President Energy has now released their final results for the year ended 2016.

Revenues declined when compared to last year, reflecting lower oil prices, as a $599K growth in Argentina revenue was more than offset by a $791K decrease in US revenue. Depreciation was down $405K but Argentine workover costs increased by $1.6M and well operating costs grew by $1.1M to give a gross loss $2.5M above last year. Staff costs declined by $971K, however, share based payments were down $934K and there were no legal costs, which accounted for $600K last time. Other admin expenses were up $692K though to give an “underling” operating loss $657K worse than last time. The group received $585K in insurance claim proceeds, however, and impairment charges fell by $355K to give an operating loss $131K lower than 2015, We then see a $1.7M detrimental movement in forex translation and a $569K increase in loan interest, partially offset by a $419K decline in loan fees before a $6.3M increase in the income tax credit meant that the loss for the year was $14M, an improvement of $4.5M year on year.

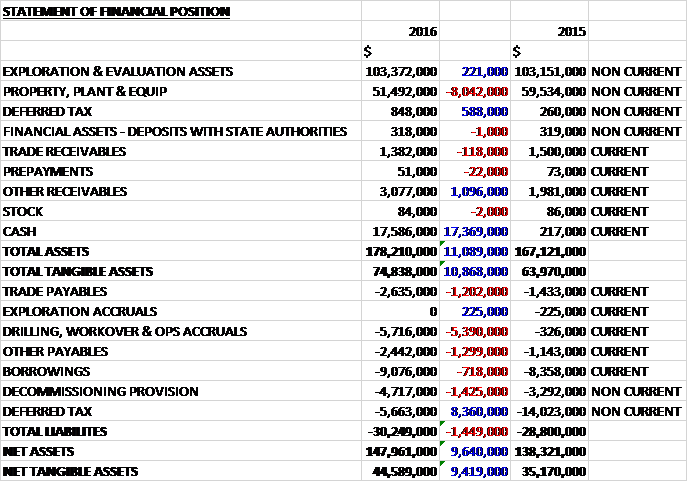

When compared to the end point of last year, total assets increased by $11.1M, driven by a $17.4M increase in cash and a $1.1M growth in other receivables partially offset by an $8M decline in the value of property, plant and equipment. Total liabilities also grew during the year as an $8.4M decline in deferred tax liabilities was more than offset by a $5.4M growth in drilling, workover and operating accruals, a $1.4M increase in the decommissioning provision, a $1.3M growth in other payables and a $1.2M increase in trade payables. The end result was a net tangible asset level of $44.6M, a growth of $9.4M year on year.

Before movements in working capital, the cash outflow increased by $2.1M to $4.6M. There was a cash inflow from working capital, however, as the group seems to have delayed its payments (including some of the costs on the failed DP-1002 well) so the net cash from operations was $2.2M, an improvement of $3.2M year on year. They then spent $578K on exploration and $14M on development and production so that after the $585K of insurance proceeds relating to claims arising in connection with the DP1002 well in Argentina are included, there was a cash outflow of $11.6M before financing. The group then took a net $12.7M of new loans, lost $12M on loans converted to equity and received $31M from the issue of new shares. They also had an interest bill of $2.3M, more than the amount of cash received in operations, to give a cash flow of $17.8M and a cash level of $17.6M at the year-end.

Overall group production increased by 3% to 506boepd but has since increased by 117%, hitting 1,100boepd in April 2017. They are targeting 1,200bopd from Argentina alone by the end of September. The average oil price in the year was $53.51 per barrel compared to $56.48 in 2015. Oil sales in Argentina averaged $57.83 per bbl as the regulated price moved in line with prevailing global oil prices. Well operating costs before workover expenses were managed down from $63.02 to $55.69 so at this oil price, the group is not making money. There has been a continued focus in 2017 on efficiency gains in field operating costs so the group are expecting a further reduction this year.

Production at Puesto Guardian increased by 26.3mboe to 125.1mboe; production at East Lake Verret declined by 4.1mboe to 18.3mboe; and production at East White Lake declined by 15.9mboe to 41.6mboe.

The operating loss in Argentina was $4M, an increase of $1.9M year on year with average production increasing by 26% to 342bopd. The first part of the year was spent conducting workovers of certain wells in the Puesto Guardian concession with solid progress in production rates, albeit not spectacular. The decision was taken in the second part of the year to drill new horizontal wells, the first being the DP-1002 well at Dos Puntitas.

The DP-1002 well drilled to the reservoir ready for the production leg but suffered throughout from various mechanical and service quality issues. The well was rendered incapable of completion for production and costs impaired giving rise to an impairment charge of $10.9M. The group are pursuing claims against certain service providers in connection with that well.

After the year-end, the group worked over the DP-1001 well in Argentina which initially returned to production at about 300bopd from a vertical section. Additionally ongoing studies at the concession have yielded encouraging results indicative of the potential for structures and reservoir targets on the concession that have not to date been targeted. This reinforces management’s view that there exist multiple development and appraisal opportunities as well as workover opportunities that could yield material upside, particularly should oil prices recover from their present levels.

The operating loss in Paraguay was $132K, a decline of $329K when compared to last year. Geological work continued through the year and is ongoing. With the modest improvement in oil prices, the results of their technical work combined with appetite returning for exploration projects, the group has determined that it is now appropriate to move forward to identify farm out partners for their interests in the country.

The operating profit in the US was $188K, a decrease of $783K when compared to 2015. Production fell by 25% to 164boepd due to gas pipeline outages at the Triche well and natural decline at East Lake Verret and East White Lake. The realised prices in the country edged up 3% to $44.51/boe with cost of sales growing to $37.48/boe due to the lower production. During the second half of 2016 steps were taken to manage down further operational and admin costs in the US operations, the benefits of which should be seen in 2017.

In April 2017 the group acquired an additional 50% working interest and the assumption of operatorship of the Triche Well in East Lake Verret, for an initial cash consideration of $2.25M and an additional production related earn out of up to $400K. They already held a 12% interest and the acquisition represents an incremental production stream of about 150boepd. The well is performing in line with expectations since the acquisition.

The group’s interest in Australia had already been completely written off and was relinquished without penalty. During the year a placing raised $20M and a conversion of $12M of debt to equity was undertaken.

So far, turnover in the first five months of 2017 is ahead of the same period of 2016. The group did not make a profit last year and is not expected to make one in the coming year either so PE comparisons are meaningless. At the year-end the group had a net cash position of $17.6M compared to net debt of $8.1M at the end of last year.

On the 5th July the group released an Argentina sales update. June proved to be a record month for oil sales from Puesto Guardian, generating revenue of $1.2M in the month. In addition, the group continues to benefit from the newly expanded Louisiana production assets which in a usual month contribute over $200K of free cash. With the Argentine production currently insulated against the day to day volatility of the oil price, the group continue to concentrate on margins and profitability.

On the 17th July the group released an update covering the Puesto Guardian workover programme. Since the last update, they have completed work on the new water disposal well at Dos Puntitas 8 and brought the prior successful workovers at Puesto Guardian 21 and Dos Puntitas 15 into production as planned and at expected levels. The rig then moved to well CGr-20 at the Canada Grande field in the concession.

Canada Grande had not seen any consistent production activity since 2011. The well has on a two day test steadily free flowed good quality light oil at rates in the range of 50-80bopd without the need for the previously planned stimulation or downhole pump. Accordingly, steps are now being taken to hook up this well to the Puesto Guardian field battery as the Canada Grande field is in a remote location having had its infrastructure removed some time ago.

The successful test results and steady oil flow has encouraged the group to consider other old wells in the Canada Grande field as well as undrilled prospectivity there. In the meantime, the rig is now moving back to the Puesto Guardian field for the next workover at well PG-19. In parallel, facility upgrades continue to take place with the emphasis on replacing old equipment, maintaining production with the minimum of shut downs and bringing in more powerful surface pumps to more adequately handle the increased gross fluids being produced.

Overall then last year has been another difficult one for the group. The loss improved but this was due to tax receipts and pre-tax losses widened. Net assets increased, as would be expected with the equity raise, and although the operating cash flow improved, this was due to a large increase in payables and cash losses worsened. The Louisiana business is, just about, still profitable at these oil prices but Argentina is yet to break even. An overall sale price of $53.51 and cost price of $55.69 tells the story.

So far this year, some progress is being made on costs and a great deal of progress has been made on Argentinian production. Whether this is enough to actually make any money, given Brent crude is currently below $50 per barrel is doubtful. Following the placing, the group is in a much better position, with a decent amount of cash but I just don’t see any money being made with the oil price still so low.

On the 2nd August the group released a production update. The group have now completed the workover of well PG-19 at Puesto Guardian which has been shut in for the last 19 years. After a downhole jet pump is installed, work will start to hook the well up to the battery. Taking into account the well history and up to date pressure data, an initial conservative gross fluid rate of 500-bopd at a 750 barrels per day would deliver 50-% oil cut. The workover rig will then move to well PG-20 which has been shut in since 2002.

Argentinian production is currently limited by the significant ongoing infrastructure works at the concession including installing five new surface pumps, lifting and cleaning of existing downhole pumps, laying of production lines prior to hooking up new producing wells and the commissioning of two new water disposal wells to handle increased water generation arising from the new production wells. All these works are expected to be completed during September.

With the workover programme still continuing, whilst production is presently constrained to a maximum of about 600 bopd, the group intends to bring on stream an additional four producing wells during September with a further three wells, which are currently working at sub-optimal capacity, brought up to full volume within that same time period and a three well stimulation campaign also slated for that month.

In the US, after a prolonged period of shut in due to heavy rain, production has now come back up to pre-shut in levels of 300boepd net to the group, with the new Triche well acquisition contributing comfortably in line with expectations.