Games Workshop have now released their interim results for the year ending 2019.

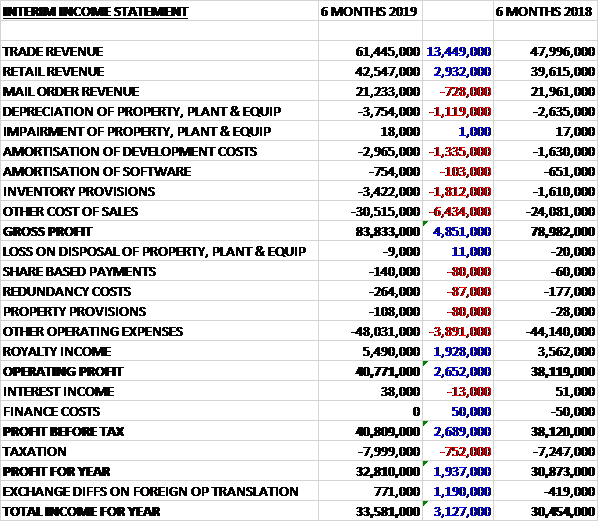

Revenues increased when compared to the first half of last year as a £728K decrease in mail order revenue was more than offset by a £13.4M growth in trade revenue and a £2.9M increase in retail revenue. Depreciation was up £1.1M, amortisation increased by £1.4M, inventory provisions rose by £1.8M and other cost of sales were £6.4M higher to give a gross profit £4.9M above that of last time. Operating expenses increased by £3.9M but the royalty income grew by £1.9M which meant that the operating profit was £2.7M higher. Finance costs were broadly similar but tax charges were up £752K to give a profit for the period of £32.8M, a growth of £1.9M year on year.

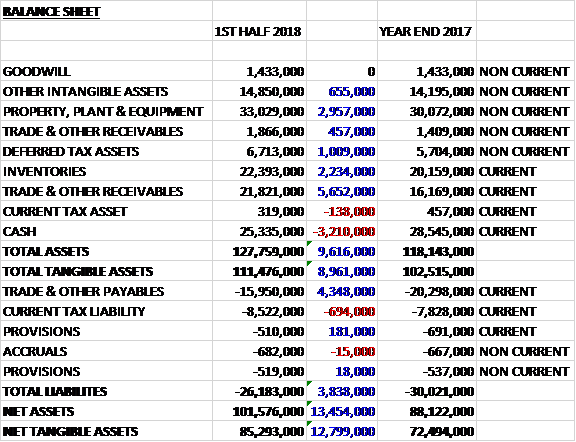

When compared to the end point of last year, total assets increased by £9.6M driven by a £6.1M growth in receivables, a £3M increase in property, plant and equipment, a £2.2M growth in inventories and a £1M increase in deferred tax assets, partially offset by a £3.2M decline in cash. Total liabilities declined during the period, mainly due to a £4.3M fall in payables. The end result was a net tangible asset level of £85.3M, a growth of £12.8M over the past six months.

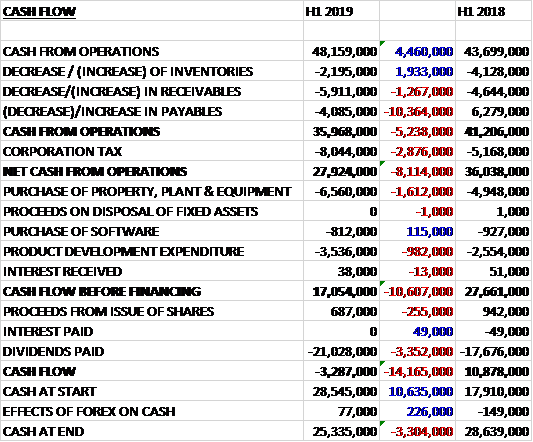

Before movements in working capital, cash profits increased by £4.5M to £48.2M. There was a cash outflow from working capital and after tax charges increased by £2.9M the net cash from operations was £27.9M, a decline of £8.1M year on year. The group spent £6.6M on property, plant and equipment, £3.5M on development expenditure and £812K on software to give a free cash flow of £17.1M. This didn’t quite cover the £21M paid out in dividends so there was a cash outflow of £3.3M and a cash level of £25.3M at the period-end.

The operating profit in the Trade business was £22.5M, a growth of £5.3M year on year with growth in all territories. The net number of trade outlets increased by 300 accounts which helped drive forward sales. A large number of independent retailers now also sell the group’s products online.

The operating profit in the Retail business was £4.8M, an increase of £1.9M when compared to the first half of last year. There was growth in all territories except Australia and New Zealand. They opened 23 stores and closed 5 with recruiting new store managers an area of focus.

The operating profit in the Online business was £13.1M, a decline of £566K when compared to the first half of last year. Sales in the Citadel online shop were flat and the Forge World and Black Library stores declined slightly. Sales of digital titles remain comparable to last year and the group continue to increase the functionality of their online stores.

The operating profit in the Product and Supply business was £9.6M, a decrease of £3.5M year on year. The operating profit from Royalties was £5M, a growth of £1.8M when compared to the first half of last year reflecting the change in accounting mentioned below.

As the group moves to complete a series of major investment projects, the gross margin and stock levels are now currently where they’d like them to be. The completion of the new Nottingham factory and ERP projects will allow them to fully optimise their Nottingham site. From there, they will begin to upgrade their warehousing capacity in both Memphis and Nottingham. These further investments will help them maintain their current volumes, increase efficiencies and give good scope for sales growth in the future.

The community website continues to increase its readership with visitor numbers up 30% with almost a million visits to the site per week. Elsewhere on social media they have over 250,000 people signed up to the Warhammer.tv site.

There have been a number of accounting changes that have had the effect of reducing EPS by 0.7p. Amounts receivable from customers in respect of delivery charges are now recognised as revenue when previously the income was offset against delivery charges in cost of sales. Also the minimum royalty guarantee will be recognised in full at inception of the contract when previously it was deferred and recognised in accruals and deferred income and released with licensee sales.

Going forward, December trading continued in line with the performance in the first half.

At the current share price the shares are trading on a PE ratio of 16.2 which increases to 17 on the full year forecast. After an increase in the dividends the shares are yielding 4.4% which falls to 4.1% on the full year forecast. At the period-end the group had a net cash position of £25.3M compared to £28.6M at the same point last year.

Overall then the group had a pretty decent period overall. Profits were up, net assets increased but the operating cash flow deteriorated somewhat with the dividends not quite being covered by free cash. This was due to adverse working capital movements related to the recent investments being made, however, and free cash saw an improvement. The trade and retail sectors are performing well but there was a bit of a blip in online. The reason for this wasn’t really given so this is a bit concerning. The shares are also no longer that cheap with a forward PE of 17 and yield of 4.1%. I do feel this is a great company but not sure the value is quite right at the moment.

On the 12th April the group announced that trading has continued well. Compared to last year, sales and profits are ahead. Royalties receivable are also ahead of the prior year following the signing of new license agreements. The board’s current expectation is that pre-tax profit for the year will be around £80M.

On the 7th June the group released a trading update covering the year. They expect sales to be £254M and the group’s pre-tax profit to be at least £80M. Royalties receivable from licensing are around £11M.