Molins has now released its final results for the year ended 2016.

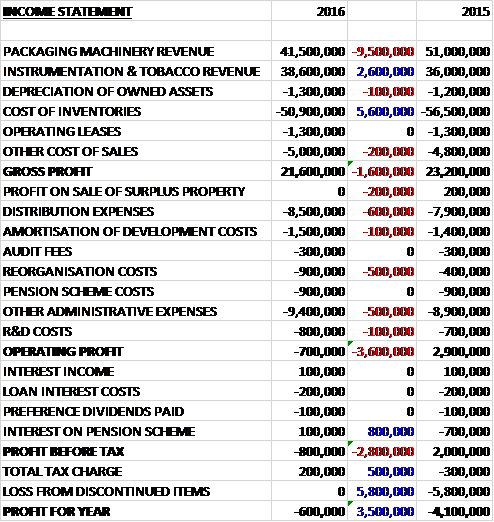

Revenues declined when compared to last year as a £2.6M growth in instrumentation and tobacco revenue was more than offset by a £9.5M decline in packaging machinery revenue. Cost of inventories declined by £5.6M but other cost of sales were up modestly to give a gross profit £1.6M below that of last year. Distribution expenses grew by £600K and reorganisation costs were up £500K with other admin expenses increasing by £600K which meant that the operating loss saw a detrimental movement of £3.6M. There was, however, an £800K positive swing to an interest income from the pension scheme and tax charges saw a positive movement of £500K which gave a loss for the year of £600K, a detrimental movement of £2.5M year on year.

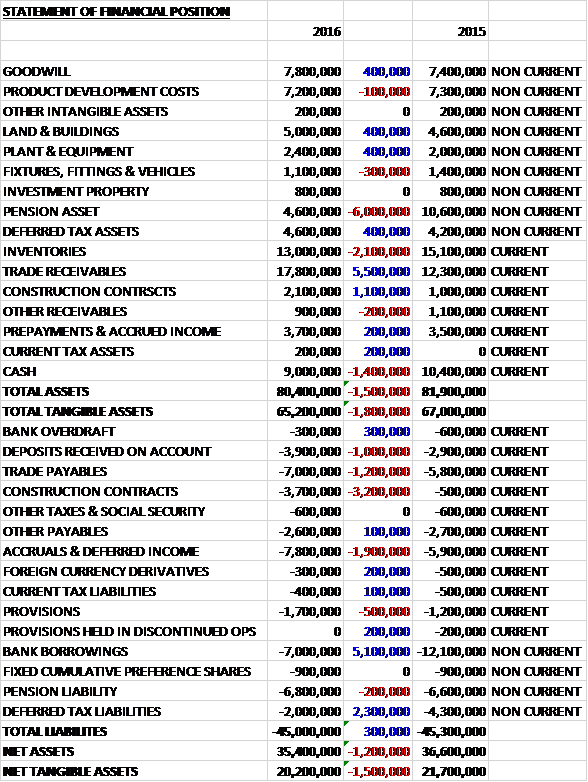

When compared to the end point of last year, total assets declined by £1.5M to £80.4M driven by a £6M decrease in the pension assets, a £2.1M fall in inventories and a £1.4M decline in cash, partially offset by a £5.5M growth in trade receivables and a £1.1M increase in construction contracts. Total liabilities saw a modest decline as a £5.1M fall in bank borrowings and a £2.3M decrease in deferred tax liabilities was mostly offset by a £3.2M increase in construction contract payables, a £1.9M growth in accruals and deferred income, a £1.2M increase in trade payables and a £1M growth in deposits received on account. The end result was a net tangible asset level of £20.2M, a decline of £1.5M year on year.

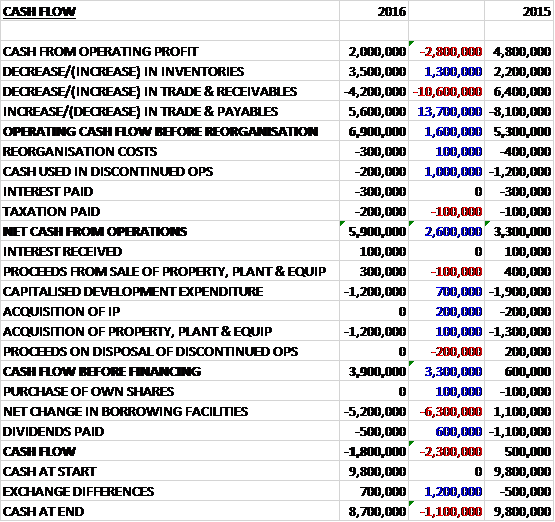

Before movements in working capital, cash profits declined by £2.8M to £2M. There was a cash inflow from working capital, however so the operating cash flow of continuing operations increased by £1.6M. The group spent £1M less cash in discontinued operations so the net cash from operations was £5.9M, a growth of £2.6M year on year. The group spent £1.2M on development expenditure and £1.2M on property, plant and equipment to give a free cash flow of £3.9M. Of this, £500K was paid out in dividends and £5.2M was used to pay back loans so there was a cash outflow of £1.8M and a cash level of £8.7M at the year-end.

The underlying operating profit in the Packaging and Machinery division was £700K, a decline of £3.2M year on year. The division started the year with a lower order book and although a large number of projects were discussed, conversions to orders were delayed and the operational efficiencies of the business suffered through under-utilisation. Towards the end of the year, the group reduced the cost base of the division which helped position the business more effectively for 2017.

Order intake in the last few months of the year started to improve, across all of the regions and most of the sectors. Overall order intake improved by 40% (28% at constant currency) leading to a significantly improved order book as they enter 2017. Order prospects remain positive and the division received a valuable pharmaceutical-related order in January 2017, although the board remain cautious until they see a longer trend of sustained order intake.

The underlying operating profit in the Instrumentation and Tobacco Machinery division was £400K, a growth of £300K when compared to last year. The increase arose from the instrumentation business entering the year with a stronger order book and converting that to sales. Overall order intake in the year was at broadly similar levels to the year before but order intake for services increased in the year.

Demand within the tobacco machinery business remained low for new machinery but the board remain encouraged by their introduction to the market of the Alto cigarette making machine and the Optima cigarette packing machine. The Optima machine is nearing the end of its field trials, the results of which have been very positive and enables them to market the product knowing that it is a strong machine that is taking them back into the cigarette packing market. The product portfolio of this division is strong and largely complete, and the focus is now on selling those products.

The group have continued to take steps to improve the efficiency of the division and have removed costs from some of the regional centres. Headcount reduced by a further 9% following a 20% reduction the year before.

Following the change in leadership the group is looking to develop their service offering and they have also changed their sales regions to the Americas, EMEA and Asia Pacific. Further investment will be made to support the growth markets with products which complement the product portfolio and broaden the customer base in their target markets. These investments are expected to be principally funded through cash generation by the group.

The pension schemes remain a major issue here and the value of the schemes liabilities currently stand at £397.3M with the main cause of the increase due to a decrease in the discount rate, reflecting lower interest rates at the year-end compared with the prior year. The level of deficit funding is currently £1.8M per annum, increasing by 2.1% per year with an estimated recovery period of 13 more years or so.

This year the non-underlying costs related to £900K of administration costs for the defined benefit pension scheme (these costs recur every year), reorganisation costs in the packaging machinery division of £800K, and instrumentation division of £100K.

Although trading was not strong during the year, emanating from a low order book as the group entered the year and the impact of delayed customer investment decisions during most of the year, order intake improved in Q4 and increased by 20% overall compared to the prior year, leading to a significantly higher order book as the group enters 2017.

As the group was loss making over the past year, there is no PE ratio but this is a cheap-looking 5.3 on next year’s consensus forecast. At the year-end, the group had a net cash position of £800K compared to a net debt position of £3.2M at the end of last year. It was decided not to declare a dividend this year.

Overall then this has been a difficult year for the group. They swung to a loss, net assets declined and cash profits fell. The cash generation, however, was actually pretty good with operating cash flows improving and some free cash being generated, although this was entirely due to favourable working capital movements. The Packaging and Machinery division saw a big fall in profits as less orders were received and some were delayed. The Instrumentation division did see a modest improvement but still remained subdued.

Going forward, however, I think things look a bit better. The new CEO seems to have injected some much needed umph to proceedings and the development of a services business looks to be sensible. The order intake has also much improved since the start of last year and with a forward PE of 5.3 this is looking rather tempting now.

On the 8th June the group announced that it had entered into an agreement with Coesia (GD) to sell their instrumentation and tobacco machinery division for a gross cash consideration of £30M. The net proceeds of the sale, expected to be £27.3M and similar to the book value of net assets being sold, will be used to invest in the group’s packaging machinery activities and to strengthen the balance sheet, leaving it in a net cash position.

The tobacco industry is undergoing a transformation with the introduction of vaping products set to progressively displace sales of traditional cigarettes. This change will require significant and timely investments in new product development.

The group has agreed to transfer the name “Molins” to GD following completion but they will retain the right to use the name for a period of six months after which they will have to change their name and remove all associated Molins branding.

Following the sale, with a strong order intake in the last few months of 2016 continuing in the first five months of 2017, the board believes the division is well placed to match 2015’s sales levels. Whilst the division’s profitability will, in the short term, be impacted by the allocation of all the group’s central costs, the impact of this is expected to be dissipates as the group grows. The first part of the year has resulted in order intake being at levels ahead of the same period last year.

In particular, order intake in the continuing group at the end of May was considerably ahead of order intake for the same period last year. Trading is as expected and ahead of last year in all parts of the continuing group so the sales in 2017 are likely to be significantly ahead of last year.

The group has agreed to make a one-off contribution to the pension fund of £2.7M and will continue to pay £1.8M per annum. If underlying operating profit in any year is more than £5.5M, the group will pay to the fund an amount of 33% of the difference between the profit and £5.5M.

Overall this seems to be a good deal to me. To be able to sell a division that needs a lot of investment to remain competitive for its net asset value seems like a very good thing and I am glad I bought in here (for now!)

On the 27th June the group released a trading update covering the first half of the year. They group entered 2017 with a strong order book that was substantially stronger than the start of 2016 with the increase arising in the Packaging Machinery division. The first part of the year has resulted in order intake in all parts of the group being at levels ahead of the same period of last year. In particular the order intake in the continuing group at the end of May was considerably ahead of order intake for the same period last year. Trading is as expected and head of last year in all parts of the group.

The group also announced thay entered into an agreement to sell a manufacturing facility in Canada for a gross consideration of £6.7M payable in cash with net proceeds expected to be £5.9M, generating a profit on the sale of £4.4M. The group is to enter into a ten year contract to lease a newly built facility about eight miles from their current location, still in Ontario, from a third party at an annual cost of £350K. They are expecting to spend about £1M adapting the building to their needs.