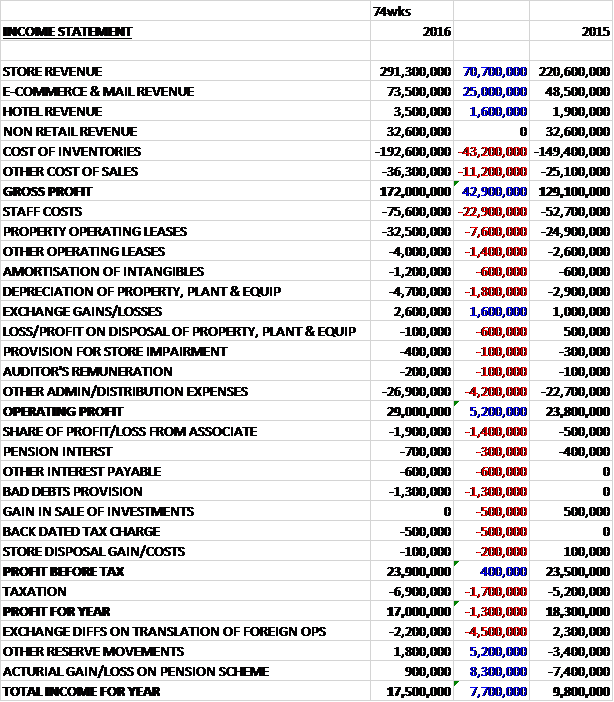

Laura Ashley has now released its final results for the year ended 2016. For some strange reason the group seems to have neglected to provide a like for like contrast so these results represent 74 weeks of 2016 and 52 weeks of 2015!

The gross profit increased by £42.9M and obviously admin costs increased, driven by a £22.9M growth in staff costs but there was a £1.6M increase in the exchange gain to give an operating profit £5.2M higher. The share of loss from associate increased by £1.4M and there was a £1.3M bad debt position along with a £500K back dated tax charge and the lack of a £500K gain on investment that occurred last year which meant that the profit for the period was £17M, a decline of £1.3M year on year.

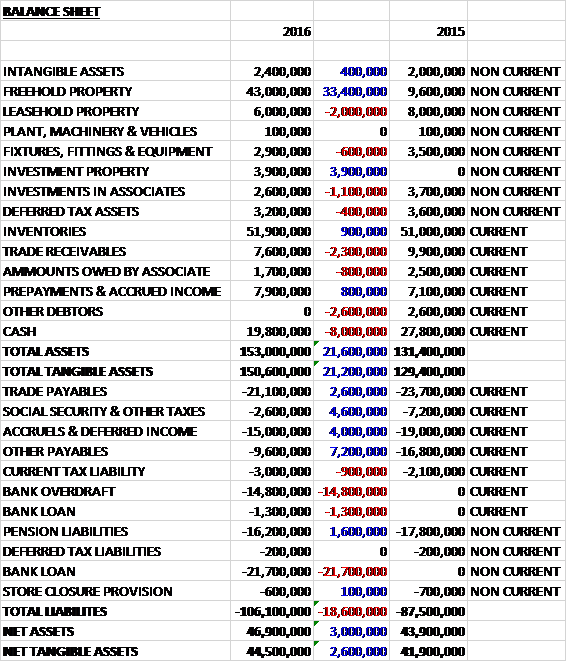

When compared to the end point of last year, total assets increased by £21.6M driven by a £33.4M growth in freehold property and a £3.9M increase in the value of investment properties, partially offset by an £8M decline in cash, a £2.6M fall in other debtors, a £2.3M decrease in trade receivables and a £2M decline in leasehold property. Total liabilities also increased during the period as a £7.2M decline in other payables, a £4.6M fall in social security and other tax payables, a £4M decrease in accruals and a £2.6M decline in trade payables were more than offset by a £14.8M growth in the bank overdraft and a £23M increase in bank loans. The end result was a net tangible asset level of £44.5M, a growth of £2.6M over the period.

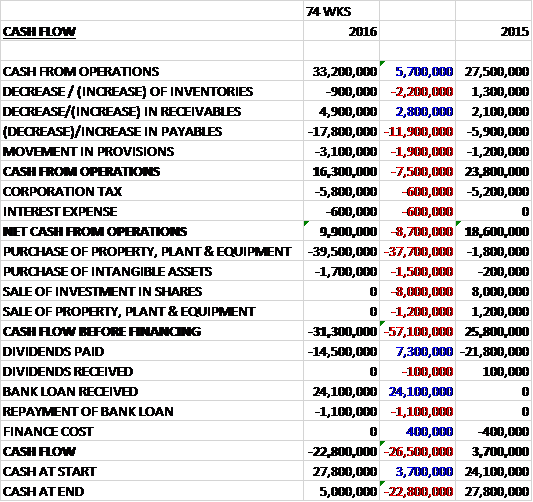

Again, a comparison with last year is nigh on impossible. Before movements in working capital, cash profits increased by £5.7M to £33.2M but there was a large cash outflow from working capital and after tax and interest payments both grew by £600K each, the net cash from operations came in at £9.9M, a decline of £8.7M year on year. This was totally dwarfed by the £39.5M spent on property, plant and equipment so after the group also spent £1.7M on intangible assets, there was a cash outflow of £31.3M before financing. The group paid out £14.5M in dividends it couldn’t really afford and after they took out a net £23M in new loans there was a cash outflow of £22.8M and a cash level of just £5M at the period-end.

Overall like for like sales grew by 4.1% with like for like e-commerce sales up 15.7%. During the period five stores were opened in the UK and eighteen closed, reducing total selling space by 4.2%. Furniture sales saw like for like growth of 4.3% with the availability of financing products helping the category to grow. Home accessory sales saw like for like growth of 6.8% based on new range additions, new product categories such as cookware and kitchen products as well as an enhanced seasonal offering. Decorating sales saw like for like growth of 1.6% and fashion sales were up 2.2% on a like for like basis as the group have started to partner with selected British retailers to give broader exposure to the ranges.

The profit from stores was £16.3M on a pro-rate basis, a decline of £3.3M year on year. The profit from e-commerce and mail order was £12.2M, a growth of £2.6M year on year. The loss from the hotel was £300K, an improvement of £100K when compared to last year.

Overseas there were 252 franchise stores compared to 303 at the start of 2015. Franchise and licensing revenue declined by £500K primarily due to the performance of a sluggish Japanese market and continued political instability and economic difficulties in other territories. During the period the group incurred an exceptional charge of £1.3M following a license partner in Australia being placed into administration. They have now signed a new license partner for the country and the board are confident that the business opportunity there will be optimised.

Trading for the first six weeks of the New Year is performing in line with management expectations.

On the 21st October the group announced that following the acquisition of Homebase by Wesfarmers, they will cease to trade in its concessions within the stores with the closures taking place in Q2. They do not expect there to be a material impact on the group and expect that the majority of trade they receive from the concessions will be redirected to other Laura Ashley stores and the website – it rather begs the question of why they had them in the first place if that is the case!

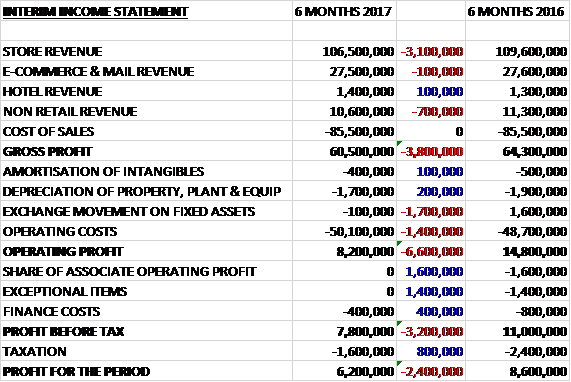

Laura Ashley has now released its interim results for the year ending 2017.

Revenues declined when compared to the first half of last year due to a £3.1M fall in store revenue and a £700K decrease in non-retail revenue. Cost of sales remained stable so the gross profit fell by £3.8M. Depreciation and amortisation decreased by £300K but there was a £1.7M detrimental movement of the effect of forex changes on fixed assets. Other operating costs were up £1.4M which meant that the operating profit declined by £6.6M. The losses from associates were eradicated this time, which accounted for £1.6M last year; there were no exceptional items, which were £1.4M last time and finance costs fell by £400K. Tax was also down, decreasing by £800K to give a profit for the period of £6.2M, a decline of £2.4M year on year.

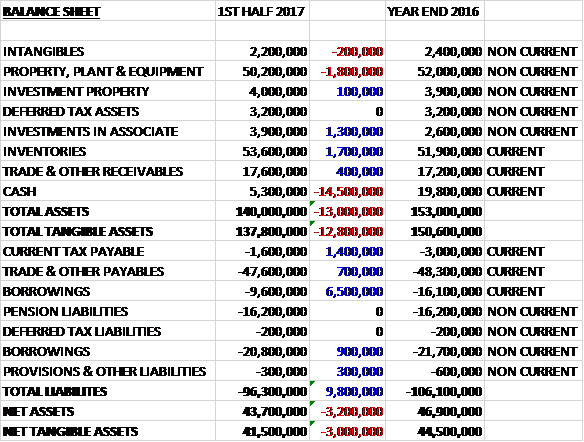

When compared to the end point of last year, total assets increased by £13M driven by a £14.5M decline in cash and a £1.8M decrease in property, plant and equipment partially offset by a £1.7M growth in inventories and a £1.3M increase in investments in an associate. Total liabilities also declined during the period due to a £7.4M decrease in borrowings and a £1.4M fall in current tax payables. The end result was a net tangible asset level of £41.5M, a decline of £3M over the past six months.

Before movements in working capital, cash profits declined by £3.5M to £10.1M. There was a cash outflow from working capital compared to an inflow last time and after tax payments increased by £700K the net cash from operations came in at £3.9M, a decline of £10.4M year on year. The group spent just £200K on capex so there was a free cash flow of £3.7M. This didn’t come close to covering the £10.9M of dividends paid out and after £700K of the bank loan was repaid there was a cash outflow of £7.9M and a cash level of -£2.9M at the period-end.

Margins have been affected in the period due to adverse currency rates and underlying cost increases due to the rise in the national living wage. Some 22 concession stores in Homebase will be closed by June following its acquisition by Bunnings. Actions are being taken to minimise the impact to profit of the closure of these concessions, although the board have previously stated that they don’t expect there to be a material effect.

The profit from stores was £6.1M, a decline of £5.9M year on year with like for like sales down 3.5%. Like for like furniture sales were down 8% although there was some performance in Q2. The new season product range has recently been launched and the early reaction is apparently encouraging so the board are hopeful of a stronger second half in this category. Like for like home accessory sales increased by 2.5% with the seasonal ranges being the most successful element. Decorating sales were down 6.4% but again the board are pleased with the early reactions to the new ranges. Like for like fashion sales were down 3.2%.

The profit from e-commerce and mail order was £6.8M, a growth of £300K when compared to the first half of last year as like for like sales grew by 2.1%. The group also continue to improve their reach and after already delivering to eight European countries they have added delivery to the Czech Rep and Hungary. New payment solutions will be added to the online platforms in Germany, Benelux and France over the coming months. The group also launched their digital platform in China in November which will continue to be developed during the current year.

The profit from non-retail activities was £5.4M, a growth of £500K excluding the loss from associate that was not repeated this time. At the period-end the number of franchised stores were broadly stable at 251. The group signed a new license partner for the Indian market which positions the brand for advancing in this country and they also now have a presence in China having launched a website there in November.

The board feel that given the continued market challenges that pre-tax profit for the year will fall below market expectations. Like for like sales so far in the second half of the year are down 0.6%.

At the period-end the group had net debt of £2.9M compared to net cash of £5M six months ago. At the current share price the shares are trading on a PE ratio of 10.1 but this rises to 18.5 on the full year consensus forecast. With an interim dividend of 0.5p per share the shares are yielding 8.8% which falls to 7.3% on the full year forecast.

Overall then this has been a difficult period for the group. Profits are down, net assets fall and the operating cash flow reduced. Although some free cash was produced, this was no-where near enough to cover the dividends. There are a number of issues affecting the group with the decline in the value of sterling pinching margins in the UK, along with the application of the national living wage increases. The group are also having to contend with the removal of their concessions from Homebase stores and I don’t really believe the board when they say that will have no real effect.

The profit for this year is coming in below expectations and although there is a stonking dividend yield of 7.3%, the forward PE of 18.5 suggests to me that this is not sustainable on the current trading and it is hard to see where a recovery is going to come from unless the overseas sales really take off. I am steering clear for now.