Amino Technology has now released their interim results for the year ending 2017.

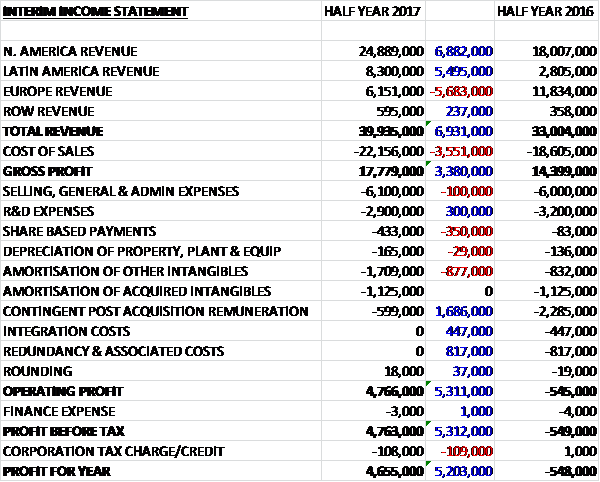

Revenues increased when compared to the first half of last year as a £5.7M decline in European revenue was more than offset by a £6.9M growth in North American revenue and a £5.5M increase in Latin American revenue. Cost of sales increased by £3.6M to give a gross profit £3.4M higher than last time. Admin costs were broadly flat, R&D expenses fell by £300K but share based payments increased by £350K and the amortisation of other intangibles grew by £877K. A few one-off costs declined, however, with contingent post acquisition remuneration down £1.7M, integration costs falling by £447K and redundancy costs decreasing by £817K to give an operating profit £5.3M higher. Tax charges were up £109K and the profit for the half year came in at £4.7M, a positive movement of £5.2M year on year.

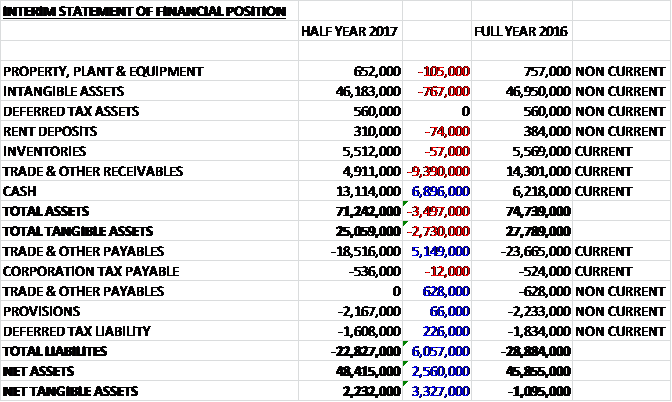

When compared to the end point of last year, total assets declined by £3.5M driven by a £9.4M decrease in receivables and a £767K decline in intangible assets, partially offset by a £6.9M increase in cash. Total liabilities also declined during the year due to a £5.7M fall in payables. The end result was a net tangible asset level of £2.2M, a positive movement of £3.3M over the past six months.

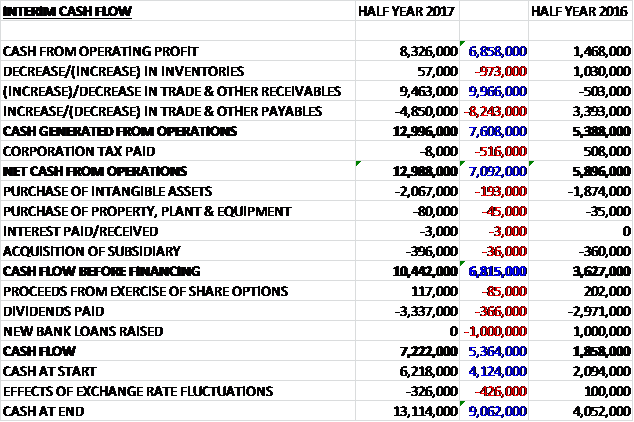

Before movements in working capital, cash profits increased by £6.9M to £8.3M. There was a cash inflow from working capital but tax payments increased by £516K to give a net cash from operations of £13M, a growth of £7.1M year on year. The group spent £2.1Mon intangible assets and £396K on acquisitions which meant that the free cash was £10.4M. Of this, £3.3M was spent on dividends to give a cash flow of £7.2M for the half year and a cash level of £13.1M at the period-end.

At constant currency there was underlying revenue growth of 4%. Sales of IP devices were strong, particularly in North and Latin America, which reported overall revenue growth of 38% and 196% respectively. In North America, sales through distribution partners showed good momentum and a major customer also placed follow-on orders for devices after the deployment of their Enable virtual set top box software platform. In addition there are an increasing number of opportunities arising from the migration of old style cable TV networks to IP-based service delivery, often over new fibre infrastructure. After the period-end they secured orders from a new customer, US regional operator Muscatine Power and Water, as a direct result of this migration.

The Latin American market saw regulatory change which is presenting new opportunities for the group to build on its existing foothold. Revenue growth for the period was driven by a mix of new customer wins and continued demand from established operators for IP devices and the Enable software platform.

European sales were 48% lower, principally due to the change of ownership of a key customer impacting the timing of orders which the board now expect to recover over the medium term. During the period they progressed well with the implementation of their first full end to end multiscreen entertainment service to Delta, however. This comprises both the Move cloud TV platform delivering TV to mobile devices, as well as TV services delivered to the home via a 4K UHD compatible Amino IPTV device. Beyond this, they see new opportunities in an increasingly disrupted global market where traditional operator business models face continued pressure from OTT subscription video on demand providers such as Amazon and Netflix.

The group’s customer offering has broadened in line with the industry-wide shift to IP and cloud based TV service delivery. Their portfolio has been enhanced during the period by the addition of a new compact 4K UHD Android TV device to meet the needs of the growing number of operators who are planning to deploy Android to support their TV offering.

They have also positioned their Enable software platform as a virtual set top box to provide operators with a cost effective means of delivering new and unified TV experiences across legacy devices already installed in customer homes. During the period the Chilean operator GTD deployed this solution across its customer base. The pipeline of qualified software opportunities arising from planned upgrades to legacy devices in 2018 is significant.

Software and Services revenues declined by 41% to £3M. Last time they included £2M of one-off revenue from Enable software contracts that did not repeat. Excluding these, recurring software and service revenues grew by 30%. Devices revenue increased by 11% to £36.9M. Gross margins are expected to be lower in the second half as a result of the shift in product mix towards newer product lines and industry wide pricing pressures for certain components.

Exceptional items this time included £600K contingent post-acquisition remuneration in respect of the Entone acquisition. The final retention plan payment is due in August and is expected to result in a maximum cash payment of £1.2M.

Going forward, the sales pipeline is robust and the board are confident that they will deliver gull year profits in line with market expectations.

At the current share price the shares are trading on a PE ratio of 14.1 which falls to 13.8 on the full year consensus forecast. At the period-end the group had a net cash position of £13.1M, aided by the timing of some large orders, compared to £3.1M at the same period of last year. After a 10% increase in the interim dividend the shares are yielding 3.3% which increases to 3.5% on the full year forecast.

On the 18th July the group announced that non-executive director Michael Bennett sold 1M shares at a value of £1.9M. This is quite a hefty sale.

Overall then this has been a pretty decent period for the group with profits up, net assets increasing and the operating cash flow growing with plenty of free cash being generated. The cash flow was aided by the timing of that large order and forex has also been a strong tailwind for the group but the underlying performance seems to have improved modestly. Things seem to be going very well in the Americas but the European division struggled due to a major customer being taken over. The board seem to think this will recover, however.

The forward PE of 13.8 and yield of 3.5% are probably about right. I am tempted to buy in here but am a little put off by the large director sale. It may be more prudent to wait and see, a tricky one!

On the 9th August the group announced that non-executive director Michael Bennett sold 1,000,000 shares at a value of £1.9M. This is another large sale.

On the 15th August the group announced that CEO Donald McGarva purchased 2,780 shares at a value of nearly £5K. This is a drop in the ocean as he holds 445,428 shares.

On the 30th August the group announced that Michael Bennett continued to sell off his holding with a disposal of 600,000 shares at a value of £1.1M.

On the 5th September the group announced that non-executive director Michael Bennett sold 50,000 shares at a value of £98K.

On the 5th December the group released a trading update covering the full year. They expect to report a full year performance that demonstrates customer traction for their IP/Cloud video software solutions despite industry-wide memory cost headwinds. Gross profit and pre-tax profit are expected to be in line with expectations whilst revenue is expected to be similar to the previous year. They enter 2018 with a solid backlog and excellent pipeline which provides the board with confidence for the year ahead.

On the 6th June the group released a trading update covering the first half of the year. During the period they booked over 40% more orders than in the first half of last year. This, along with good pipeline coverage, means that the board’s expectations remain unchanged.

They expect to have revenues weighted to the second half of the year and so, expect year on year revenues to be down £9.9M. Earlier this week they announced that Kabelnoord, the leading Dutch cable operator, is to deploy the group’s MOVE end to end multiscreen video platform in H2.

Revenues from software and services sold on a standalone basis continued to increase to around $5M. Net cash at the period-end was £11.3M, a decline of £1.8M.