Finsbury Food has now released their interim results for the year ending 2017.

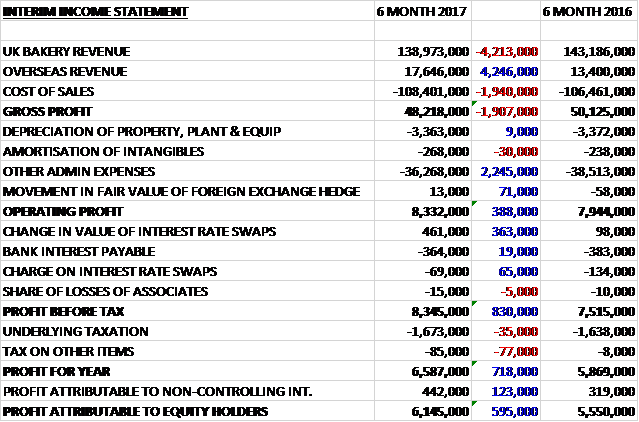

Revenues were broadly flat when compared to the first half of last year as a £4.2M decline in UK bakery revenue was offset by a £4.2M growth in overseas revenue. Cost of sales increased, however, so the gross profit fell by £1.9M. Admin expenses declined by £2.2M to give an operating profit £388K above last time. There was also a favourable £363K movement in the value of interest rate swaps and a £65K reduction in the charge on hedging items but tax charges increased by £112K to give a profit for the period of £6.1M, a growth of £595K year on year.

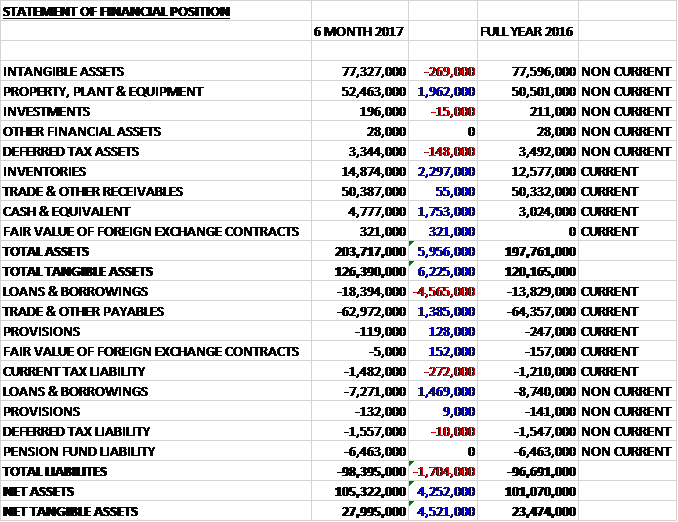

When compared to the end point of last year, total assets increased by £6M to £203.7M driven by a £2M growth in property, plant and equipment, a £2.3M increase in inventories and a £1.8M growth in cash. Total liabilities also increased as a £1.4M decline in payables was more than offset by a £3.1M growth in borrowings. The end result was a net tangible asset level of £28M, a growth of £4.5M over the past six months.

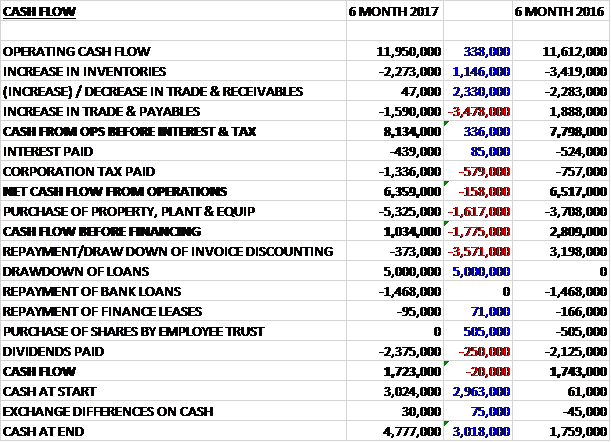

Before movements in working capital, cash profits increased by £338K to £12M. There was a cash outflow from working capital, but this was broadly the same as last time although tax payments grew by £579K to give a net cash from operations of £6.4M, a decline of £158K year on year. The group spent £5.3M on capex which gave a free cash flow of £1M. This did not cover the £2.4M paid out in dividends wo the group took out a net £3.5M of new borrowings to give a cash flow of £1.7M for the half year and a cash level of £4.8M at the period-end.

The underlying operating profit in the UK Bakery business was £7.4M, a growth of £159K year on year. The grocery cake market saw a year on year volume decline of 4.8% and a value decline of 1.5%, and the bread and morning goods grocery market sees year on year volume growth of 0.6% and a value decline of 0.2%. In cake, the group have followed the market. Celebration continues to perform but round cake has seen declines on the back of lower promotional activity, a common response to higher input prices. In bread the group’s focus is on more niche style bakery products as opposed to traditional bread and therefore revenue exceeded the market performance.

The UK bakery operating profit margin has increased to 5.3% due to operational efficiencies within the factories and includes the benefit of significant capex over the last two years. The group will continue to invest in automation and operational improvements to increase product capabilities and maintain margins.

The underlying operating profit in the overseas business was £968K, an increase of £200K when compared to the first half of last year. The business is heavily exposed to the Euro which has had a favourable impact on sales and profits. In Euro terms the business has performed well too, however.

The UK grocery market continues to be challenging even though the wider economic environment is improving slowly. Increasing commodity prices, the adverse impact on exchange rates and the national living wage means the group is working hard to mitigate input cost inflation through continued operational efficiency, investment in automation and price increases, all of which are ongoing. Despite this, the board expect the group’s steady performance to continue into the second half of the year.

At the current share price the shares are trading on a PE ratio of 17.7 which falls to 10.8 on the full year consensus forecast. At the period-end the group had a net debt position of £21M compared to £19.7M at the prior year-end. After a 7.5% increase in the interim dividend the shares are yielding 2.7% which increases to 2.8% on the full year forecast.

Overall then this has been a pretty decent performance in a tough environment. Profits were up, net assets increased and although the operating cash flow fell, this was due to an increase in tax payments and cash profits grew. There was some free cash generated, although this did not cover all of the dividends. The UK bakery business is performing OK with a decline in the market for cake being offset by growth in niche bread and some cost cutting. In Europe, the business is being aided by the weak pound.

The weak pound, however, is the source of some pressure for the group. This along with the living wage and some other issues mean that going forward times are going to be tough and the group are likely to have to put prices up. The forward PE of 10.8 looks decent enough, however, so although this is a tough time for the group, this may be valued in already?

On the 7th April the group announced that non-executive director Zoe Morgan purchased 49,047 shares at a value of £52K. Following the purchase she holds 70,028 shares in the company.

On the 17th July the group released a trading update covering the full year. Total company sales revenues grew to £314.3M, a like for like increase of 0.3% and the group is confident of delivering profits in line with market expectations. On a constant currency basis, revenues declined by 1.1% like for like.

Against a backdrop of UK retail food market deflation, the UK bakery division declined by 1.4% like for like but this improved through the year with a 2.9% decline in H1 turning into a 0.1% increase in H2. The overseas division grew by 17.3%, made up of 15.1% exchange rate benefit and just 2.2% organic growth. As noted previously, industry-wide challenges has necessitated price rises and as such the group has had “productive” discussions with its customers during the period. They continue to monitor the need for further action in light of unusual cost spikes, as is currently the case with butter.

This update really reiterates what a sluggish state the market is in at the moment. Whilst this remains a good company in my view, I just think there are too many headwinds to invest at this time.

On the 23rd August the group announced that it is proposing to close their Grain D’Or business, a provider of premium baked goods for the pastry sector based in London. The business has been historically loss making and despite a range of initiatives to improve the business, it still made a loss this year. So, fair enough then.