group companies.

The operating loss in the Premium Bakery division was £162K, a detrimental movement of £606K compared to 2015. There is one customer in this division that accounts for a huge 17% of the group’s overall external sales. Despite the narrowing of the product range, sales at Haydens actually grew with the growth rate quickening in H2 but there was a significant labour cost increase which led to the decline in profits. The extension of the customer base had a positive effect on sales but product complexity remains the challenge and is being addressed with an even greater focus on fewer product lines with the impact of this being seen already in Q4.

The process of further focusing on core lines and processes where the business has recognised product superiority will continue. Part of this will be the launch of a small range of branded premium sweet treats which will be sold to a range of customers and generate significant scale. The Chantilly acquisition has already highlighted a number of cross selling opportunities which will be pursued and there are a number of opportunities for automating non-added value, manual processes which will be prioritised against the scale achieved in each product sector.

The group has acquired two business during the year. In December it acquired the ISO2 Nutrition sports supplement brand from the administrators of Creative Health. This business has been integrated into Garrett Ingredients, part of the Food Ingredients sector and is seen as an enabler to the entry into a new product diversification. The total consideration was just £16K. In February it acquired Chantilly Patisserie which produces frozen desserts supplying the foodservice sector with customers such as Marston’s Brewery, Warner Leisure, Brakes and Country Range. The business complements the offering of Haydens and it is envisioned that significant commercial opportunities for both businesses will be identified as a result. The total consideration for this acquisition was £1.75M.

There were a number of non-underlying costs incurred during the year. The management restructuring costs reflect a number of fundamental reorganisations within Cake Decorating and Head Office. The acquisition costs relate to the purchase of Chantilly Patisserie (£306K) and additional costs for the acquisition of Rainbow Dust Colours (£74K).

The group is exposed to currency risk on purchases of almonds from the US. The risk associated with these purchases is mitigated by matching with sales in foreign currencies. The group is also exposed to currency risk on purchases of sugar from Europe which is also mitigated in the same way.

Since the year-end the group has negotiated extended borrowing facilities with Lloyds Bank to enable it to continue its acquisition and investment strategy. They have entered into an invoice finance facility of £20M on a revolving basis with an interest rate 1.5% above base rate. In addition a new term loan of £3M has been agreed to replace the loan taken out to finance the acquisition of Rainbow Dust Colours which has an interest charge of 2.75% above base rate. To aid the capex growth planned it has also entered into a £4M facility with an interest charge of 3.5% above base.

The food industry faces challenging times with diversifying sales channels, increasing legislative burdens, the growth in the minimum wage and ever-demanding customers. Trading in the first three months of the new financial year has been satisfactory with recent order intake positive, and with the investments the group are making the board are confident that they will deliver growth across all three divisions.

At the current share price the shares are trading on a PE ratio of 20.5 which falls considerably to 9.1 on next year’s consensus forecast. At the year-end, net debt stood at £5.1M compared to £30.1M at the end of last year as the proceeds of the disposal were received.

Overall then this was a bit of a mixed set of results for the group. Profits did increase, but this was due to the gain on contingent consideration as a prior acquisition did not hit performance targets – not really something to be cheered. Excluding that, profits were broadly flat. Net assets did improve due to the disposal and they not look much more healthy but there was an operating cash outflow, a deteriorating position when compared to last year, although the blame can be placed on less favourable working capital movements this year as cash profits grew.

The only profitable division is currently Cake Decoration and a better mix of sales meant that profits here increased. Both of the other divisions struggled with losses at Food Ingredients widening due to lower dairy and sugar prices, and the Premium Bakery business swinging into a loss which is being blamed on higher staff costs. The weak Sterling is unhelpful to the group and trading so far this year is described as merely satisfactory. Despite the forward PE ratio of 9.1 making these shares look cheap, I do not believe here to make me buy in just yet.

On the 12th September the group released a trading update for the first four months of the year. Overall the board are satisfied with the performance and remains confident in meeting market expectations for the full year. The order intake is strong, particularly in the premium bakery business which is showing double digit percentage revenue growth. The cake decorating business also has good order visibility which gives the board confidence in that area.

The group are conscious of the impact of the living wage increase and are undertaking a plan to make the most efficient use of their labour force across their operations but the board feel it is important to start to pursue a progressive dividend policy alongside this. It is currently anticipated that an interim dividend will be declared for FY 2017 which will be the start of regular payments.

They have not seen any material negative impact on any of their operations as a result of the Brexit vote, which is reassuring.