Portmeirion has now released its interim results for the year ending 2016.

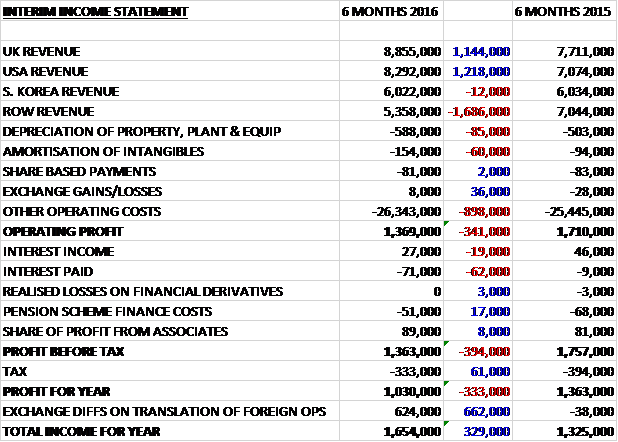

Revenues increased when compared to the first half of last year, although this was due to a £1.5M contribution of sales from Wax Lyrical as a £1.7M decline in ROW revenue and flat S. Korea revenues were offset by a £1.2M growth in US revenue and a £1.1M increase in UK revenue. Operating costs increased more (£170K were acquisition costs), however, which meant that the operating profit was £341K lower than last time. Interest payments increased by £62K but the tax charge was down £61K which meant that the profit for the period came in at £1M, a decline of £333K year on year.

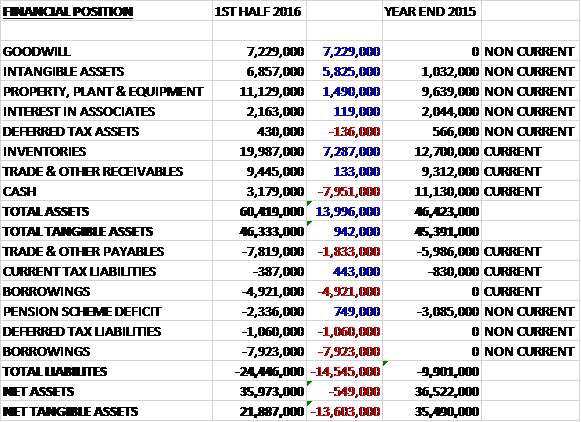

When compared to the end point of last year, total assets increased by £14M driven by a £7.3M growth in inventories, a £7.2M increase in goodwill, a £5.8M growth in intangible assets and a £1.5M increase in property, plant and equipment, partially offset by an £8M fall in cash. Total liabilities also increased during the period due to a £12.8M growth in borrowings, a £1.8M increase in payables and a £1.1M growth in deferred tax liabilities. The end result was a net tangible asset level of £21.9M, a decline of £13.6M over the past six months.

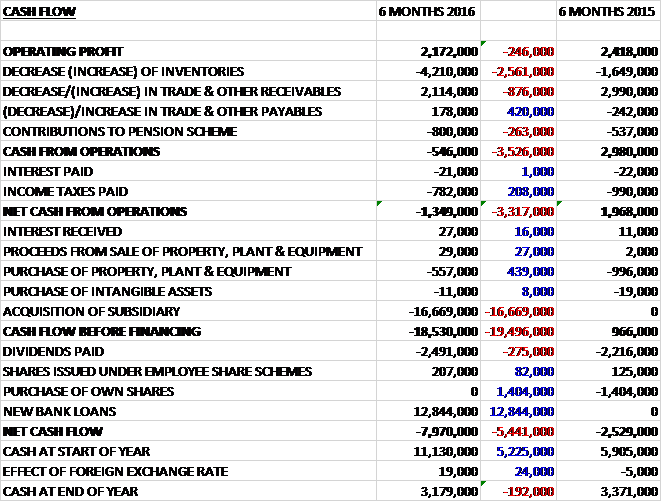

Before movements in working capital, cash profits declined by £246K to £2.2M. There was a cash outflow from working capital with a big increase in inventories, partly seasonal but partly due to the acquisition of Wax Lyrical, and despite tax payments falling by £208K, there was a net cash outflow of £1.3M from operations, a detrimental movement of £3.3M year on year. The group spent just £557K on property, plant and equipment but laid out £16.7M on an acquisition to give a cash outflow of £18.5M before financing. They then paid out a further £2.5M in dividends and took out £12.8M of new loans to give a cash outflow of £8M for the period and a cash level of £3.2M at the end of the half.

The group received a benefit from the favourable USD/GBP exchange rate but even on a constant currency basis, sales to the US also increased. Excluding the contribution from Wax Lyrical, sales to the UK saw a 1.5% decrease as the 19% growth in their own retail and online sales was more than offset by a 12.5% fall in wholesale sales. The South Korean market continues to be difficult. Revenues from the country are level on last year due to the timing of shipments and they expect full year revenues to be below those of last year. They are working with their distributor in this market on a number of new product ranges which they expect to start selling later this year.

Last year’s good growth in India has not been repeated this year as sales in the first half were some £2M below the same period of 2015. The group are taking corrective action, looking for additional distributors targeting specific distribution channels in India but they do not expect this to start bringing in sales until 2017. The group have strengthened their sales team. They have refocused their efforts on Europe and have just appointed a new sales manager to target the South American and Middle Eastern markets where they have historically sold little. They expect their sales in China, where they have a trading subsidiary and have appointed a number of distributors, to increase significantly from 2017.

First half profits are not a reliable indicator of full year profits and in particular, because of the recent investments in new factory capacity, they expect the imbalance to increase with the acquisition of Wax Lyrical exacerbating this effect.

The Anti-dumping case which the group have been challenging since 2012 has gone against them and they have abandoned their attempts to reclaim more than £2M which this has cost. It is expected that anti-dumping will expire in 2018.

As a result of the reduced demand from Asia, the group have pulled production back to levels just below last year. They remain confident that the demand for production will be recovered and the new kiln is a long-term investment.

On the 4th May the group acquired Wax Lyrical for a total cash consideration of £17.5M. The business is the UK’s largest manufacturer of home fragrances and is both a wholesaler and retailer of its home fragrance products, primarily scented candles and reed diffusers, to both UK and export markets. The acquisition generated goodwill of £7.2M and the business made a profit of £2.1M last year and is expected to be earnings enhancing in the current year, although the profit impact so far this year has been minimal. Significant growth opportunities for Wax Lyrical’s products are envisaged within the group’s existing market and in particular the group expect to be able to grow their sales through Portmeirion’s existing UK customers, websites and retail outlets as well as export markets.

The success seen in India last year has not been repeated in 2016 and sales to South Korea have not recovered as originally hoped. The board expect the adverse situation in both of these markets to continue in the short term. In addition they are starting to see a negative effect on wholesale demand from Brexit towards the end of the period. Despite this, they remain confident that the revised expectations of the full year profit will be met but are adopting a prudent forward view.

At the current share price the shares are trading on a PE ratio of 13.9 but this increases to 16.1 on the full year consensus forecast. After a 15% increase in the interim dividend, the shares are yielding 3.4% which increases to 3.5% on the full year forecast. At the period-end, the group had a net debt position of £9.7M compared to net cash of £11.1M at the prior year-end and a net cash position of £3.4M at the same point of last year.

Overall then this has been a difficult period for the group. Profits were down, net assets declined and the operating cash flow deteriorated with a cash outflow this time, not helped by adverse working capital movements. The US was the one area of growth but in the UK, wholesale sales deteriorated, apparently Brexit-related. South Korea remained difficult and despite sales being flat in the first half, they are expected to be lower for the full year. The real disappointment was India, with the strong showing last year not repeated.

The acquisition does seem to be a decent one and is probably the saving grace here – despite this, however, I am a little concerned that the board seem a bit over-confident of hitting full year targets. The dividend yield of 3.5% is decent enough but the forward PE of 16.1 fails to really price in the issues here I feel. This is not for me at this time, such a shame!

On the 19th January the group released a trading update covering the year where they stated that pre-tax profit was expected to be slightly ahead of market expectations. They expect to report record revenues for the year of over £76M, an increase of 11% year on year. The revenue contribution from Wax Lyrical was over £10M and the business performed in line with management expectations. At a constant exchange rate, the total group revenue increase would have been nearer 7%.

The Indian and South Korean markets have been challenging and total revenues from these two markets were over £7M below the reported revenue last year. Nevertheless, overall total revenue increased and the board look forward with confidence.

While it is good that profits will be slightly above expectations, I would have thought this is likely to have been forex-based. In addition it seems that much (if not all) of the revenue growth is due to the acquisition. I am not quite convinced that this company has turned around.