Empresaria has now released its interim results for the year ending 2016.

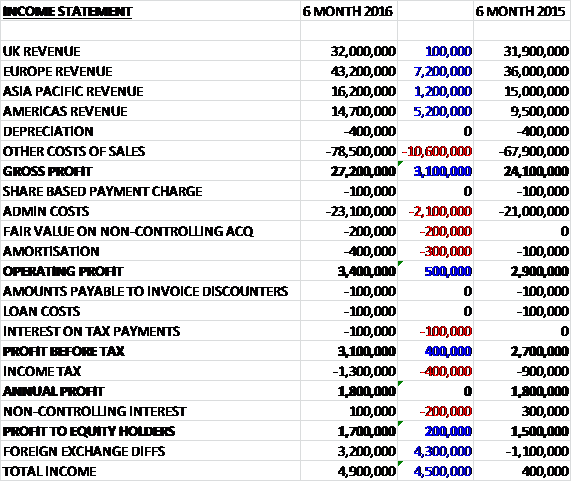

Revenues increased when compared to the first half of last year with a £7.2M growth in Europe revenue, a £5.2M increase in Americas revenue and a £1.2M growth in Asia Pacific revenue. Cost of sales also increased to give a gross profit £3.1M ahead. Admin costs grew by £2.1M, amortisation was up £300K and there was a £200K charge relating to a change in fair value on non-controlling interests so the operating profit grew by £500K. There was also a £100K interest charge on late tax payments and income tax increased by £400K reflecting higher levels of prior year charges and a change in profit mix from different tax areas which meant that the profit for the period came in at £1.7M, a growth of £200K year on year.

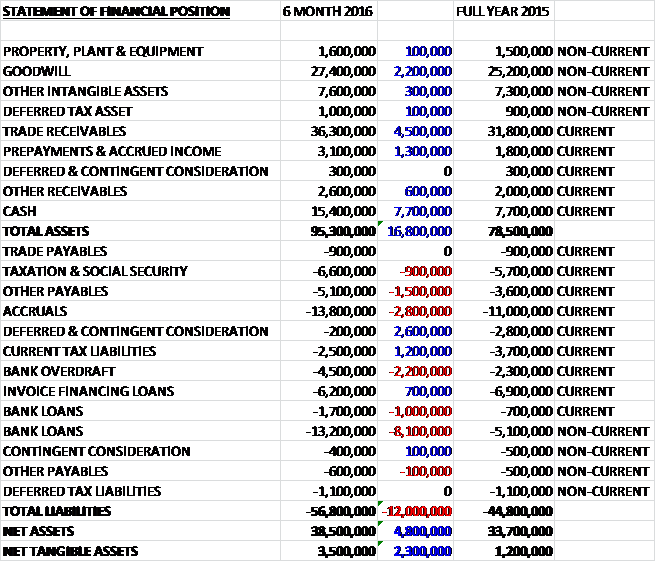

When compared to the end point of last year, total assets increased by £16.8M to £95.3M, driven by a £7.7M growth in cash, a £4.5M increase in trade receivables, a £2.2M growth in goodwill and a £1.3M increase prepayments and accrued income. Total liabilities also increased as a £9.1M increase in bank loans, a £2.8M growth in accruals, a £2.2M increase in the bank overdraft and a £1.5M increase in other payables was partially offset by a £2.7M decline in deferred consideration and a £1.2M fall in current tax liabilities. The end result was a net tangible asset level of £3.5M, an increase of £2.3M over the past six months.

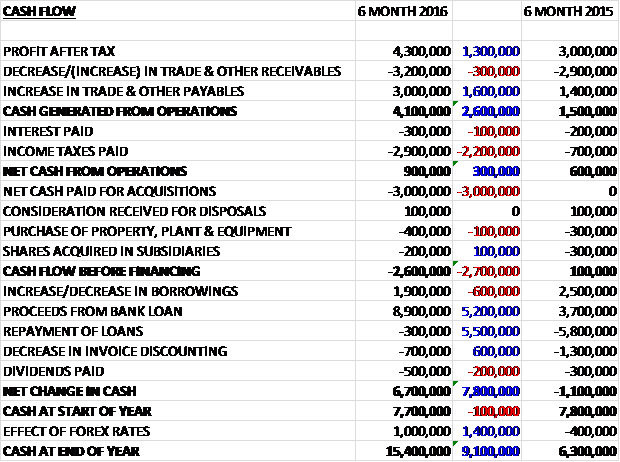

Before movements in working capital, cash profits increased by £1.3M to £4.3M. There was a slight cash outflow from working capital but a higher increase in payables than last year was offset by a £2.2M increase in income tax payment, partly relating to a German tax review, to give a net cash from operations of £900K, a growth of £300K year on year. The group spent £400K on tangible assets, £200K on acquiring non-controlling interests and £3M on acquisitions so before financing there was a cash outflow of £2.6M. We then see a net £8.6M brought in from new loans and a £1.9M increase in other borrowings to give a cash flow of £6.7M for the period and a cash level of £15.4M at the period-end.

The operating profit for the UK business was £500K, a decline of £500K year on year with temporary sales up 1% and permanent sales down 1%. The growth in temporary sales was helped by a good performance in the Technical and Industrial sectors. There was also temporary sales growth in Professional Services, although this was offset by falls in permanent sales. Since the global financial crisis the businesses in this sector have diversified away from a primary focus on financial services, so are now better placed to deal with any slowdown. In the IT & Digital sector, the group made changes to the senior management teams which is having a short-term negative impact on profitability but is necessary to reposition the business on a growth trajectory.

The build up to the EU referendum led to a slowdown in May and June as business confidence dropped and hiring decisions slowed. Following the Brexit vote, the market has stabilised and sales pipelines are holding up well, but it remains too early to see what impact this will have on the businesses for the rest of the year. The bulk of the fall in operating profit was due to increased costs in staff and rent so given the current market conditions, the board are closely monitoring the situation with a focus to reduce costs if trading levels drop in the second half of the year.

The operating profit for the Continental Europe business was £1.8M, a growth of £800K when compared to the first half of last year, helped by positive movements in exchange rates. Both divisions are up on the prior year with the logistics services division growing NFI by 12% through greater client penetration and the temporary division growing by 20% with a focus on investing in new staff and training to develop new sector coverage Market conditions in Germany remain positive.

As previously highlighted, new legislation has been announced in Germany to be implemented in January 2017, which will limit the time a worker can be a temporary worker at the same client to 16 months. The group are working on plans to address this. In the Finnish Healthcare business, results are following a positive trend but they continue to operate in a weak economic market. Cost reductions made last year are helping to improve profits with NFI flat on a constant currency basis.

The operating profit for the Asia Pacific business was £900K, an increase of £100K when compared to the first half of 2015 with both temporary and permanent sales up, aided by positive forex movements (constant currency revenue growth was just 0.5%). The best performers were in Japan, China and India. China has seen significant growth following a restructure of the team in the second half of last year, with a focus on the local Shanghai market and showing no signs of being impacted by the wider Chinese economic slowdown.

The economic conditions in SE Asia have been mixed, with the Executive Search brand in the Philippines and Malaysia seeing growth, but Indonesia and Thailand down year on year. The training business in Indonesia has stabilised, with cost reductions made last year offsetting a small drop in NFI. In the Middle East the fall in the oil price has negatively impacted business confidence and the market has seen a slowdown in the first half of the year. NFI in the region was down 27% in what is purely a permanent market, but costs have been reduced in line with the reduced trading and the board expect the business to remain profitable this year.

There are a number of important infrastructure projects that are expected to be started by the end of the year, being work to get Dubai ready for the Expo 2020 and in Qatar for the football work cup in 2022. Whilst some of this work has been postponed due to local economic conditions, the timetable requires work to start in earnest shortly which should provide a boost to the local staffing market next year.

The operating profit for the Americas business was £200K, a growth of £100K year on year reflecting a full contribution from the Pharmaceuticals Strategies business. The new business has performed in line with expectations and has started work with a number of new clients which should help generate growth over the next 18 months. In Chile the group have seen good growth in their seasonally stronger half year. Over the past couple of years the group have focused on developing temporary and permanent sales services to complement the traditional outsourcing business. This is progressing well, helping revenue grow 19% on a constant currency basis and the outsourcing business is growing through greater client penetration. The start-ups in Mexico and Chile in Executive Search are progressing, although it takes time to get tractions with new office openings.

During the period there was a positive impact on profits due to the relative weakness of sterling against various other currencies, although the currency was actually stronger against the Indian Rupee, Chilean Peso and Thai Baht. As of the period-end, all of the major currencies the group operate with had strengthened against Sterling, ranging between 9% in India and 28% in Japan. If currency rates remain at these levels throughout the rest of the year, there would be a greater positive translation effect in the second half of the year.

In April the group increased their interest in Ball & Hoolahan from 75% to 100%, acquiring from the founder who left the business as part of a planned transfer of ownership. The consideration was £200K, all paid in cash. In June they increased their shareholding in Monroe (Executive search in Thailand) by 10%, taking it up to 70%. The consideration of £200K was paid in cash and a £200K fair value charge has been recognised in the income statement. They have also finalised a second generation plan in Germany, with four managers buying up to 16% shares in their respective legal entities of Headway. These shares only create value if the profits exceed historic levels.

After the end of the period, in July, the group invested in an 82.6% share of Rishworth Aviation, an international specialist recruiter in the Aviation sector with offices in New Zealand and Sweden. The total consideration was £7.5M which was fully paid in cash on completion. The remaining 17.4% interest in the business is held by senior management. The business had net liabilities of £451K so the acquisition generated goodwill of nearly £8M. It is expected to be earnings enhancing on an adjusted basis this year.

At the period-end, net debt stood at £10.2M compared to £7.3M at the end of last year. During the period a new five year UK revolving credit facility of £10M was entered into. At the period-end, £6M had been drawn down in readiness for the investment in Rishworth Aviation. The bank loans include a £4.5M UK term loan which matures in October 2018. They also include a €5M term loan in Germany which expires in February 2018 and in total the group has £15.4M of bank facilities undrawn.

The group continue to look for suitable external investments to fill in gaps in their sector or geographic coverage with a pipeline of prospects. The board see strong growth opportunities across the group and remain confident in their ability to deliver increasing profits and their ability to meet market expectations in the current year.

At the current share price the shares are trading on a PE ratio of 11.7, falling to 9.5 on the full year consensus forecast. As usual there is to be no interim dividend paid which means the yield remains at 0.9%, increasing to 1% on the full year forecast.

Overall then this has been a fairly good period for the group. Profits were up, net assets increased and operating cash flow improved, although the group still seems unable to be able to make any free cash. The performance in the UK was not so good, being affected by extra costs associated with senior management change, and a slowdown in the run-up to the EU referendum, put the performance elsewhere was much better.

There was a strong result from the rest of Europe, in particular Germany, although the new legislation on temporary workers in the country is a concern as it looks likely to affect the group. The performance in Asia Pacific was good, with growth from Japan, China and India, although the low oil price is having an effect on the Middle East market. There was also growth in the Americas as Pharmaceutical Strategies started contributing. There are also currency tailwinds currently for the group as they benefit from weak Sterling.

I do think the debt is a bit high for my liking, however, especially following the Risworth acquisition and it concerns me slightly that they are already lining up more acquisitions. The forward PE looks good value at 9.5 but this probably excludes acquisition costs and amortisation etc. This is a tricky one, it looks pretty decent value and the diversification is great but I am concerned they are over-stretching the balance sheet a bit.

On the 6th October the group announced that it had purchased a 65% interest in ConSol Partners for a cash consideration of £9.4M. The remaining 35% will be held by the senior management team. The business is a specialist recruitment group in the IT sector with a focus on the niche sectors of communications & mobile, cloud technologies and the digital supply chain, operating in the US, UK, US and Continental Europe. They provide both contract and permanent staffing services with 57% of NFI coming from contract services.

The business made a pre-tax profit of £1.2M last year on revenues of £23.4M. The board believes the investment will be earnings neutral on adjusted basis this year and earnings enhancing in its first full year of ownership. The initial cash payment on completion is £4M with a deferred amount expected to be about £5.4M. The transaction has generated goodwill of around £6.7M. The investment will be funded by the existing revolving credit facility but debt levels have now increased above the board’s target. Both debt and the balance sheet are not too rich for me so I am not investing until this changes.

On the 24th January the group released a trading update covering the whole year. Full year profitability will be slightly ahead of market expectations. Adjusted pre-tax profit growth is expected to be 23% year on year, NIF 20% ahead and EPS up 12%.

There were strong performances across the group with Headway in Germany, Skillhouse in Japan and Monroe in SE Asia all delivering solid growth year on year. In addition, the group’s business in Finland, Australia, China, India, Chile and the technical and industrial brands in the UK performed well.

Following a short period of uncertainty in the UK prior to the EU referendum, the UK region has seen stable activity levels return. Overall in the UK this has led to profitability being down year on year but the group has reduced costs and is encouraged by the business activity as the move into 2017. In the Middle East, the weak economic conditions persisted in H2 and expected improvements did not materialise. The business has been restructured accordingly and the group expects an improved result in the coming year from the region.

The group’s US investment, Pharmaceutical Strategies, is integrating well having won a number of new clients and improved penetration across key clients. The decision during the year to invest in their management team and their largest client having reduced its overall spend on staffing requirements has resulted in a short-term impact on profitability. Despite this, the business continues to see good growth opportunities going forward.

In July they acquired Rishworth Aviation and ConSol in October. Both businesses are performing well and demonstrating positive growth potential for the coming years. This all sounds fairly positive but I want to see some actual figures to ascertain the state of the balance sheet which was one of my main concerns last time.

On the 3rd May the group released a trading update. They made a solid start to the year, delivering year on year growth in NFI in Q1 across all four regions. Both Rishworth Aviation and ConSol Partners are performing well and the board are pleased with their integration. They remain on course to meet market expectations for the full year.

On the 21st July the group released a trading update covering the first half of the year. NFI was up 26% with the strongest trading in the UK, Europe and Asia Pacific regions. The group is on course to meet market expectations for the full year.

The recent investments in Rishworth and ConSol have been integrated into the group and the board is pleased with their contributions so far. In Rishworth Aviation the group has invested in setting up new bases for key clients that are expected to deliver growth in terms of pilot recruitment in the coming years. At ConSol, they have invested in the US office which is expected to benefit the business in the second half.