Pan African Resources has now released their interim results for the year ending 2017.

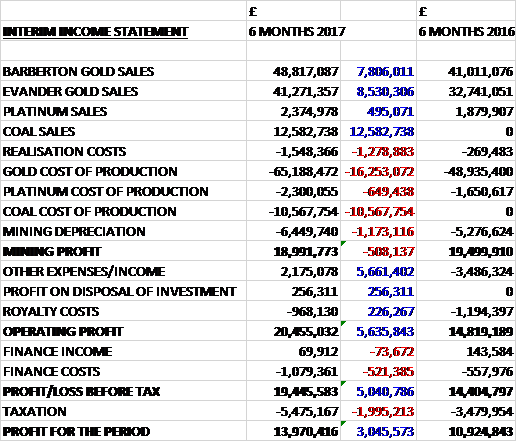

Revenues increased when compared to the first half of last year with a £7.8M growth in Barberton Gold sales, an £8.5M increase in Evander Gold sales, a £495K growth in in platinum sales and the first £12.6M of coal sales. Realisation costs increased by £1.3M, the gold cost of production grew by £16.3M with both labour and electricity costs increasing considerably, the platinum cost of production increased by £649K, there was a £10.6M cost of coal production and mining depreciation rose by £1.2M to give a mining profit £508K lower than last time. There was a £5.7M positive shift to “other income”, possibly due to a gold hedge, a small profit on the disposal of an investment and a £226K decrease in royalty costs which meant that the operating profit grew by £5.6M. Finance costs rose by £521K and tax charges grew by £2M due to increased deferred taxes so the profit for the period was £14M, a growth of £3M year on year.

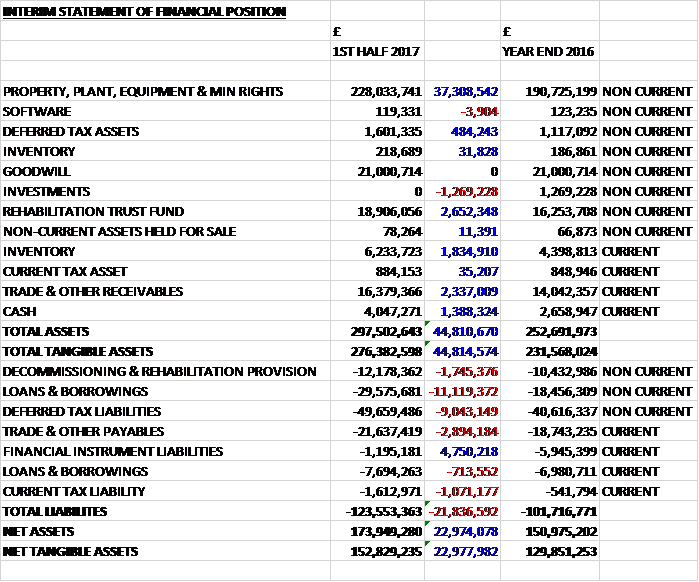

When compared to the end point of last year, total assets increased by £44.8M driven by a £37.3M growth in property, plant and equipment, a £2.7M increase in the rehabilitation trust fund, a £2.4M growth in receivables, a £1.8M increase in inventories and a £1.4M growth in cash , partially offset by a £1.3M decline in the value of investments. Total liabilities also increased during the period as a £4.8M decline in financial instruments was more than offset by an £11.8M increase in borrowings, a £9M growth in deferred tax liabilities, a £2.9M increase in payables and a £1.7M growth in the rehabilitation provision. The end result was a net tangible asset level of £152.8M, a growth of £23M over the past six months.

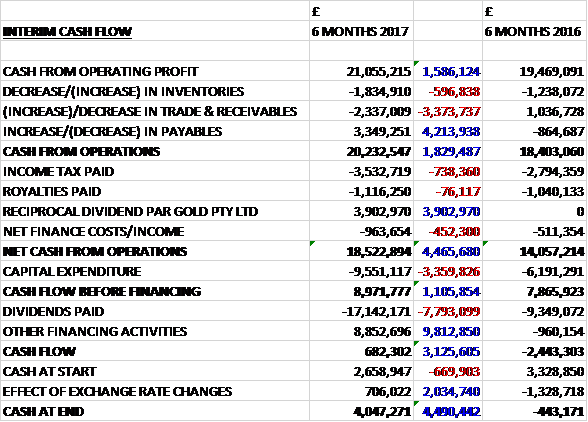

Before movements in working capital, cash profits increased by £1.6M to £21.1M. There was a small cash outflow from working capital, tax payments increased by £738K and finance payments grew by £452K but there was a £3.9M reciprocal dividend from PAR Gold Pty which meant that the net cash from operations was £18.5M, a growth of £4.5M year on year. There was £9.6M of capex which gave a free cash flow of £9M. This did not cover the £17.1M dividend so the group took out £8.9M in new loans to give a cash flow of £682K and a cash level of £4M at the period-end.

The group has benefited from the weakness of sterling. In Sterling terms, profits increased by nearly 25% but in Rand terms the growth was only 10%. Overall group gold production decreased by 10% to 91,613 ounces but the gold price received increased by 13.2% to $1,257 per ounce. Due to the lower gold production, all in sustaining costs increased from $908/oz to $1,014 per ounce.

The net pre-tax income at Barberton was £20.3M, an increase of £7.2M year on year. The average mining head grade reduced from 10.6g/t to 9.4g/t as the Fairview mine experienced issues resulting from lower grade face values, specifically at its high grade 11-block. Work is underway to develop additional production platforms to expose additional high grade panels to increase mining grades.

Gold sold decreased by 13% to 49,212 ounces as a result of the underground gold sold decreasing by 9,146 ounces to 49,212 ounces. The BTRP gold sold increased by 1,911 ounces to 14,741 ounces, supported by grades increasing from 1.3g/t to 2.2g/t. Three separate incidences of community unrest interrupted production as these protests prevented employees from reporting to work, resulting in six days of lost production. In addition, six section 54 regulatory notices resulted in eight lost production days.

Despite the fall in gold production, revenues increased modestly in Rand terms due to a higher gold price. Cash costs increased from $610 per ounce to $773 per ounce as a result of the reduction in the amount of gold produced.

The net pre-tax income at Evander was £372K, a decline of £2.3M when compared to the first half of last year. The average mining head grade reduced from 5.8g/t to 5.4g/t. Due to Section 54 stoppages and a reduction in hoisting speed at 7 shaft during the period, the amount of gold sold fell by 6.5% to 42,401 ounces although revenues increased due to the higher gold price. The 7 shaft, which is used to hoist ore from underground mining to the surface is undergoing critical repairs and maintenance and requires a suspension of the underground mining operations for up to 55 days from 20th February.

The mine experienced a material increase in safety stoppages during the period. They were issued with four Section 54 notices which resulted in 13 lost production days, mainly relating to shaft 7. Cash costs increased from $903/ounce to $1,114 per ounce.

The net pre-tax loss at Phoenix Platinum was £276K, a worsening of £262K when compared to the first half of 2016. The tonnes processed increased by 3.9% to 122,024 tonnes. In July 2016 the business commissioned a scrubber which increased the production capacity by 25% but re-mining was limited by a recent drought. The head grade achieved reduced from 3.2g/t to 2.2g/t due to re-mining from the lower grade tailings facility. Overall PGE production increased by 1.8% to 4,574 ounces with recoveries increasing from 39% to 57% following the installation of thigh energy agitation cells in the plant. Revenues increased due to a modest increase in production and a rise in the selling price, up from $641 per ounce to $664 per ounce.

The cost of production increased from $563/Oz to $643/Oz, however, due to the higher cost associated with transporting the Elandskraal tailings to the plant and higher refinery charges relating to the higher chrome prevalence in the tailings processed from Elandskraal.

The maiden net pre-tax income from Uitkomst Colliery was £1.8M. The operation produced and sold 327,202 tonnes of coal, of which 127,605 tonnes was from the underground mining operations with the rest coming from third parties for processing.

The Elikhulu Tailings treatment project which was approved during the period will provide organic production growth of around 56K ounces of gold per annum and reduce the overall cost profile of the operations. The decision to start construction of the project remains subject to finalising the most appropriate financing package but the group hope to commission it by Q4 2018 calendar year. It is expected to have all in sustaining costs of $523 per ounce over the life of the project and the initial capital cost is forecast to be about £103M which equates to a payback period of four years assuming a gold price of $1,180 per ounce.

The Evander 2010 pay channel is a potentially attractive orebody that runs parallel to the Kinross pay channel and is accessible via the 7 shaft. Surface drilling is underway but initial results have been delayed due to poor rock conditions as well as due to the intersection of water on various instances. The first reef intersection is now expected in April 2017. The 2010 pay channel may offer the group the possibility of establishing a new underground mining area without the cost of sinking a new vertical shaft from the surface.

In conjunction with the 7A shaft refurbishment, Evander’s management initiated a number of independent engineering studies to assess the condition of the underground mining infrastructure. These studies identified critical issues requiring remedial action to ensure safe operation of these shafts. The nature of the refurbishments require a suspension of Evander mines underground operation for a period of up to 55 days with the tailings and surface operations unaffected. The cost of the programme is expected to be around £2.3M.

The immediate focus is to restart the Evander underground mining operations following the suspension of mining to refurbish critical infrastructure, and to finalise the Elikhulu funding package.

At the current share price the shares are trading on a PE ratio of 7.4 which falls to 6.8 on the full year consensus forecast. After an increase in the dividend the shares are yielding 7% but this falls back down to 5% on the full year forecast. At the period-end the group had a net debt position of £28.4M compared to £19.4M at the year-end.

On the 10th March the group released an update. The Evander shaft repairs are progressing on schedule and are still expected to be completed on time. During the suspension of the underground mining operations, the treatment plants have used available capacity to continue processing tailings and additional surface sources. The group have also implemented a number of initiatives to reduce the mine’s underground fixed cost base once mining re-starts.

Evander mines has also reached an agreement with the National Union of Mineworkers. Around 30% of their employees will be retrenched at a cost of around $4.1M. These personnel were designated as redundant for Evander to meet production targets.

With regards the Elikhulu financing the group has built a book of demand in excess of the shares it was given authority to issue at the shareholder meeting but given the current market conditions and volatility they have decided not to complete an equity issuance at this time. They will continue to progress the development from cash and banking facilities until the final funding package is secured.

On the 5th April the group announced the disposal of the Uitkomst colliery for a total consideration of £15.7M. The profit on disposal is £3.8M and the consideration consists of £7.1M in cash, £1.4M of deferred consideration and the rest in COAL shares. This enables management to concentrate on Elikhulu and helps with the cash flow but is a bit of a strange turnaround in strategy in only a short time.

On the 8th April the group announced that the refurbishment at Evander is progressing according to schedule with underground mining operations restarting sometime after the 15th April.

On the 12th April the group announced a proposed funding package for Elikhulu. This includes a proposed placing of 291,480,983 new shares at an issue price of 14p per share and a $72M underwritten seven year debt facility agreed in principle with Rand Merchant Bank. The placing is to raise $51M subject to demand.

On the 20th July the group announced an operating update covering the year. Gold produced was approximately 4.4% below the production guidance at 173Koz due to the slower than anticipated restart of the underground mine at Evander and operational challenges experienced at Barberton, which have now been remedied. The production guidance for 2018 is now 190K ounces.

At Evander in the coming year there will be a continuation of the engineering work plan to improve the reliability of the shaft and related infrastructure, an improvement in the total amount blasted per panel and crew, old gold vamping which is the cleaning of mud accumulations in redundant declines and spillage in and around the belt declines, and pillar mining and vamping at 7 shaft.

Mining in the high-grade areas in Fairview’s 11 block is also now established and expected to continue for the remainder of the year. Productivity improvements are expected at Fairview following the commissioning of a new bulk air cooler which will reduce the ambient temperature at the work face by around 3-4 degrees C. To address the flexibility constraints currently experienced at Fairview, and increase gold production, a feasibility study into a new sub-vertical shaft has been finalised.

The Elikhulu project is progressing according to plan. Following the $50M equity raise in April, the group has started funding the initial capex on the civil engineering works and the procurement of the long lead time items such as the tower crane and carbon in leach tanks. Capex of £10M has been incurred on the project during the current period and capital spend remains on track to be within initial forecasts.

The Fairview mining operation at Barberton is currently restricted by the hoisting capacity of its No.3 Decline, which is used to access workings below 42 Level. This decline is currently used to transport employees, material and for rock hoisting. The 11-block, or MRC, orebody has an average grade of 31.3g/t and current life of mine of 22 years. With no intervention, future mining at depth will result in increased travelling distance. The estimated capex for the sub-vertical shaft from 42 level to 64 level, which will be used to transport employees and material to the working areas so that the No.3 decline can be used exclusively for rock hoisting, is £6M to be incurred over two years. These improvements are estimated to yield an additional 7K ounces of gold per annum.

At Evander, an exploration borehole intersected the Kimberley reef at a depth of around 2km, highlighting a reef intersection with a 6cm width 36.8g/t. Additional drilling deflections will be performed to further delineate the ore body. The group has started a feasibility study related to the 7 Shaft No.3 Decline and 2010 Pay Channel resource which can potentially increase the mine’s underground gold production significantly at a relatively low capital cost. The study is expected to be completed in Q1 2018.

At the period-end the group had net debt of £3.8M compared to £19.4M at the end of last year. The group has also announced that they have sold Phoenix Platinum to Sylvania Platinum for a total cash consideration of £5.1M.

Overall then, this has been a bit of a mixed period for the group. On the surface, the financial performance has been decent. Profit was up, seemingly due to “other income”, net assets increased and the operating cash flow improved with some free cash flow being generated. This seems to have been due to an increase in the gold sales price. Operationally things don’t seem to have been that good. Barberton saw a growth in profits due to increases in the sales price. Production fell due to community unrest and stoppages.

The Evander mine saw profits fall and it is barely making any profit at the moment due to several stoppages and an issue with the shaft 7 which led to a suspension in underground mining, which has now been rectified. Phoenix saw profits fall too but this operation has now been sold. Likewise, Uitkomst, which made a decent contribution during the period has also been sold. The Elikhulu tailings project is the focus going forward and this is a big project which has some risk attached. The forward PE of 6.8 and yield of 5% does account for some of this risk but I am not sure the time is right at the moment.

On the 25th August the group announced that the Integrated Water Use licence of Elikhulu has been granted for a period of 20 years. All environmental permits are therefore now in place to start construction.