Orosur Mining has now released its final results for the year ended 2016.

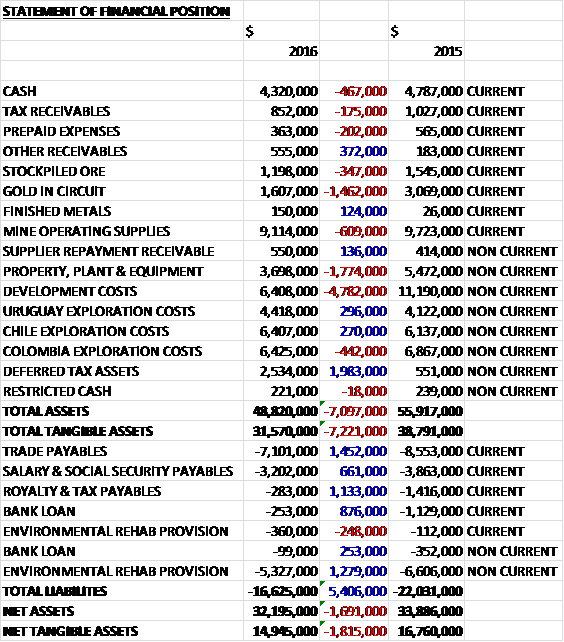

When compared to the end point of last year, total assets declined by $7.1M to $48.8M driven by a $4.8M decline in development costs, a $1.8M fall in property, plant and equipment and a $1.5M decrease in the value of gold in circuit, partially offset by a $2M growth in deferred tax assets due to increased fiscal losses. Total liabilities also fell during the year due to a $1.5M decline in trade payables, a $1.1M fall in royalty and tax payables, and a $1M decrease in the environmental rehabilitation provision. The end result was a net tangible asset level of $15M, a decline of $1.8M year on year.

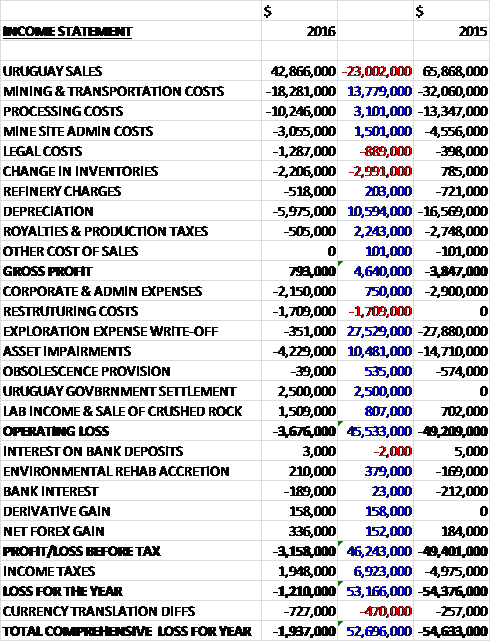

Revenues declined by $23M when compared to the prior year due to lower quantities sold and a reduced gold price, but costs were also down with mining costs falling by $13.8M, processing costs down $3.1M, mine site admin costs falling by $1.5M, depreciation down $10.6M due to the prior year impairments and lower production this year, and royalty costs falling by $2.2M due to the exemption granted during the year. This gave a $4.6M improvement to gross profit. Corporate expenses fell by $750K but there were $1.7M of restructuring costs. Offsetting this, there was a $2.5M government settlement and an $807K growth in other income.

The big movements, however, were a $27.5M reduction in exploration costs written off and a $10.5M decline in asset impairments to give an operating loss $45.5M lower than last year. We then see a forex gain, a derivative gain and a $379K positive swing in the environmental rehabilitation accretion. There was also a $6.9M positive swing to a tax credit relating mainly to deferred tax, relating to the depreciation of the Uruguayan Peso and the effect this has on the value of assets, along with the recognition of $2.5M of deferred tax losses on the basis that sufficient taxable profit will be generated in order to utilise the benefit of the losses, to give a loss for the year of $1.2M, a positive movement of $53.2M year on year.

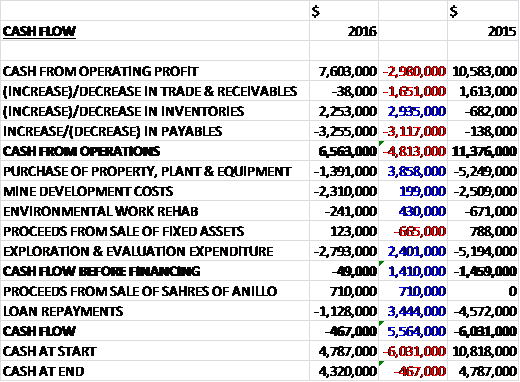

Before movements in working capital, cash profits declined by $3M to $7.6M. There was a modest cash outflow from working capital with a decrease in payables so the cash from operations came in at $6.6M, a decline of $4.8M year on year. The group spent $1.4M in property, plant & equipment; $2.8M on exploration expenditure and $2.3M on mine development costs to give a cash outflow of $49K before financing. The group brought in $710K from the sale of Anillo shares and repaid $1.1M of loans to give a cash outflow of $467K for the year and a cash level of $4.3M at the year-end.

Production for the year was 35,773 ounces of gold, above the stated guidance of between 30,000 and 35,000 ounces but below the 53,485 ounces produced last year as a result of the implementation of a new strategic plan in response to the lower gold price environment in H2 2015. During the year, 1,013,104 tonnes of ore was processed at a grade of 1.19g/t compared to 1,212,463 tonnes at 1.48g/t last year; and 925,583 tonnes of ore was mined at a grade of 1.24g/t compared to 1,182,457 tonnes at 1.5g/t last year. Some of the planned high grade stopes of Arenal could not be mined during Q4 and as a consequence, minor grade ore from other sources was processed, meaning the average grade processed in Q4 was just 0.96g/t. The high grade material of Arenal was delayed until June, which has already been recovered during this month.

The average gold price realised for the year was $1,154 per ounce, a decrease of 6% year on year. All-in sustaining costs were $1,069 per ounce, a reduction of 10% when compared to last year and in line with prior guidance. In the second half of the year, costs were $978 per ounce in Q3 and $971 per ounce in Q4 after the implementation of a strategic plan to reduce costs and ensure more profitable production.

During the year, geological and engineering development activities were mostly focused on the start-up of the SGW underground project, the second mechanised underground mine in Uruguay, after Arenal. It is a continuation of the San Gregorio open pit deposit which, to date, has produced more than 500K ounces at an average grade of 2.1g/t.

Capex is expected to be minimised and personnel and equipment have started to be shifted from Arenal to San Gregorio. By phasing the development with the closure of Arenal Deeps, the group intends to fund the development with internal cash and cash flow, although there are risks to this approach. It is anticipated to start production by the end of the first half of 2017. The plan for 2017 is to accelerate the definition of resources and reserves in areas such as San Gregorio East UK, SG West UG and Argentinita UG.

San Gregorio East is a sector contiguous to the SGW UG project where the group is aiming to drill a further 3,000m aimed at increasing and validating reserves. The group has completed the first drill hole in this programme, intercepting attractive mineralisation over a significant interval. They also aim to further explore a potential San Gregorio West underground extension located at depth, below the portion of the reserve base which will be put into production and mined in 2017. The deposit in this sector is open at depth and the group will conduct six dee drill holes to test the area below. Historic drilling at this location has demonstrated promising mineralisation and mineralised intervals. At the company’s Argentinita UG development project, 27K ounces of maiden reserves have been delineated and a drilling campaign is planned with the intention of increasing and upgrading this reserve.

The Veta Rey open pit remains in production. In recent months, the mine has supported plant ore feed while SGW UG is being developed. At the same time, Veta Rey provides waste material which is used in the construction of a new tailings dam phase, further optimising loading and hauling costs. The Veta Rey open pit has produced about 14K ounces over the past two years. As in the case of Veta Rey, the group’s suite of open pit projects in Uruguay are currently being re-evaluated for potential development and production activities in the higher gold price scenario present at the moment. Based on internal analysis, some targets at Santa Maria and Peru appear to be economic at or around $1,300 per ounce, which could result in additions to the mine plan of around 10K to 12K ounces.

During the year, exploration activity was concentrated on brownfield activity near the current mines, while some of the most promising exploration projects and targets were re-evaluated during the year. This work has enabled the group to put forward a solid work plan for 2017 with the objective of further consolidating and extending mine life. As a result of insufficient mineralisation encountered during exploration drilling, the previously announced Arenal Repetition exploration project has been discontinued.

In Southern Uruguay, a number of high grade, low tonnage targets were identified for treatment and processing in the San Gregorio plant, as part of the group’s approach to extend mine life. The permitting process for confirmatory and exploration drilling at these projects is currently underway.

As far as capex was concerned, the group invested $3.9M in capital and $2.8M in exploration. The construction of phase 3 of the second tailings dam was finalised during the year as well as additional investment in the repair of heavy equipment, and the development of Arenal Underground and the San Gregorio Deeps project. The efforts to meet the new guidance were accompanied by cost reduction measures across the group’s exploration activities. At the San Gregorio Deeps project, the fortification of the entrance to the main ramp was concluded at the end of the period and the preliminary system ventilation to the tunnel was in place. First blasting at the portal was started in May 2016.

Permits for San Gregorio Deeps were granted from the mining authority during February 2016 and the group is planning to have SGD operational during 2017 and therefore development work has already started in Q4. First blast took place in May 2016 and the company will not require sourcing of additional non-dilutive project funding for as it will be financed from cash from operations.

At the high-grade Anza project the group is currently evaluating a number of options in advance of the project. They are generating a geological model and carrying out some exploratory metallurgical tests. The project includes two small underground gypsum mines which have their environmental and mining permits already granted by the Colombian authorities. This constitutes a strategic element of the project as it gives the possibility to fast track an extension of those permits for a future gold mining operation. These gypsum mines have been operated by a contractor and the group is in the process of taking over operatorship.

At Anilo, in June 2015 the group signed the definitive option agreement for the funding of the next phases of exploration with Asset Chile. The agreement defines a non-dilutive financing of up to $3.5M to advance the exploration of Anillo and states that Asset Chile may earn up to a 40% interest in the project. In July 2015, Asset Chile invested $850K to funding of the phase 1 of the exploration while the group placed $100K to complete the budget.

A total of 21.5km of ground geophysics and 3.6km of reverse circulation drilling were carried in late 2015 to test five targets. The results demonstrated the presence and continuity of Au-Ag mineralisation in three zones related to high and low sulphidisation epithermal systems, which have been passed to the delineation stage. A pipeline of six Au-Ag opportunities have been defined at the property, including three areas coming from indicative old works of the company.

During July 2016, Asset Chile requested an extension until March 2017, which the company accepted, to allow them to decide on exercising their option to move to phase 2. In this period, Asset Chile will contribute $120K to cover the minimum expenditure in Anillo and they need to complete their contribution to phase 2 (up to $1.25M to fund 5,5km of RC drilling) in order to earn a 32.5% interest of the group’s share in Anillo. In the case that they do not complete this phase 2, they will lose their earn-in achieved to date.

At Pantanillo, none of the annual minimum amounts were paid as Anglo American granted an extension to December. Last year the group recognised an impairment charge with regards the project of $25.5M. The group decided not to fulfil the payment of advanced royalties totalling $1.6M due to Anglo by December which triggered a process for the properties to be returned to Anglo, a process that is ongoing.

At Talca, during the year the group conducted a property review to try to generate value from the asset. Some field work was undertaken to raise relevant information and the property was presented to potential partners and investors. At Noletir in Uruguay, as of the year-end the parties were waiting for the Government’s grant of new mining licenses in order to continue with the exploration campaign and on this basis, Noletir has requested an extension to the December 2015 deadline.

At the Chamizo gold project in southern Uruguay, in November 2015, Minerales Cala gave notice to the company of the completion of its expenditures and reporting obligation with respect to phase 2 of the option agreement thereby earning an additional 29% interest in the project for a total of 80%. Simultaneously, they requested and the company granted its consent to enter into an option agreement with Patagonia Gold to transfer in a phased manner their interest in the project. In January 2016, the agreement was exercised and as a result, Patagonia has been funding Minerales Cala’s expenditures for phase 3 of the project. As of the year-end the group retained a 20% interest and phase 3 of the option agreement had started and exploration work carried on based on a proposed programme submitted for the first half of 2016.

At the Isla Cristaline Belt, Gladiator has notified the group f its completion of the work contemplated by phase 2 and in June 2015 they submitted a statement of expenditures. In September 2015, due to a number of objections concerning these expenditures and an ongoing dispute between the parties, the group requested an audit of the statement. By the end of the month, Gladiator notified the group that they do not intend to complete phase 3 of the option agreement and therefore that phase 3 has expired. Once the audit of the phase 2 expenditures has been finalised, the parties will be required to renegotiate a new joint venture agreement in order to continue with the development of the project.

During the year the group completed an assessment of the carrying value of its CGUs and recorded an impairment charge of $4.2M relating to underground development costs and driven by changes in reserve estimations as the company enters the final stages of the Arenal Deeps project. It is expected to reach the end of its mine life by mid-2017. The group also undertook a sensitivity analysis to identify the impact of changes in long-term pricing. They believe a 10% change in the gold price assumption will not have an impact on the estimated recoverable amount, although a 10% reduction in the gold price would reduce profits by $4.2M with the opposite being true. The group have also hedged about 2,200 ounces of gold at a forward price of about $1,258 per ounce.

In April 2013 the group made a prepayment of $550K to a supplier to start the raiseboring of the Arenal underground. The supplier was unable to provide the services so as a result the group initiated actions to recover the amount and a positive arbitration award was received in April 2014. As defence the supplier filed for judicial review of the award offering as counter-guarantee equipment valued at $600K. In May 2016, the defence was dismissed and the court ordered the freezing of the supplier’s bank accounts and the valuation of the equipment to sell it at auction. The group expects to recover the amount in addition to damages and fines.

In December 2015, the president of Uruguay granted the group an exemption on the royalty payment to the government (3% of sales) covering the period from April 2015 to March 2016.

The group has $1.5M of undrawn line of credit with Santander available as of the year-end and the board believe this to be more than adequate given the current gold price environment.

The group’s forecast production guidance for 2017 is increased to between 35,000 and 40,000 ounces of gold at operating cash costs of between $800 and $900 per ounce. This is an improvement on this year as they expect to benefit from the savings generated by the ongoing optimised operations as well as higher grades from the underground project which will be offsetting external factors such as inflation in Uruguay. The group expects to maintain the level of savings achieved and plans to continue its operational improvement programme focused on sustainable cost cutting measures and driving ongoing operational efficiencies.

As the group is still loss-making, we can’t really get much from PE ratios but on next year’s consensus forecast, they are trading on a future PE ratio of just 2.4.

On the 23rd August the group announced that non-executive director, Pablo Marcet sold 1,000,000 shares at a value of £188K. He retains 1,215,338 shares in the company.

Overall this was a mixed year for the group. They are still loss making due to continued impairments but the performance has improved year on year. Net assets declined, however, as did the operating cash flow with no free cash being generated, although it should be noted that the group is not losing too much cash. Gold production reduced this year as expected due to the lower gold price environment at the time but the grade reduced in Q4 due to the higher grade stopes of Arenal not being able to be mined, although this has now been rectified.

The average gold price was below that of last year but it has since recovered and the reduced costs of $971 per ounce in Q4 look pretty decent. The forward PE of 2.4 looks very cheap but I am rather nervous over the phasing f the San Gregorio pit start-up. There is very little room for error and I would have thought there is some risk here. Probably a bit too much risk at these prices.