Redrow has now released its interim results for the year ending 2017.

Revenues increased by £136M when compared to the first half of last year and after cost of sales grew by £97M the gross profit was £39M higher than last time. Admin expenses were up £5M which gave an operating profit some £34M higher. Finance costs declined by £2M but tax charges increased by £7M which meant that the profit for the period was £112M, a growth of £29M year on year.

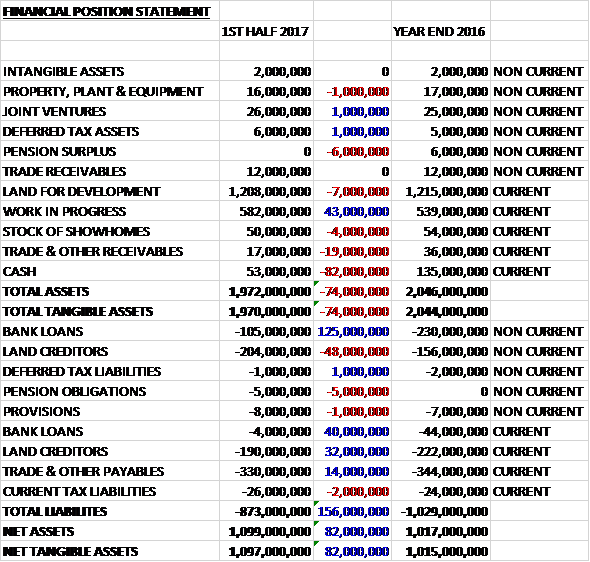

When compared to the end point of last year, total assets declined by £74M driven by an £82M fall in cash, a £19M decrease in receivables, a £7M reduction in land for development and a £6M elimination of the pension surplus, partially offset by a £43M growth in work in progress. Total liabilities also declined during the period as a £165M reduction in bank loans and a £14M fall in payables was partially offset by a £16M growth in land creditors. The end result was a net tangible asset level of £1.097BN, a growth of £82M over the past six months.

Before movements in working capital cash profits increased by £32M to £143M. There was a cash outflow from working capital but this was less than last time and after tax payments increased by £5M the net cash from operations was £105M, a growth of £102M year on year. There was no capex so this was all free cash which easily covered the £22M of dividend payments. The group also paid back £125M of loans so there was a cash outflow of £42M for the period and a cash level of £49M at the period-end.

Legal completions, including the Croydon JV, increased by 281 homes to 2,459 and for wholly-owned sites the increase was 238. The average selling price of the private homes increased by 12% to £344K, mainly due to geographic mix with 47% of turnover being generated in the South of the country as opposed to 38% last year.

Demand for new homes remains strong throughout the country on the back of improved mortgage availability and competitive mortgage rates. In the first half of the year, 865 of private reservations used Help to Buy, up from 746 in the same period last year. The value of private reservations increased by 13% on a like for like basis to £177M resulting in a record closing order book of £897M, up 35% on a like for like basis compared to the end of H1 2016.

The sales rate per outlet per week was up 5% which meant that a number of sites sold out earlier than expected. As a result, they were only operating 122 outlets at the end of the period compared to the 127 planned, although the number of outlets should increase in the second half subject to progressing a considerable number of sites through the planning process.

The group secured 1,760 plots for their current land holdings in the period. Of these, 1,352 were converted from the forward line pipeline. Over the same period the pipeline has remained unchanged with the potential for 25,600 plots with the land transferred to current land holdings being replaced by new additions.

In February the group purchased Radleigh Homes, a regional housebuilder based in the East Midlands which will give the group a new division in this area. The business completed 188 homes in 2016 and has a pipeline of over 1,300 plots with planning and a further 1,200 plots controlled under options in its strategic land pipeline.

The board are updating their medium term guidance as a result of the strength of their order book and sales rate, the recent acquisition and lower net debt expectations. In 2019 they expect to deliver turnover of £1.9BN, an operating margin of 19.5% and EPS of 77p. They enter the second half of the year with a record order book with many of their sites sold five to six months in advance. The strong advance sales have the effect of limiting availability but customer traffic and sales remain robust and the rate of sales since the start of 2017 at 0.73 is in line with last year.

At the current share price the shares are trading on a PE ratio of 8.9 which falls to 7.5 on the full year consensus forecast. After a 50% increase in the interim dividend the shares are yielding 2.4% which increases to 3.1% on the full year forecast. At the period-end the group has a net debt position of £56M compared to £183M at the same point of last year but the board expect a modest rise in net debt in H2 as a result of the recent acquisition and the ongoing investment in the business.

Overall then this has been a strong period for the group. Profits increased, net assets grew and the operating cash flow increased with plenty of free cash being generated which enabled the group to pay back some borrowing. Operationally things seem to be going well with completions up, the sales rate remaining steady and the average selling price increasing, although the latter is due to a change in mix.

Although it is important to remain vigilant about the unsteady macroeconomic environment, the forward PE of 7.5 and sensible yield of 3.1% meant that these shares still look decent value and I remain a holder.

On the 16th February the group announced a couple of director share sales. Matthew Pratt sold 15,300 shares at a value of £75K and William Heath sold 2,800 shares at a value of £14K. Not massive sales but not great to see nonetheless.

On the 9th May it was announced that director Barbara Richmond sold 120,000 shares at a value of just under £700K. This is a substantial sale.

On the 24th May the group announced that director William Heath sold 16,326 shares at a value of £93K.