Cambria have now released their final results for the year ended 2018.

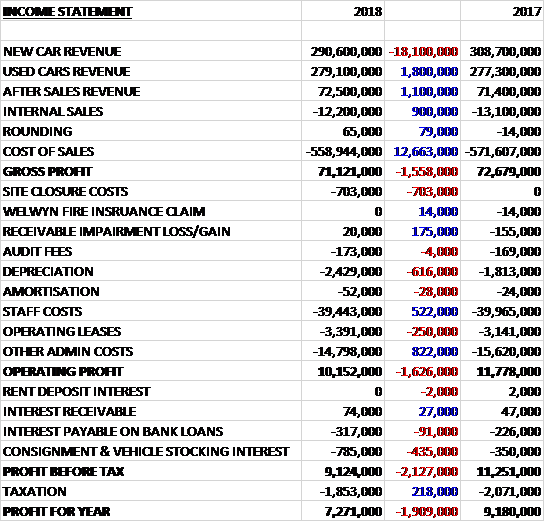

Revenues declined when compared to last year as a growth in after sales and used car revenue was more than offset by an £18.1M decline in new car revenue. Cost of sales declined by £12.7M to give a gross profit £1.6M lower. The group incurred site closure costs of £703K, operating lease payments were up £250K and depreciation increased by £616K, although staff costs declined by £522K and other admin costs were down £890K which meant that the operating profit was £1.6M lower. Consignment and vehicle stocking interest grew by £435K to give a profit of £7.3M, a decline of £1.9M year on year.

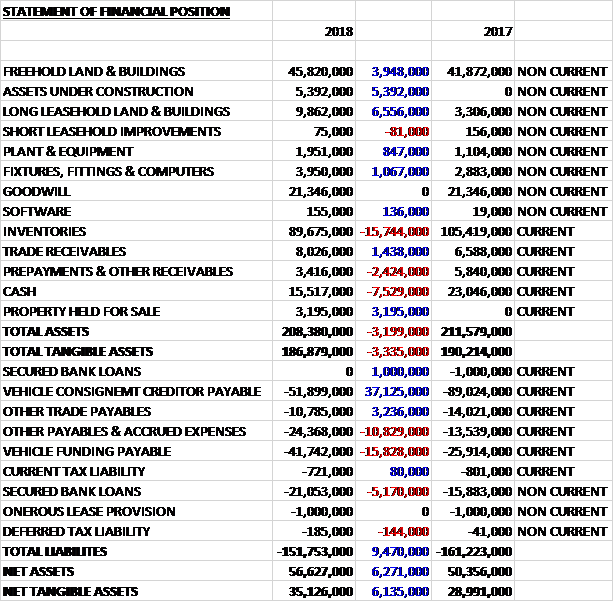

When compared to the end point of last year, total assets declined by £3.2M driven by a £15.7M decrease in inventories, a £7.5M fall in cash and a £2.4M decline in prepayments and other receivables, partially offset by a £6.6M growth in long leasehold land and buildings, a £5.4M growth in assets under construction, a £3.9M increase in freehold land and buildings and a £3.2M property held for sale. Total liabilities declined during the year as a £15.8M increase in vehicle funding payable, a £10.8M growth in other payables and accrued expenses and a £4.2M fall in secure bank loans were more than offset by a £37.1M decline in the vehicle consignment creditor payable and a £3.2M decrease in other trade payables. The end result was a net tangible asset level of £35.1M, a growth of £6.1M year on year.

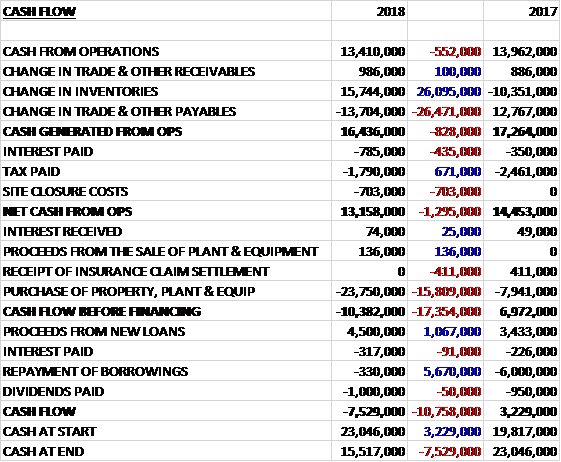

Before movements in working capital, cash profits declined by £552K to £13.4M. There was a cash inflow from working capital but this was slightly less than last time and after interest payments increased by £435K, and the site closure costs of £703K were slightly offset by a £671K reduction in tax payments, the net cash from operations was £13.2M, a decline of £1.3M year on year. The group spent £23.8M on capex to give a cash outflow of £10.4M before financing. They took in £4.5M of new loans and spent £1M on dividends which meant that there was a cash outflow of £7.5M in the year and a cash level of £15.5M at the year-end.

Total funds invested in capex were £23.8M. The Swindon development incurred £6.6M to complete the project, the Hatfield development £5.7M for the land purchase and £5.4M on the development. The Chelmsford and Tunbridge Wells property developments amounted to £1.9M. Including the fitout cost of Swindon and the Tunbridge Wells and Chelmsford developments, there were fixtures, fittings, plant and machinery additions of £3.7M and computer expenditure of £200K.

Over the coming two years the group intends to complete the following major freehold investments: Swindon land freehold purchase at £2.3M, Hatfield JLR, Aston Martin and McLaren completion at £6M, and Solihull Aston Martin at £5M.

This year has seen a difficult new car market that has been impacted by weakening consumer demand in the face of the uncertainty around the Brexit negotiations, inconsistent messaging around the future of diesel engines and the impact on car supply from the change in emissions testing regulations in September. They have also had to cope with the Government driven central cost increases including the Apprenticeship Levy, pension contributions, increases in debit and credit charges and increased property rating costs.

During the year, however, the group has delivered a financial performance with profit slightly ahead of market expectations.

The gross profit in the new car business was £18M, a decline of £3.3M year on year. Revenues decreased by nearly 6% and sales volumes were down 17%. The reduced volumes were partly offset by an improvement in the gross profit per unit sold which increased by 1.2%, a direct reflection of strengthening mix from business additions.

The business has gone through a significant period of disruption with the closure or development of eight of the group’s franchise outlets which caused significant disruption in the day to day operations. The addition of two Lamborghini, two Bentley, one McLaren and a Peugeot franchise will make a major contribution to growth plans, however. The reduction in sales volumes was attributable to reductions in unit sales from certain volume manufacturer partners who have experienced significant reductions in national registrations.

The group’s sales to private individuals was 17.3% lower, new commercial vehicle sales improved by 2% and new fleet unit sales decreased by 42%. The new vehicle registration data showed total registrations were down 6.8% with the registration of cars to private individuals down 4.7%. The sale of diesel engine vehicles was hardest hit as a result of the negative media coverage around diesel engine emissions and sales were down nearly 28%.

The gross profit in the used car business was £24.6M, an increase of £1M when compared to last year. Revenues increased by £1.8M but the number of units sold declined by nearly 7%, partly driven by site closures. The gross profit per unit sold increased by 11.6%. They have focused on increasing the efficiency with which they source, prepare and market their used vehicles which gave rise to a twelve month rolling return on used car investment of 125%, slightly down from the 129% achieved last year.

The gross profit in the aftersales business was £28.5M, a growth of £700K when compared to 2017. Revenues increased by 1.5% with improved margins on the back of the increase in labour hours sold. The 0-3 year car parc continues to be replenished as the increase in new car sales experienced over the previous year’s produces cars ready for aftersales operations, although this is obviously reducing.

To facilitate the development of the Chelmsford and Tumbridge Wells Bentley and Lamborghini sites, the group closed two bodyshops along with an Alfa Romeo and Jeep business in Chelmsford and a Honda and Mazda business in Timbridge Wells. They took the decision to close the loss making Blackburn site in July which comprised of a leasehold showroom for Fiat and Alfa Romeo and the break clause has been exercised. The Renault and Volvo showrooms were owned freehold and are therefore held for sale currently.

The completion of the Swindon JLR facility in July on the group’s long leasehold premises facilitated the relocation of Swindon Land Rover from the property in Royal Wootton Bassett to the new facility. The Wootton Bassett site is now held for sale. After the year-end the group has secured the freehold title of the land in which the development sits from Swindon Borough Council.

The major property development at Hatfield which is due to complete in January 2019 will relocate the group’s JLR and Aston Martin dealerships in Welwyn Garden City which currently operate in short leasehold facilities into a purpose built freehold property with the addition of the McLaren franchise which will operate on the same site.

During the year the Royal Wootton Bassett freehold property was vacated following the transfer of the Land Rover business to the newly developed site in Swindon so have been classified as held for sale. The same is the case for the freehold property at Blackburn following the closure of that dealership.

The group have secured a new development site in Solihull for a permanent facility in line with Aston Martin franchise standards. The group has exchanged contracts and completion is subject to planning permission and the conclusion of extensive highway works to define the site. It is expected that the total freehold investment will be £5M. Due to delays in the highway works, it is now expected that work to the dealership will begin in Q2 2019.

Going forward so far this year trading has been in line with board expectations in September and October and that of last year, supported by strong performances in their used car and aftersales operations. The new car market will see a further reduction in 2018 with forecasts 11.5% lower. There is little doubt that market sentiment has been impacted since the Brexit vote. With the current weakness in Sterling there is ongoing downward pressure on the number of cars registered in the UK as the manufacturer landed cost of imported cars and components increases. Diesel engine vehicles have received the largest negative impact with a significant amount of negative media coverage and clear political positioning in relation to diesel vehicle emissions.

Whilst 2018 delivered a solid set of results, as a result of the uncertainty in the economic outlook the board remains cautious about the new car trading environment in 2019.

At the current share price the shares are trading on a PE ratio 7.9 which falls to 7.4 on next year’s consensus forecast. After the dividend remained the same, the shares are yielding 1.7% which increases to 1.8% next year. At the year-end the group had a net debt position of £5.5M compared to a net cash position of £6.1M at the same point of last year.

On the 4th January the group released a trading update for the first quarter which was in line with board expectations and ahead of the corresponding period last year. As expected the new car market was significantly affected by the impact of the changes in the emissions testing regime from September onwards and the market was down 15.4%. Whilst this led to a reduction in the group’s new vehicle sales, this was offset by improved gross profit. New vehicle unit sales were down 25% with the sale of new retail cars to private buyers down 19%. Some of the volume manufacturer franchises experienced the largest reduction in sales.

The gross profit per unit improved significantly on a total basis as a result the stronger mix from the new franchised outlets representing Bentley, Lamborghini and McLaren. Group profit per unit also improved on a like for like basis and the overall impact of the improved profit per unit mitigated the reduction in unit sales.

Used vehicle sales continued to perform well. Whilst total used unit sales were down 10.5% (like for like down 3%) this unit reduction was offset by continued improvement in gross profit per unit. The significant changes in portfolio mix and closure of the Blackburn site last year had a material impact on sales volumes but as a result of the improved profit per unit, the like for like profit from the division improved year on year. The group’s aftersales operations delivered a good performance, with revenue increasing by 1.9% and gross profit up 6.5%.

The group opened its second Lamborghini dealership in November alongside the Bentley dealership in Tunbridge Wells. The major property development for JLR, Aston Martin and McLaren at Hatfield is progressing well and the JLR facility was completed for occupation in December as planned. It is now expected that the Aston Martin and McLaren facility will be ready in February. In December they completed the sale of the Wootton Bassett freehold property for £2.8M.

The board remain cautious about the general uncertainty in the economy and around the consumer environment, particularly the ongoing uncertainty around Brexit. The new luxury franchises and other redevelopments leaves the business well positioned for the year ahead, however. All very non-committal!

Overall than this has been a difficult period for the group. Profits were down, the operating cash flow deteriorated with no free cash being generated, although next year capex seems like it’s going to reduce. Net assets did improve, however. There was a lot of disruption from the investments being made but the real issue is a declining market due to uncertainty over Brexit, weakening Sterling and the issues surrounding diesel emissions. Profits in used cars and aftersales offset the decline in new car profits and the volume declines were offset by increases in unit profits due to an improving mix.

One issue that I am concerned about is that the reduction in new car sales will at some point have a knock on effect on aftersales as less people have purchased cars and the debt levels are creeping up. Still, this is potentially priced in with a forward PE of 7.4 and yield of 1.8%. This is a tricky one, it could be an interesting value play but obviously not without risks as mentioned above.

On the 6th March the group released a trading update covering the first five months of the year which was ahead of the same period last year, both on a total and like for like basis.

During the period the new car market has been significantly affected by a number of factors including the impact of the changes in the emissions testing regime and the negative impact of the weak sterling position on the imported price of the cars which has led to price increases for many manufacturers. In the period, the total new car market was down just over 10%. The diesel segment of the market was worst hit, down 30%.

Supply side market influences have contributed to a reduction in the group’s new vehicle sales, although this was partly offset by improved gross profit per unit in the like for like businesses and fully offset by the improved gross profit per unit across the total group as a result of the stronger mix from the new Bentley, Lamborghini and McLaren outlets. New vehicle unit sales for the period were down 23% (like for like 20%) although he prior year comparative included a low margin commercial vehicle deal which has not been repeated. The sales of new retail cars to private purchasers was down 16% (like for like 11%).

Used vehicle sales continued to perform well. Total used unit sales were down 11% (like for like 4%) but this unit reduction was offset by an improvement in the gross profit per unit. The significant changes to the franchise portfolio mix and closure of the Blackburn site in the prior year had a material impact on sales volumes but as a result of the improved profit per unit, both the total and like for like profit from the business improved year on year.

The group’s aftersales operations delivered a good performance with revenue increasing by 7% (like for like 3%), gross profit up 4% (like for like 2%) and aftersales contribution up 10% (like for like 7%).

Going forward, whilst challenges remain given the ongoing uncertainty around Brexit and the terms of the UK’s departure from the EU, the group’s ongoing franchising development activities have enhanced their dealership portfolio mix and the changed made in the prior year have further benefited the group. These new businesses are still in their infancy, but have exciting potential.