Photo-Me has now released their final results for the year ended 2017.

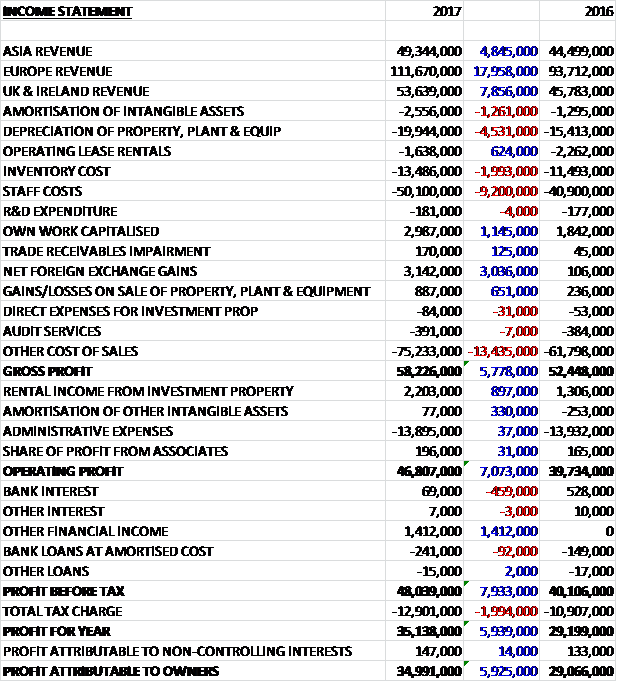

Revenues increased when compared to last year, mostly as a result of forex movements, due to an £18M increase in European revenue, a £7.9M growth in UK & Ireland revenue and a £4.8M increase in Asian revenue. Amortisation was up £1.3M, depreciation increased by £4.5M due to increased investment and the Asda acquisition, inventory costs grew by £2M due to forex movements and staff costs were up £9.2M. There was a £624K decline in operating lease rentals, a £1.1M increase in own work capitalised, a £3M increase in forex gains and a £651K growth in gains from the sale of assets, offset by a £13.4M growth in other cost of sales which gave a £5.8M growth in gross profits. There was an £897K increase from rental income and a £330K reduction in other amortisation to give an operating profit £7.1M above last time. Bank interest did decline by £459K but there was £1.4M of other financial income, offset by a £2M increase in tax charges, mostly relating to deferred tax. This all meant that there was an annual profit of £35M, a growth of £5.9M year on year.

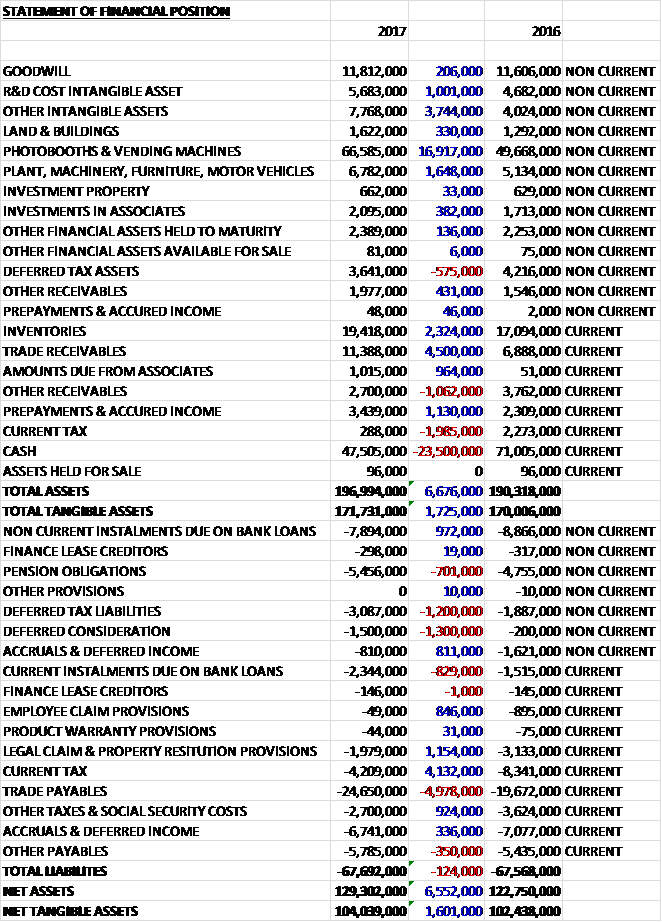

When compared to the end point of last year, total assets increased by £6.7M driven by a £16.9M growth in the value of photobooths, a £4.5M increase in trade receivables, a £3.7M growth in intangible assets and a £2.3M increase in inventories partially offset by a £23.5M decline in cash. Total liabilities saw a modest increase as a £4.1M decline in current tax liabilities was more than offset by a £5M increase in trade payables, a £1.3M growth in deferred consideration and a £1.2M increase in deferred tax liabilities. The end result was a net tangible asset level of £104M, a growth of £1.6M year on year.

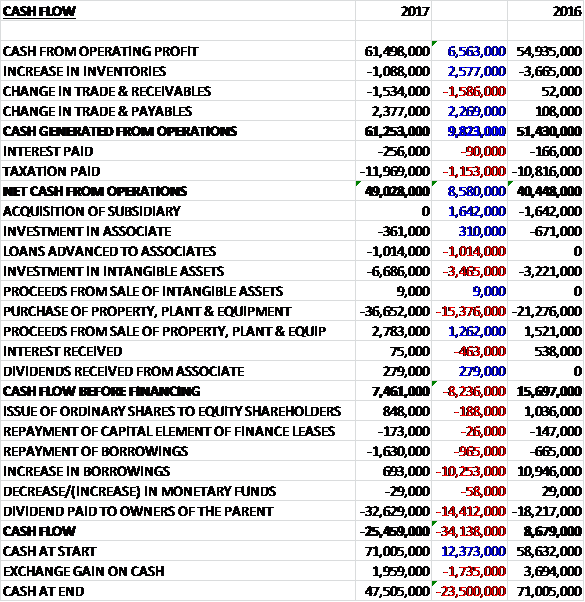

Before movements in working capital, cash profits increased by £6.6M to £61.5M. There was a broadly neutral working capital position compared to a cash outflow last year and after tax payments increased by £1.2M there was a net cash inflow of £49M, a growth of £8.6M year on year. The group loaned £1M to an associate, spent £6.7M on intangible assets and £36.7M on tangible fixed assets which meant there was a free cash flow of £7.5M. This didn’t come close to covering the dividends of £32.6M and there was a cash outflow of £25.5M and a cash level of £47.5M at the year-end.

Although profits were up nearly 20%, the majority of this was due to favourable forex movements and at constant currency they increased by 4.2%.

The operating profit in the Asian business was £8.6M, a decline of £2.1M year on year due to lower volumes in Japan following the government’s decision not to enforce the My Number card scheme immediately. At the end of the year, there was an increase of 708 units, of which 679 were photobooths. Although revenues increased, at constant currency they declined by 12% although sales in China and Korea increased by 28% and 45% respectively.

Contributions from the Japanese government’s My Number ID card programme were lower than initially expected as the ID cards are not mandatory and adoption has not been as rapid as the government expected. The new card is expected to become compulsory by 2021. The group opened its first laundrette ship in Japan.

The operating profit in the European business was £33.9M, an increase of £9.8M when compared to last year primarily driven by growth in the laundry division with photobooth revenue contracting by 0.7% at constant currency levels. The group are now entering the Italian market, focusing on laundry and digital kiosks.

In France they have invested to upgrade the vast majority of photobooths to enable the direct transmission of digitised e-photo and e-signature to the ANTS secure database for driving licence applications. In Germany, their secure data capture and transfer technology is fully certified by the authorities and they have started the rollout of this technology. In the first half of the year they implemented price increases in their photobooths in the Netherlands and Switzerland.

The expansion of the laundry business in Europe has continued, focusing on France, Belgium and Portugal. In Portugal, laundry operations now account for over 60% of revenue from the country compared to 13% in 2015. During the year 27 laundrette shops were added to the estate and results from these sites have been solid. Production of the new compact Revolution machines started in March and the board expect them to be more attractive to Far Eastern markets.

The number of digital printing kiosks increased by 3%, primarily driven by the gradual rollout of the new Speed Lab Cube and Bio kiosks. They have started the deployment at Carrefour, replacing Kodak units and so far results have been encouraging. They currently operate 20 Money Gram kiosks and a further 80 transaction kiosks in France. They are in discussions with Money Gram to extend this partnership to other territories.

The operating profit in the UK and Ireland business was £7.3M, a decrease of £653K when compared to 2016 as a result of start-up costs associated with the newly formed retail business (the acquired Asda stores business) which contributed a £1.8M loss. Without this, profits grew on revenues that increased by 16% driven by a doubling of sales from the laundry business.

The number of photobooths remained flat but there was a 787 increase in other units. The number of digital kiosks increased by 737 to 992 after introducing the SpeedLab cube at Morrisons and Asda. The laundry estate increased by 57% to 499 operated units. Fowler, the commercial laundry and catering equipment business made a contribution of £700K. In March the group launched the rollout of their encrypted photo ID technology across Ireland in partnership with the government. This agreement, which leverages the technology developed for the French government, provides customers with a system for the digital transfer of ID photos as part of the online passport application service.

The group is the first company licensed to capture and transfer digital photos as part of the new online passport renewal system in Ireland. The phobooths are being rolled out with Topaz, Super Valu, Tesco and An Post as well as a number of shopping centres. Upon completion of the rollout, expected by the end of 2017, 98% of the population will live within 5km of a unit. During the year a £1 price increase was implemented in the London area.

The group has now started deploying Revolution laundry units at suitable sites in the UK with 70 units deployed during the year in petrol station forecourts and other high footfall locations. Following the acquisition of the UK photo division of Asda, the addition of 363 sites, 191 photo centres and 172 self-service corners has extended their presence in the UK market. The reconfiguration of layouts and equipment upgrades which are being implemented as well as ongoing operational measures are expected to restore profitability to the business in the short term and expand profitability going forward. The group has also sited over 120 Speed Lab Cubes at Morrisons stores.

The laundrette business is making progress. The strategy is to acquire underperforming laundrette businesses located on attractive sites and refit the shop in a format that is more attractive to the end user. In the short to medium term the aim is to expand their presence in the laundrette market in Japan, estimated to be one of the largest markets in the world. The board also believes they can extend the Fowler business model to other geographies, particularly continental Europe.

In the UK the group is lobbying to propose a similar system to the ANTS system in France. While there may be a short term negative impact from the Brexit vote, in the long term potential re-nationalisation of UK identity documents as well as strengthening immigration regulations could lead to increased requests for the group’s products.

Going forward, despite a context of general uncertainty, the board expect another year of underlying progress as the new financial year has started in line with their expections. They will remain focused on driving profitability from their existing estate and investing in new products.

At the current share price the shares are trading on a PE ratio of 17.2 which reduces to 16.3 on next year’s consensus forecast. After a 20% increase in the total dividend, the shares are yielding 4.4% which increases to 5.3% on next year’s forecast. At the year-end the group had a net cash position of £39.2M compared to £62.4M at the end of last year.

Overall then this has been a solid year for the group. Profits and net assets both increased but this was mainly due to favourable forex movements and the underlying growth was rather slower. The net cash flow increased with some free cash being generated but this is not close to the amount needed to cover the dividend. The Asian business suffered, apparently due to the Japanese ID cards not being compulsory and the UK/Irish business also saw declining profits but this was due to costs associated with the Asda store acquisition and underlying profits increased with Fowler making a decent contribution too.

The only area to see profit growth was Europe which was driven by the continued rollout of the laundry units. Going forward the PE of 16.3 and yield of 5.3% is probably about right although that dividend needs some more cover in my view. I continue to hold.

On the 17th July the group confirmed the completion of the sale of its head office building in Bookham to Shanley Homes for a consideration of £2.5M. The book value of the land sold is £100K so they booked a profit of £2.4M on the sale. This disposal is part of the group’s review of its property portfolio in order to group the activities of its head office and UK operations into one location.

On the 25th November the group released an update covering the first five months of the year. The business have continued to perform as expected, with revenues also supported by favourable forex movements. Turnover improved by 11.2%, consistent with full year expectations, and cash generation remained strong.

In Photo ID, further progress has been made in the rollout of the encrypted photo ID upload technology. Since the Irish government launched the online passport application service in April, 178 upload enabled photobooths have been deployed and the group remained on track to roll out a total of 300 units by the end of April 2018. In the UK, discussions with the government to formally adopt the online passport have progressed, while expanded testing is ongoing. The group expects that the new service will be rolled out across the UK in early 2018.

The group continues to expand its presence in the laundrette market through the acquisition of underperforming businesses in attractive locations with particular focus on the Japanese market where it sees significant opportunity. In July they acquired Inox and Tersus, UK-based business to business laundry businesses which provide bespoke professional design, procurement and installation of laundry and catering facilities. They continue to look for bolt on acquisitions in this area.

Production of the Revolution laundry machine has now been transferred from Hungary to a new factory in Poland and as a result they are benefiting from enhanced capacity flexibility in production volumes.

Following the acquisition of the UK photo division of Asda last year, the group is reviewing the progress of these operations and re-shaping its digital printing operations to boost profitability, resulting in some restructuring of this business.

Whilst the board remain mindful of the macroeconomic environment, currency movements and consumer disposable income, which has led to some softening in the UK and Japanese markets, the group has continued to make good progress against its strategy and the board remains confident of the outlook for the full year.