RM has now released their interim results for the year ending 2017.

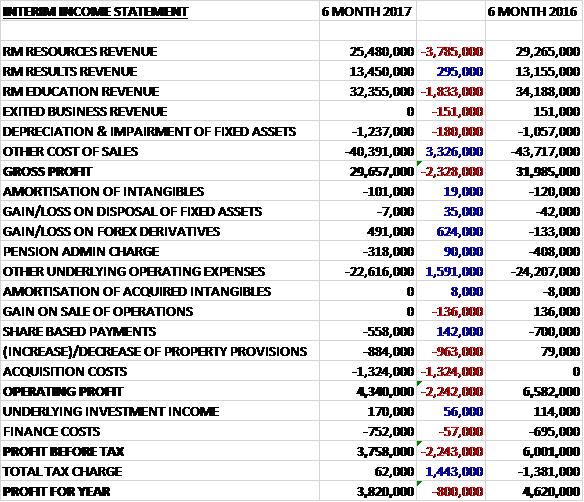

Revenues declined when compared to the first half of last year as a £295K growth in RM Results revenue was more than offset by a £3.8M decline in RM Resources revenue and a £1.8M decrease in RM Education revenue. Cost of sales also fell to give a gross profit £2.3M lower than last time. There was a £624K positive swing to derivative forex gains and other underlying operating expenses declined by £1.6M but there was a £963K increase in property provisions and £1.3M of acquisition costs to give an operating profit £2.2M lower. Finance costs were broadly stable and the tax charge declined by £1.4M to give a modest tax credit, reflecting the one-time benefit of £978K due to a reduction in the transfer pricing tax provision associated with cross border intra-group transactions between the UK and India, and a profit of £3.8M, a decline of £800K year on year.

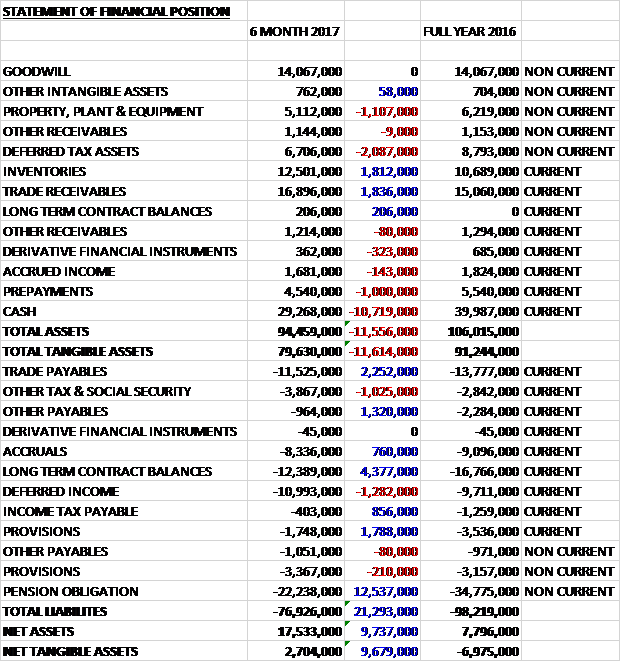

When compared to the end point of last year, total assets declined by £11.6M driven by a £10.7M decrease in cash, a £2.1M fall in deferred tax assets, a £1.1M decline in property, plant and equipment and a £1M fall in prepayments, partially offset by a £1.8M growth in inventories and a £1.8M increase in trade receivables. Total liabilities also declined during the period due to a £12.5M fall in the pension liability reflecting positive asset performance, a £4.4M decrease in long term contract payables and a £2.3M fall in trade payables. The end result was a net tangible asset level of £2.7M, a positive movement of £9.7M year on year.

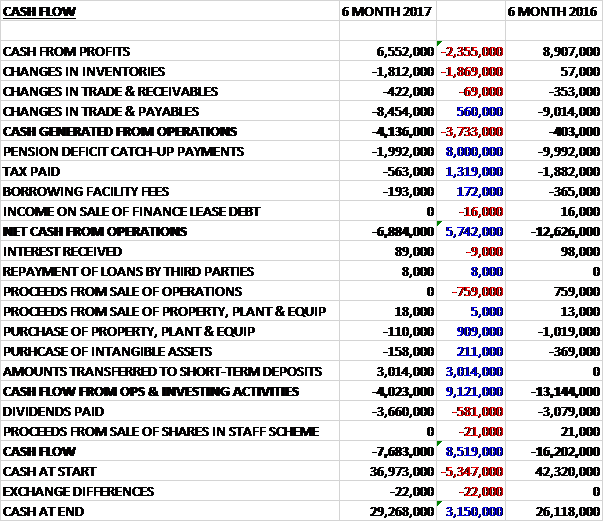

Before movements in working capital, cash profits declined by £2.4M to £6.6M. There was a cash outflow from working capital but tax payments reduced by £1.3M and pension catch-up payments declined by £8M which gave a net cash outflow of £6.9M from operations, an improvement of £5.7M year on year. The group had very little in the way of capex with £158K going on intangibles and £110K on tangibles but they spent more on dividends, with £3.7M being distributed to shareholders. This meant that there was a cash outflow of £7.7M in the half year and a cash level of £29.3M at the period-end.

The profit in the RM Resources division was £2.8M, a decline of £1.4M year on year. UK direct marketing revenues decreased by 20% with schools continuing to focus on buying essentials as a result of ongoing tightened UK budgets for schools. International revenues grew by 29% driven by increased sales of proprietary products but operating margins reduced from 14.6% to 11%, impacted by the lower UK revenues and adverse forex movements which more than offset a £1.1M reduction in operating costs.

The profit in the RM Results division was £2.8M, a growth of £387K when compared to the first half of last year. Revenues increased by 2.2% benefiting from a new five year framework agreement signed with Oxford University Press to deliver a global assessment platform, and the timing of revenues accounted for in the first half that more than offset lower data contract revenues. Operating margins increased from 18% to 20.5%.

The profit in the RM Education division was £3.1M, an increase of £834K when compared to the first half of 2016. Revenues reduced by 5.4% reflecting the continued transition away from legacy offerings. These included reduced Building Schools for the Future infrastructure spend and lower warranty and network revenues. In the period they were selected by Education Scotland to continue to deliver their largest Digital platform contract providing Glow authentication and portal services over five years. They are also awarded a three year contract for connectivity services for over 500 schools in Hertfordshire. Despite the reduction in revenue, the division significantly improved operating margins, up from 6.6% to 9.6% reflecting the benefits of the cost cutting taken last year.

After the period-end the group acquired Hedgelane from Smiths News. In connection with the acquisition they have entered into a £75M revolving credit facility. The focus now is on combining this business within RM Resources to create scale and to deliver meaningful synergies.

Going forward, whilst market conditions in the UK education sector continue to be challenging as a result of pressure on school budgets, the board’s expectations for the full year results remain unchanged.

At the current share price the shares are trading on a PE ratio of 10.8 which falls to 9 on the full year consensus forecast. After a 10% increase in the interim dividend the shares ae yielding 3.6% which grows to 3.9% on the full year forecast.

Overall then this has been a bit of a mixed period. Profits were down due to higher provisions and acquisition costs, underlying profits were broadly flat. Net assets improved as the pension deficit fell and although the operating cash outflow did improve, this was due to lower pension payments and cash profits declined. RM Resources struggled as a result of depressed schools budgets and higher costs due to forex movements but both Education and Results saw profits rise due to cost cutting and order timings respectively.

The acquisition is obviously going to change a lot here, including taking on quite a bit of debt to the already struggling balance sheet. Until more is known about how this is going to leave the balance sheet, I feel unable to invest here despite the forward PE of 9 and yield of 3.9% suggesting value is on offer here.

On the 7th December the group released a trading update covering the year as a whole where they stated trading will be ahead of expectations. RM Resources benefited from organic revenue growth in H2 and RM Education experienced a resilient performance following last year’s restructuring. RM Results was in line with management expectations, having had a strong summer delivery.

Net debt at the year-end was £13.4M following the acquisition of The Consortium in June. Good progress is being made on integration and better synergies coupled with more scope for operational efficiencies are now expected to realise benefits ahead of the initial expectations of £2M per annum. Agreement has also been reached with the Trustees of the Consortium Care defined benefit pension scheme with regards to the triennial valuation as at the end of December at a deficit of £4.2M, with a recovery plan of £379K per annum over the next ten years, which doesn’t seem too onerous.

This all sounds very positive and I am tempted to make a purchase here.