Wynnstay has now released their interim results for the year ending 2017.

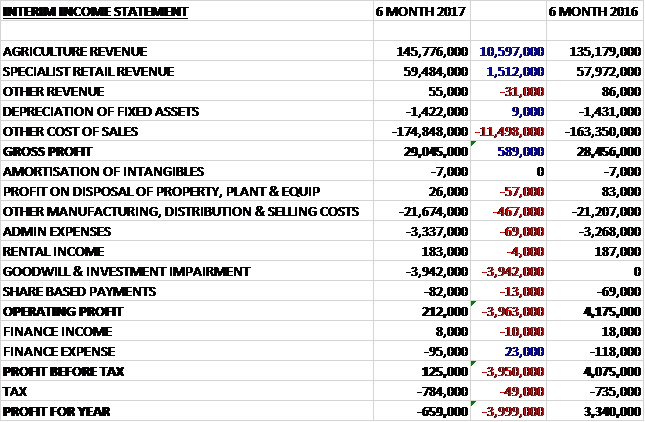

Revenues increased when compared to the first half of last year with a £10.6M growth in agriculture revenue and a £1.5M increase in specialist retail revenue. Cost of sales also increased, which meant that the gross profit grew by £589K. Manufacturing, distribution and selling costs grew by £524K and admin expenses were up £69K. During the period there was also a £3.9M goodwill impairment which meant that the operating profit was down £4M. Finance expenses saw a modest decline but this was more than offset by a £49K growth in tax charges to give a loss for the period of £659K, a detrimental movement of £4M year on year. Excluding the goodwill impairment, this would have been a profit of £3.3M, a decrease of just £57K year on year.

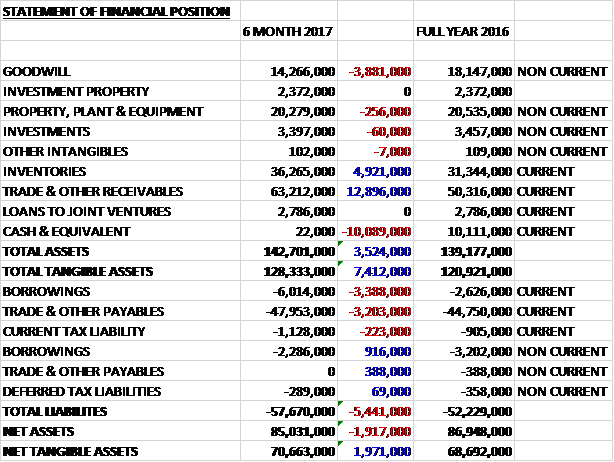

When compared to the end point of last year, total assets increased by £3.5M driven by a £12.9M growth in receivables and a £4.9M increase in inventories, partially offset by a £10.1M fall in cash and a £3.9M decrease in goodwill. Total liabilities also increased during the period due to a £2.5M growth in borrowings and a £2.8M increase in payables. The end result was a net tangible asset level of £70.7M, a growth of £2M over the past six months.

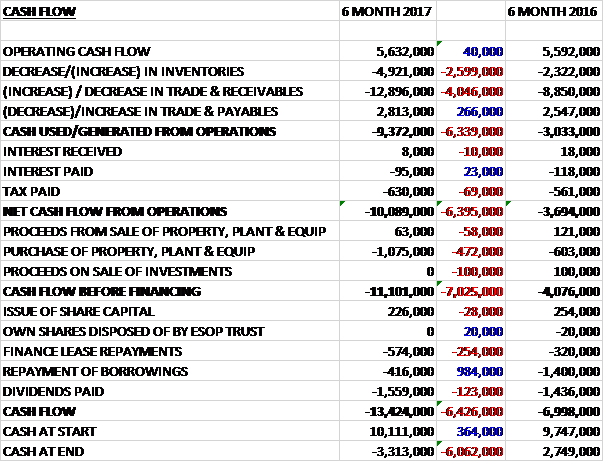

Before movements in working capital, cash profits were broadly flat, increasing by just £40K. There was a cash outflow from working capital which was greater than last time and after tax payments increased by £69K the next cash outflow from operations was £10.1M, an increase of £6.4M year on year. The group spent £1.1M on property, plant and equipment which meant that before financing there was an outflow of £11.1M. The group also spent £574K on finance lease payments, £416K on loan repayments and £1.6M on dividends which meant that there was a cash outflow of £13.4M during the half year and a cash level of -£3.3M at the period-end.

The profit in the Agriculture business was £1.5M, a decline of £280K year on year with low volumes of traded grain and margin pressures in other products affecting the result. The last two years have been particularly challenging for livestock and arable farmers. There has been some improvement in grain and milk prices since last autumn but they have not recovered to levels previously seen. The improvement in output prices has lifted farmer confidence, however, and helped to generate greater demand for most inputs with the group benefiting from the increased volume of feed and arable products but pressure on margins continued.

Strong demand for feed products over the winter months led to an overall increase in feed volume in the period, reflecting the national trend. The early 2017 spring tempered feed demand and in April, total volumes reduced reflecting the decrease in sheep feed. This contrasted with April volumes last year which benefited from inclement weather conditions. The improved milk price supports ongoing demand for dairy feed as producers return to more traditional feeding patterns. As expected the bagging facility commissioned ahead of the winter period helped to improve supply chain efficiencies of bagged product to farm and through the network of retail stores.

Glasson grain performed well in the period. Fertilizer volumes increased significantly but margins remained under pressure. Sales of traded materials and specialist products were slightly lower than the previous year but the business remains well placed in the market.

The smaller grain harvest from last year limited the volume of cereals marketed through the Grain Link and Woodheads businesses and, as a result, the contribution from these activities was below last year’s level. Arable crops have benefited from recent rainfalls which should support prospects for a good 2017 harvest but it is still too early to make firm predictions. Demand for fertilizer was strong over the winter period as farmers ordered ahead of anticipated price increases. Aided by an early spring, overall group volumes exceeded the previous year.

Sales of cereal seed were also buoyant although slightly lower in volume than the record performance last year. There is ongoing demand for herbage seed and agrochemicals as they enter the busy spring growing season.

The profit in the Specialist Retail business was £2.7M, a growth of £270K when compared to the first half of last year, reflecting improved results at Wynnstay Stores. At Wynnstay Stores, like for like sales improved by over 2%. There was a strong performance from key agricultural products, reflecting improved farmer sentiment. This was particularly evident in increased demand for milk powders, animal health and hardware products. They completed the refurbishment of their store at Craven Arms, Shropshire, in the period and will be relocating their store in Denbighshire during the summer.

As previously reported, certain stores at Just for Pets did not deliver the expected performance and, overall, trading remained subdued. This resulted in a loss from the chain during the first half. The board is reviewing the options for the business and it is implementing restructuring measured in the second half. During the year the group made a goodwill impairment of £3.9M relating to Just for Pets.

Going forward, it is encouraging to see an improvement in output prices for farmers but the current oversupply of many commodities in the global market and the negotiations for Brexit will being further challenges for many farmers. This provides for a challenging backdrop for the agricultural supply industry and will affect the rate of recovery of the sector.

At the current share price the shares are trading on a PE ratio of 17.8 which falls to 16.7 on the full year consensus forecast. After an increase in the interim dividend the shares are yielding 2.3% which increases to 2.4% on the full year forecast. Net debt at the period-end was £8.3M compared to £3.9M at this point of last year, reflecting higher levels of working capital utilisation, partly as a result of commodity price inflation.

Overall then this was a bit of a mixed period for the group. Excluding the goodwill impairment, profits declined modestly but net tangible assets improved. The operating cash outflow worsened due to working capital movements – the cash profit performance was broadly flat. The Agriculture business saw profits declined as a lower grain harvest affected traded grain volumes and margin pressures affected other products. An improved farmer sentiment saw Wynnstay stores have a good period but this masked problems at Just for Pets which recorded a loss in the period.

The forward PE of 16.7 and yield of 2.4% mean the shares are not exactly cheap and despite an improved farmer sentiment and better harvest this year, I am not sure this fully takes into account the issues at Just for Pets and other macroeconomic risks.

On the 14th September the group announced that they are appointing administrators to the Just for Pets business which generated an operating loss of £250K in the first half of the year. Management expects to recognise exceptional charges relating to the write-off of net assets of £2.2M and associated costs. This is a real shame that they could not make it work as the stores offered an interesting diversion from the core business.

On the 10th October the group announced that terms had been agreed by the administrators for the sale of 18 stores to PSR Trading. The remaining seven stores are expected to be closed.