Zytronic has now released their final results for the year ended 2018.

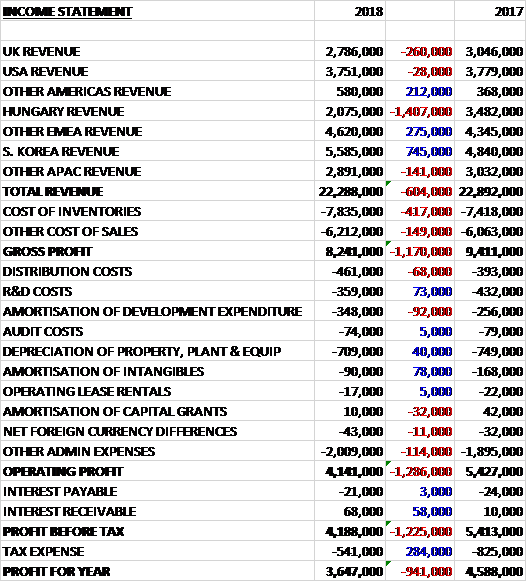

Total revenues declined by £604K when compared to last year as a £745K growth in Korean revenue was more than offset by a £1.4M decline in Hungarian revenue. Cost of inventories were up £417K and other cost of sales grew by £149K to give a gross profit £1.2M higher. Admin expenses also saw a modest rise but there was a £58K growth in interest receivable and a £284K decrease in tax expenses to give a profit for the year of £3.6M, a decline of £941K year on year.

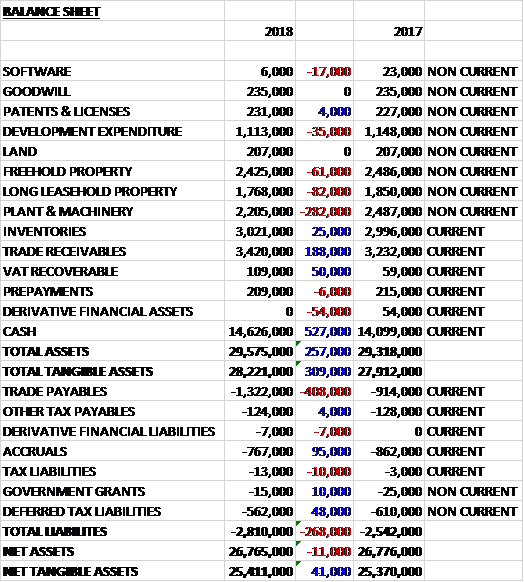

When compared to the end point of last year, total assets increased by £257K driven by a £527K growth in cash and a £188K increase in trade receivables, partially offset by a £282K decrease in plant and machinery. Total liabilities also increased during the year Due to a £408K growth in trade payables. The end result was a net tangible asset level of £25.4M, a growth of just £41K year on year.

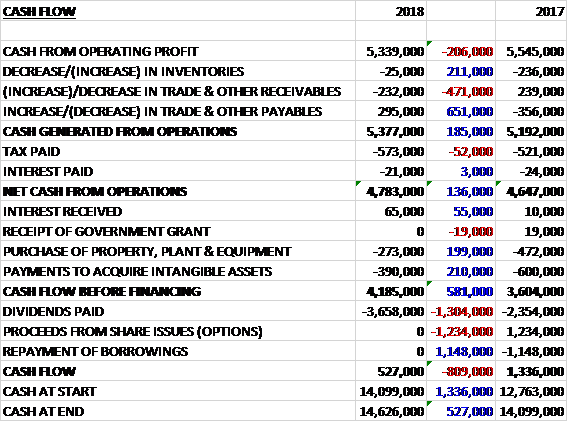

Before movements in working capital, cash profits declined by £206K to £5.3M. There was a slight cash inflow from working capital compared to a cash outflow last time and after tax payments increased by £52K the net cash from operations was £4.8M, a growth of £136K year on year. The group spent £273K on property, plant and equipment along with £390K on intangible assets which meant that the free cash flow was £4.2M. Of this, £3.7M was spent on dividends which meant that the cash flow for the year was £527K and the cash level at the year-end was £14.6M.

This year they continued to experience encouraging growth in sales of their touchscreens to the gaming sector which somewhat offset the decline in sales to financial markets. The benefit of this growth was partly offset by lower margins, however, principally from labour and material inefficiencies as new and different products and methods associated with gaming replaced more familiar touchscreens for the ATM sector.

The first half revenues were affected by the performance of the financial market (ATMs) which at £2.8M was £1.1M lower than the prior year. The second half performance was also impacted by the financial market but to a lesser degree as the improvement in the level of sales did not materialise as quickly as hoped. As a result, the total impact was £1.3M of reduced financial sales for the full year composed of £900K of touch and £400K of non-touch.

Within touch sales, gaming, which was dominated by casino-based upright cabinet designs, has continued to be the top revenue generating application market with growth of £500K. This growth reflects the maturation of existing projects and new predominantly Asian PCT and MPCT projects which moved into production.

Financial touch sales saw a decline on the back of total unit volumes falling by 6,000 to 44,000 units. The board believe that the decline has been down to several factors which have generally been felt by the larger ATM OEMs in the market. These were an imposed change in the procurement practices in China for the Chinese market, a slower than anticipated change to the outsourcing of ATM assembly to third parties, and the move by financial institutions to a Windows 10 operating system and consequent delays caused in them placing new unit orders. There is also little doubt that consumer digital money management may be influencing future ATM deployment levels.

Vending continued to be their second highest market in terms of units produced at 28,000 but this was 7,000 units lower than last year due in the main to two factors, the finalised supply of the Freestyle Coca Cola drinks machine and a reduced supply into German-based customers in the field of parking management and fare collection. In terms of revenue, it remained the third largest market but declined by £500K.

The industrial market saw an 8,000 unit increase in sensors sold to 24,000 units and an increase in revenues generated of £200K. The signage market increased by £400K on the back of a 1,000 unit increase in large sensors sold to 2,000 units as the number of smart city type street furniture deployments increased, particularly for cities in the US which offer on the street internet, wayfinding and WIFI hotspot capabilities.

The other markets which are predominantly in the small size ranges and are open to much greater competition from alternative suppliers are home automation, healthcare and telematics and sales declined by £200K. This reflects the units supplied to home automation almost halving to 5,000 units, as the Bosch cooktop moves towards end of design life and those supplied to health reduced by nearly two thirds to just 1,000 units.

The group ended the year with twelve regional agreements covering the Americas as they terminated the agreement with one underperforming agent. Looking forward they are likely to terminate a further three agencies but have already agreed terms with two replacements Although previously stating their intention to increase the US-based business, direct sale teams from two to three, a decision was made to delay the recruitment. At the end of the period they had twelve agreements covering the Asia Pacific region. During the year they employed a further indirect employee in Japan and have been working closely with a new VAR for Thailand which they should shortly expect to sign an agreement with.

As of the year-end there was a pipeline of opportunities of £8M compared to £8.2M at the end of last year.

Over the course of the year ZDL has been in dispute with a former licensor, over the process used to write micro-fine wire to a substrate. The licensor alleged that ZDL owed it duties of confidentiality in relation to information alleged to have been imparted to ZDL in 1999 and asserted that ZDL had breached that duty in the content of its MPCT patent applications filed in 2012 and ZDL’s processes infringed that a patent filed by the licensor in 2014 in response to the alleged breach of duty.

A claim was made against ZDL through the patents court. While the group did not accept it was liable, they took a commercial approach to dealing with the claim, mindful of the time and cost associated with high court litigation they made an offer by which they agreed to pay £72K in settlement of the claim, which was accepted with costs of £25K.

Going forward revenues and trading are currently at similar levels as last year and the focus will be to improve margins from production efficiencies and to secure new projects from the launch of the new electronic ASIC controllers.

At the current share price the shares are trading on a PE ratio of 16.4 which falls to 14.7 on next year’s consensus forecast. After the final dividend remained the same the shares are yielding 6.1% which grows to 6.7% on next year’s forecast.

Overall then, this has been a bit of a difficult year for the group. Profits were down, net assets were broadly flat and although the operating cash flow improved, this was due to working capital movements and cash profits declined. There was still a decent amount of free cash generated, however. The gaming market seems to be going well, but the real problem has been the financial market which has been beset by a number of one-off issues. There remains the fact, however, that ATM usage is probably in structural decline. This year has started off on similar levels to last year and although the yield here at 6.7% is impressive, the shares are not overly cheap on a PE level – 14.7. This is a quality, cash generative business but there doesn’t seem to be any evidence of growth here at the moment. Another tricky one, not sure it is worth the gamble at the moment though.