Gem Diamonds has now released its interim results for the year ending 2016.

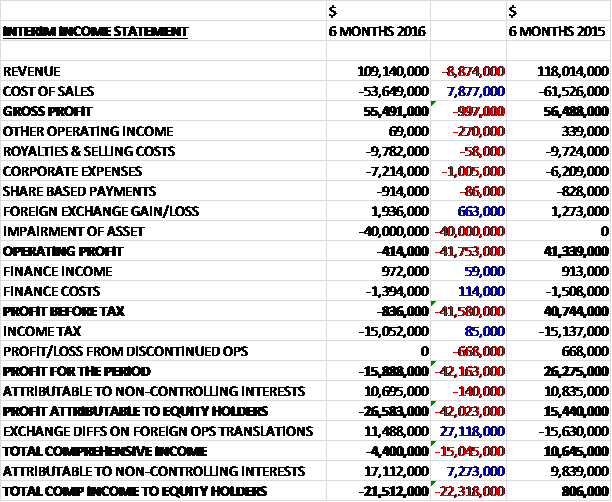

Revenues declined by $8.9M when compared to the first half of last year and after cost of sales also declined, the gross profit was down nearly $1M. Other operating income fell by $270K and corporate expenses were up $1M, although there was a $663K increase in the forex gain. After the $40M impairment at Ghaghoo, however, the operating profit fell by $41.8M to swing to a small loss. Finance costs were down somewhat and tax costs were broadly flat which meant that there was a loss for the period of $26.6M, a detrimental movement of $42M year on year.

When compared to the end point of last year, total assets declined by $23.1M, driven by a £19.3M decline in cash levels and a $3.1M fall in inventories. Total liabilities also declined as a $7.9M growth in deferred tax liabilities and a $1.1M increase in provisions was more than offset by a $4.7M decline in payables, a $4.4M decrease in income tax payables and a $1.8M fall in the bank loan. The end result was a net tangible asset level of $308.1M, a decline of $22.1M over the past six months.

Before movements in working capital, cash profits declined by $11.2M to $59.5M. There was a broadly neutral working capital position compared to a large outflow last time and after a $1.7M increase in interest paid was more than offset by a $9.7M decline in tax payments, the net cash from operations came in at $44.5M, a growth of $5.8M year on year. The group spent $31.3M on the mining of waste, $5.6M on commissioning costs, $6M on property, plant and equipment, and $2.8M on development costs so that before financing, there was a cash outflow of $1.1M. After dividends were paid out, there was a hefty $21.8M cash outflow for the period to give a cash level of $66.5M at the period-end.

The market for both rough and polished diamonds remained cautious. Liquidity constraints, high polished inventory levels and the uncertain macro-economic outlook continue to create challenges for the market.

The Letseng mine produced 57,380 carats during the period compared to 50,019 in the first half of last year and both waste tonnes mined and ore treated were up on H1 2015 driven by additional mining fleet being commissioned. The mine benefited from the plant 2 phase 1 upgrade project completed last year, realising an increased daily treatment rate through this plant. During the period the mine continued to implement the optimised life of mine plan, which enhances the mine’s net present value through optimising waste stripping and increasing the percentage of the higher grade, higher value satellite pipe ore available to be treated over the life of the mine.

The group achieved a grade of 1.72cpht compared to 1.61 last time. The high grades achieved are reflective of the area mined in the Satellite pipe that has historically produced higher than reserve grades, albeit at a slightly smaller average stone size. This also saw a decline in the number of 100+ carat diamonds recovered, impacting the $ per carat achieved. Since the start of July, however, two large diamonds of 104 carats and 85 carats have been recovered as mining moves to a different area.

Further optimisation of the Coarse Recovery Plant during the period included the refinement of the XRT sensitivities, improvement of feed quality and the installation of a high-tech glove box materials handling system to cater for the separation of ore concentrate streams from the two processing plant. The Coarse Recovery plant is currently operating at the designed >5mm cut off.

A capital project of $16.7M to relocate and construct a new mining fleet workshop is under review for the second half of the year. As Letseng continues to invest in the future of the operation, the new waste pushback which is required to extend the length of the open pit has been brought forward. The mining workshops, offices and related services, therefore, need to be relocated within the mining site and will allow the mine to effectively maintain the new and larger fleet of mining equipment. This project will be funded through additional external debt and an initial team sheet has been agreed with lenders.

In late July, extreme weather conditions were experienced in Lesotho where the mine is located, with excessive snowfall and severe winds limiting access to the mine. Following damage to the overhead power lines, standby generators previously installed at the mine were used to mitigate the impact, allowing the plants to continue to operate, albeit at reduced rates. The Lesotho Electricity Company repaired the damaged overhead power lines on the 10th August and the external power supply was fully restored. Given the strong performance in H1, waste tonnes mined and carats recovered remain within the original guidance and the Satellite pipe ore contribution has increased. Full year guidance for operating costs and tonnes treated have been revised, however, and stay in business capital has also been revised to account for the construction of the mining workshop.

Tonnes of ore treated will reduce to 6.6 – 6.8 million tonnes from 6.8 – 7 million tonnes and operating costs per tonne have increased from about 210 to 225 maloti. Stay in business capital has grown from around $9M to about $16M.

Four tenders were completed during the period with a total of 55,948 carats sold in Antwerp. The average price achieved was $1,899 per carat compared to a rolling twelve month total of $2,113 per carat and the figure of $2,264 per carat in the first half of last year. This was due to fewer large diamonds being recovered than usual as mining occurred in the lower value areas of the Satellite pipe.

Among the exceptional diamonds recovered during the period was an 11.8 carat pink diamond which sold for $187.7K per carat, the third highest price per carat for a Letseng diamond; and a 160.2 carat Type II white diamond which was sold into a partnership arrangement with additional participation in the final polished margin.

Going forward, the focus at the mine will be on continuing work streams on enhancing value through reducing diamond damage and progress feasibility studies for the next phase of plant enhancements; continue the implementation of a fleet management system to improve grade control, fleet optimisation and reduce operating costs; start construction of the mining workshop; extend the life of the tailings residue facility by an additional three years through lifting and strengthening the existing wall; and start the review and design of the next three-year CSI plan.

At Ghaghoo, the initial objectives of phase 1 of the development were to confirm the grade, diamond prices and recovery processes, including the use of autogenous milling, which were expected to increase diamond liberation. Based on the prevailing diamond market conditions, however, the operations has been downsized to 300,000 tonnes per annum from the planned phase 1 of 720,000 tonnes. It is anticipated that the planned output rate will be achieved in the second half of the year.

Following the cave-in which occurred in Block 1 at the end of 2015, a buffer zone was created during Q1 this year to prevent the ingress of sand into the production levels, resulting in the sterilisation of about 300,000 tonnes of ore which impacted the volumes of tonnes delivered to surface stockpiles during the period.

In all, 95,569 tonnes of ore was treated at a grade of 21.8cpht which recovered 20,876 carats. This compared unfavourably to the 132,125 tonnes at a grade of 26.7cpht and 35,283 carats in the same period of last year. The reason for this is that 77% of the ore was sourced from areas close to the contact zone of the Kimberlite pipe where there was dilution of ore as Block 1 was mined out. The establishment of Block 2 production stopes is progressing according to plan.

Work practices adopted to manage the water underground have proven effective and the development of the level 2 production level has started and is progressing in line with the plan to maintain production flexibility into 2017. During Q2, work was performed to optimise the performance of the mill which resulted in higher mill retention times and better diamond liberation. This increased the number of stones recovered in the smaller size fraction during the period and initiatives to further improve the overall efficiency of the processing plant continues. The downsizing activities progressed during the period with the operation now structured to produce at the targeted rate of 300,000 tonnes per annum.

Development of the Ghaghoo mine continues to progress with the implementation of the previously announced strategy to reduce the tonnage and associated cost structure. Despite some initial headwinds experienced in the retrenchment process where a court in Botswana ordered the reinstatement of twenty workers, and the costs associated with the premature caving experienced in 2015, it is expected that the targeted monthly cost rates will be achieved in the second half of the year. The sales of the mine’s diamonds have been impacted by the cautious state of the diamond market. Two sales were concluded during the period for $4.8M, achieving an average of $157 per carat compared to an average of $210 per carat in the first half of last year.

As a result of the continued market uncertainty, the ongoing difficult market conditions for Ghaghoo’s production, the recent strengthening of the Botswana pula against the dollar and the changes in the operation reaching targeted production rate, it was decided that an impairment of the Ghaghoo asset was appropriate. They recognised an impairment charge of $40M and although the group has taken a number of steps to respond to these conditions such as downsizing the operation and reducing cash spend, the impact and benefit of these steps have not yet been realised. The valuation remains sensitive to market conditions impacting price and any adverse changes could result in additional impairment.

Ghaghoo has still not reached commercial production so the costs are currently just capitalised, meaning the profits are probably overstated somewhat. Going forwards, the focus will be on further optimising the downsizing and managing costs to limit cash burn; continuing underground development on level 2 to ensure sustainable production at the planned rates; enhancing mineral resource data through sampling ore from VK Main; continuing plant efficiency initiatives to improve throughput; monitoring market conditions to assess expansion options; and continuous improvement of HSSE practice.

All of the group’s other major currencies were weaker against the US dollar during the period which positively impacted the dollar reported costs. The operating cost per tonne treated declined by 19% to $14.26 but in local currencies, these costs grew by 5% so it is having a substantial effect.

Letseng remained cash generative and as mining moves into the higher-value area of the Satellite pipe in H2, the cash generation is expected to improve. The focus at Ghahoo going forward will be on cost optimisation and a reduction in cash consumption.

At the current share price the shares are yielding around 5% which remains broadly the same on the full year forecast, although whether the group should be paying a dividend at all is debatable.

Overall then this has been a difficult period for the group. Even excluding the impairment profits were down, net assets fell and the operating cash flow reduced with no free cash being generated. The diamond market is cautious at the moment and Ghaghoo in particular has really been suffering. With sales prices falling from $210 per carat to $157, the mine is being downsized and has been partially impaired. There is still no sign of it entering commercial production.

Things have also been rather difficult at Letseng as moving to a different part of the satellite pipe meant that less large stones were recovered, meaning the average sales price fell from $2,264 per carat to $1,899. This was also coupled with some bad weather which increased costs as power supplies were interrupted. The good news is that the group are now mining a different part of the satellite pipe which is producing better diamonds. Despite this, the poor diamond market and the issues at Ghaghoo mean it is difficult to justify a purchase here.

On the 10th November the group released a trading update covering Q3. Whilst the overall mood of the market remains cautious, the demand for Letseng’s high quality large white diamonds has continued as prices achieved for them remained firm during the period. During the quarter, 6.6 million tonnes of waste was mined, down by 20% on last quarter as a result of the extreme weather experienced in July and August when the mining fleet was not able to mine waste for a ten day period.

Letseng treated a total of 1.4MT of ore during the period, 77% of which was sourced from the main pipe. The impact of the poor weather was partially mitigated by the ore being sourced from stockpiles on the surface, as access to the pits was unattainable, which led to a reduction in the grade recovered and the number of carats recovered fell by 17% year on year and 15% when compared to Q2 to just 24,388. These stockpiles are planned to be replenished before next winter.

Three tenders were held during the period with 37,990 carats sold for a total value of $61.54M, achieving an average price of $1,619 per carat. This lower price is a consequence of a continued deficiency of high quality large diamonds rather than a decrease in demand for these diamonds or a weakening of the market and overall, prices of the production sold during the sales period remained firm.

There were no sales of Ghaghoo goods during the period. The actions required to reduce tonnage have been completed and at the same time the costs are on a downward trend. Development of level two is continuing, however. The extension of the water bearing fissure has been encountered on level two as expected. The water has been contained by adopting practices implemented on level one and there has been no impact on production during the period.

Ore treated increased by 21% quarter on quarter to 54,337 tonnes. Planned changes to the mill configuration have been finalised and will be implemented in late November, during a planned three day shutdown. The expected improvements will have a positive impact on throughput, liberation and mill retention time.

The grade recovered during the period was 14.2 carats per tonne. This lower than forecast grade was impacted by several issues. Firstly, owing to the lower than expected tonnes treated, the mining mix was not what was planned, therefore, lower grade material was treated. Dilution was also a factor – the main source of the basalt dilution is from internal waste that has previously not been mapped. The amount of diluted material was significantly higher than anticipated but recently has seen a notable reduction in basalt dilution. Given the current market conditions for the type of diamonds that Ghaghoo produces, the ongoing development of the mine in the near term is under review.

Overall then these are fairly difficult times for the group. The Ghaghoo mine is just not financially attractive in the current market and although the price is holding up well, a lack of large diamonds at Letseng means less is being made of that mine too. Added to this the poor weather conditions, and this has been a rather weak quarter for the group and I am not rushing to buy these shares at the moment.

The overall mood of the diamond market continues to remain cautious. Demand for Letseng’s large high quality diamonds have remained firm throughout the period but the smaller commercial diamonds mined at Ghaghoo remain under pressure. The recent Indian demonetisation and high levels of polished inventory available, and because the supply of this category of diamonds will increase significantly from production of some 7M carats per annum from 2017 from several new mines, the group believes that prices for this category may remain constrained.

On the 6th February the group released an update covering trading in Q4. At Letseng, the total ore treated increased by 5% to 1,697,070 tonnes and the group recovered 26,438 carats, an 8% increase over last quarter. Seven diamonds sold for more than $1M and $109,677 per carat was achieved for a 12.31 carat pink diamond. The average price achieved per carat was $1,444, well below the $1,695 achieved in the year are a whole and a 5% reduction on last quarter as they recovered fewer large special diamonds than expected.

As mentioned, during 2016 the frequency of exceptional large diamonds being recovered was lower than expected. Following a review of the resource and operational processes, it was considered that the lack of these stones is due to the normal short term variability of the resource as was experienced during 2012. This is expected to revert to normal recovery levels in the near future. In addition, options are being assessed to further enhance recovery and reduce damage to these diamonds through a large diamond specific recovery plant. A review of the Letseng mine is currently being undertaken to further optimise the waste mining profile which will improve cashflow. This will be completed during Q1 2017 and is likely to lead to reduced waste tonnes mined.

At Ghaghoo, 67,466 tonnes of ore was treated and 12,380 carats were recovered, an increase of 60% over Q3 with a higher number of larger diamonds than typically found. During the period, 16,989 carats were sold, achieving an average price of just $142 per carat. The future of the operation remains under review with a decision scheduled to be made during Q1 2017 with regards to its current financial viability. Mill modifications yielded positive results with increased diamond liberation. They are not sufficient to sustain the operation, however, given current weak prices achieved for the diamonds.

At the year-end the group had a net cash position of $3.8M with $53.3M of undrawn available debt. So, things seem to be rather tough here. Letseng is going through a period of lower large diamonds – it is not exactly clear whether they are being found and broken or just not being encountered. Also, the bottom has fallen out of the commercial quality diamond market like those found at Ghaghoo and from the sound of it there is not much prospect of a recovery any time soon. It seems to be that this mine is likely to be mothballed with will no doubt lead to some hefty impairments. I am staying clear of this for now.

On the 16th February the group announced that they decided to put the Ghaghoo mine on care and maintenance with immediate effect. They will continue to monitor market conditions for a time when starting full production would make economic sense. It is expected that after the one-off settlement costs, this will result in an annualised care and maintenance cost of $3M. This is disappointing but not really that surprising to be honest.