Omega Diagnostics has now released their final results for the year ended 2017.

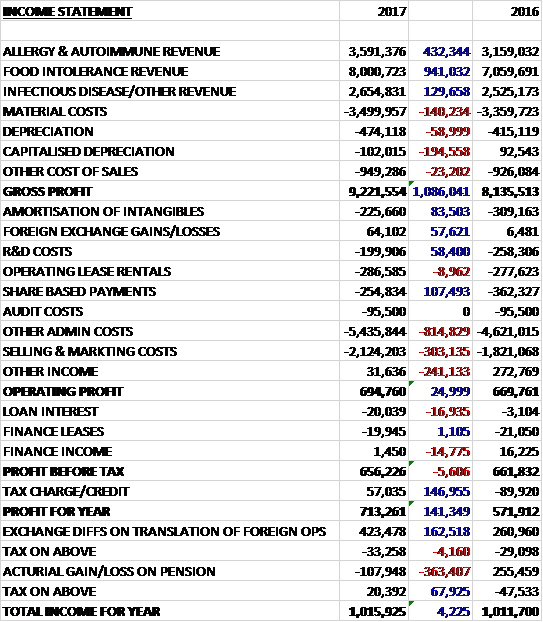

Revenues increased when compared to last year due to a £941K growth in food intolerance revenue, a £432K increase in allergy and autoimmune revenue and a £130K growth in infectious disease revenue. Material costs increased by £140K, depreciation was up £254K, partly as less was capitalised, and other cost of sales grew by £23K to give a gross profit £1.1M ahead of last year. Amortisation declined by £84K and share based payments were down £107K but other admin costs grew by £815K relating to a salary benchmarking exercise and management training programme, selling and marketing costs were up £303K due to a need to upskill the German sales management and other income fell by £241k as last year included the final amortisation of a grant received in 2014, which meant that operating profit increased by just £25K. Finance income fell by £15K and loan interest grew by £17K to give a pre-tax profit broadly flat but a £147K positive swing to a tax credit, mainly due changes in the over/under provision of tax, meant that the profit for the year was £713K, a growth of £141K year on year.

When compared to the end point of last year, total assets increased by £2M driven by a £2.2M growth in development costs, a £244K increase in prepayments and other receivables and a £366K growth in inventories, partially offset by a £622 decline in trade receivables and a £565K fall in cash. Total liabilities also increased during the year due to a £274K growth in deferred tax, a £238K increase in deferred income and a £228K growth in accruals and other payables. The end result was a net tangible asset level of £16.7M, a growth of £1.2M year on year.

Before movements in working capital, cash profits increased by £394K to £1.8M. There was a cash outflow from working capital but tax receipts reduced by £117K and there was a modest increase in finance costs to give a net cash from operations of £2M, a growth of £527K year on year. This didn’t quite cover the £2.1M of development costs and the £591K spent on property, plant and equipment so there was a cash outflow of £688K before financing. The group also paid out £142K in finance leases but received £163K from new finance leases which meant there was a cash outflow of £667K for the year and a cash level of £737K at the year-end.

The pre-tax loss in the Allergy and Autoimmune division was £455K, an increase of £77K year on year. Sales comprised of Allergy sales, up £460K to £3M, and autoimmune products, broadly flat at £560K. The allergy sales continue to be derived almost exclusively from the business in Germany where domestic sales increased by 3% in euro terms with the reported sterling increase being 15%.

Following the CE0-marking of 41 allergens the group have continued to develop further tests. A further 11 allergens have been optimised and they are on target to deliver another 20 this year. In addition to the Allersys programme, the Allergodip development pipeline has now been extended with the addition of four new panels. The introduction of a mobile phone app that allows quantification of the test result will assist in the marketing of the test to resource-poor countries with limited lab facilities.

The pre-tax profit in the Food Intolerance division was £3.1M, a growth of £565K when compared to last year. Sales of Food Detective reduced by 10% to £2.1M as the group took a conscious decision to reduce pipeline stocking in two of their key markets. Sales of Foodprint grew by 34% to £4.7M, however, with strong performances in Europe, North America and the Middle East. The group sold a further eight instruments in the year, taking the cumulative number of installations to 176 and revenue per instrument increased by 29% to £23K.

The CNS lab service showed an increase of 7% in sales to £620K, dominated by the markets in the UK and Ireland and they produced and sold 7,167 patient reports in the year, maintaining an average price of £86 per report.

Food Intolerance will continue to be a key growth driver and contributor to the bottom line. This has been reflected in the increase in operating and marketing resource to provide high level scientific support for the CNS product range. The growth trajectory is expected to continue with this core business supported by increasing the range of products and services in the health and wellbeing market, which now extends to 80 countries.

Management believe that there are further significant opportunities for growth in the business and have made progress in North America where customers are evaluating their products. In China they are in advanced discussions with a partner company which could provide access to a large market which is increasingly aware of food intolerance testing. In relation to the Food Detective product, the group has been in discussions with LRQA regarding use of the self-test version of the kit. They have agreed a timescale to complete some corrective actions to LRQA’s satisfaction but in the event that they are unable to achieve this, the CE-mark for the self-test kit will be suspended which will have a modest impact on profits – sounds ominous.

The pre-tax loss in the Infectious Disease business was £615K, an increase of £350K when compared to 2016. Sales were up 5% due to the weakening of sterling against the other currencies. In addition to the malaria rapid tests, they are also evaluating additional rapid tests for dengue fever, syphilis, leptospira, Brucella and S. Typhi.

The landscaper for CD4 testing has changed over the past six months. Amongst policy makers there has been a shift in strategy for utilising CD4 testing in the care of people living with HIV. This has resulted in a series of regional workshops being held across Africa that the group has been invited to participate in. The resulting output will see an increasing emphasis being placed on CD4 testing to help those people who present for care in the advanced stages of the disease with very low CD4 cell counts, representing about 30% of the overall HIV total. It is unclear to me exactly what this means for the group but it seems that it is a fast moving area and further delays would be very unhelpful.

The group achieved a significant milestone in attaining formal design freeze with their VISITECT CD4 test for monitoring the immune status of people living with HIV following the successful manufacture of three pilot batches. Devices from these batches were tested at three UK hospital sites on sufficient numbers of patients to demonstrate that they now have a method for manufacturing devices which consistently meet their design goal specs regarding sensitivity and specificity.

They have now moved into the validation and verification phase of the programme which can be summarised with the manufacturing of validation batches to confirm manufacturing robustness, utilising validation batches to verify performance; external performance evaluation trials and CE mark.

In India, in January the group received certificates of accreditation from BSI confirming their quality management system is compliant with various standards. In March they underwent an annual inspection from the Indian FDA confirming that the facility is compliant with GMO processes and they were issued with a manufacturing license which is valid until the start of 2021. They have launched three VISITECT malaria tests which are currently available for general sale through business to business channels in countries that do not require individual product registration and they are in the process of being evaluated to enable them to participate in higher volume tender business.

The group have explored a number of routes in the last year on how best to take their partnership with IDS forward. Whilst IDS previously expressed an interest in acquiring the allergy business, it was decided that the better course of action would be an enlarged distribution model. The board believed they have now agreed the main outline terms which should enable the formal contract negotiations to proceed so hopefully something will be decided soon.

At the current share price the shares are trading on a PE ratio of 35 but this falls to 16.9 on next year’s consensus forecast.

Today the group has announced the placing of up to 13,116,881 new shares at 18p per share and a subscription of up to 1,166,666 to raise up to £2.6M alongside an open offer to raise about £1M. The issue price represents a discount of about 6.5% to the previous share price.

In 2013 the group raised funds for the development and commercialisation of Visitect CD4. Since then, the development phase encountered some technical challenges which are now thought to be resolved. These issues extended the cost and timeframe of commercialisation which it is hoped will occur by late calendar year 2017.

This time, the placing will go towards increasing FoodPrint traction in the US, developing product enhancements that meet the US lab environment and investing into more automated manufacturing capacity; increasing the number of allergens in the Allersys range from 41 to 100; fund certain identified investment opportunities for Allergodip which involve adding new panels and developing a mobile app; and accelerate the pipeline for launching a range of rapid diagnostic tests to two or three per year to include Syphilis, Dengue, S.Typhi, Leptospirosis and Brucella.

Richard Sneller and Legal and General, two large shareholders, are both taking part as are most of the directors and it is nice to see an open offer being included so that us normals can take part too. Assuming full take up of the open offer, the enlarged share capital is expected to be 128,752,672 which will mean the new shares represent about 15.5% of the enlarged share capital.

Going forward, trading in Q1 of the current year is in line with management expectations. The Allersys reagents are now CE-market with the menu continuing to grow, VISITECT CD4 has achieved design freeze, the manufacturing facility in India is now fully validated, and VISITECT Malaria has been CE-marked.

Food intolerance continues to keep up its good performance and the board expect to see this continuing in the year ahead with the strategic marketing initiatives being planned as part of the accelerated growth strategy. With renewed effort regarding the ongoing relationship with IDS, they are looking forward to the eventual launch of the initial range of Allersys tests and hope to deliver VISITECT CD4 to the market by the end of the calendar year.

On the 6th July the group announced that it has concluded the sale and leaseback of a building in Germany. They will receive gross proceeds of €800K and have entered into a contract with the landlord to lease the facility back over 15 years. I am not really a big fan of these kinds of arrangements as it seems to prioritise short term gains over long-term stability in my view.

Overall then this has been another year of fairly slow, steady progress. Profits were up due to tax rebates, otherwise they were broadly flat. Net assets did improve, however, as did the operating cash flow but the group remains unable to generate any free cash. The Food intolerance division remains the only one that makes a profit and that business seems to be very strong but in order to make any progress it seems clear that the allergy business needs to thrash out a deal with IDS and the infectious disease business needs to get the VISITECT CD4 to market. The forward PE of 16.9 suggests some of this is going to happen and if so, the group does seem in a good position. It is a bit disappointing that they need to return to the market to raise more equity but I still have faith and remain a holder.

On the 23rd October the group released a trading update covering the first half of the year. Turnover is expected to be £7.1M, in line with last year in constant currency terms and 4% ahead on an actual basis. Pre-tax profit is in line with expectations.

Food Intolerance saw a 4% increase in revenues at £4.1M. They continue to see strong growth in North America with their microarray-based Food Print test. They are focusing resources more closely into this market. They were able to complete the actions required by LRQA on the self-test version of Food Detective within the agreed time scale and they are awaiting their final review outcome.

Allergy/Autoimmune saw an 11% reduction in revenues to £1.7M. Apparently a significant amount of above average rainfall in July was a contributing factor (there is no indication of why that should have had an effect) and they are expecting a better performance in the second half of the year. The reduction in euro-denominated revenue was mitigated by the weakening of Sterling, however.

In Infectious disease, revenues increased by 1% to £7.1M. The business has started to benefit from the initial sales of the VISITECT range of Malaria tests manufactured in India.

The group has raised £3.3M from a placing and €800K from the sale and leaseback of their German factory. These funds were raise to enable them to accelerate growth. They have signed a supply agreement with a new partner in the US for Food Print which brings the number of partners in the country up to three.

For Allersys, they remain on plan to increase the number of CE-marked allergens that have been developed for use on the instrument to 50-60 allergens by the end of the year. They have had two positive meetings recently with IDS and, subject to finalising a global distribution agreement, they are now confident that they can commercialise their range of products within the current year on terms which are beneficial to both parties.

They have manufactured bulk components for three validation batches of Visitect CD4 which have passed QC testing at external sites and have now been assembled into devices. The first two batches of assembled devices have passed final QC testing. A third batch will begin external testing soon. They have started using these validation batches to verify performance and this programme of testing is about 50% complete. External performance evaluations are underway at two UK hospitals which is expected to be completed within the next few weeks. The external performance evaluation in India is now complete and the data is being fully analysed with performance as expected on an initial review of the data. They therefore remain confident in their ability to CE-mark the test before the end of the year.

Trading in the first half of the year was in line with last year but the board expect a stronger second half. The outturn for the year, however, remains dependent on one of more of the above products delivering a material contribution to results, which sounds a bit shaky to me. Nevertheless the small investment here is remaining.

On the 29th November the group announced that it has CE-market its VISITECT Cd4 test for helping to manage people living with HIV, following successful performance evaluations in India and the UK. This means that the tests are available for general sale through business to business channels in countries not requiring individual product registration. The technical file forms the basis of the additional regulatory approval the company will seek through the WHO prequalification programme. A successful completion of this process will enable the group to become eligible for public sector procurement. The group expects this process will be completed during Q2 of next year.

In addition, they are looking to expand their VISITECT product portfolio and are working on an additional version of the test which utilises a 200 cells/mm3 cut-off. Recent global health guidelines confirm an opportunity also exists for a test that can indicate advanced HIV disease and the group is working to ensure it has a product portfolio encompassing both existing and new opportunities.

The early opportunities are likely to lead to modest sales during the next twelve months but the board anticipate generating significant demand once they have completed all the regulatory hurdles.