Naibu has now released their full year results for 2013.

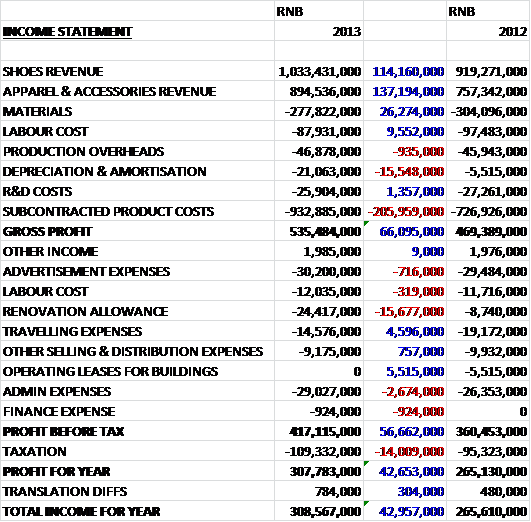

Revenue increased across both sectors, up £11.4M in shoes, driven by increased sales price per unit and £13.7M in apparel and accessories, achieved by increasing the number of outlets and increasing the display areas for clothes. Material costs also fell due to the fact the group is making less shoes than it was last year, and similarly labour costs were down due to the closed lines in the factory. Depreciation, at £2.1M increased by £1.6M but it was subcontractor costs that was the largest increase, up £20.6M due to the shoes that are now manufactured externally after the labour problems in the new factory. The only real admin expense to increase considerably was the renovation allowance that was up £1.6M during the period. The small finance expense relates to foreign exchange losses due to depreciation in the HK Dollar. A higher tax rate then meant that the profit for the year was some £4.3M higher than in 2012 at £30.8M.

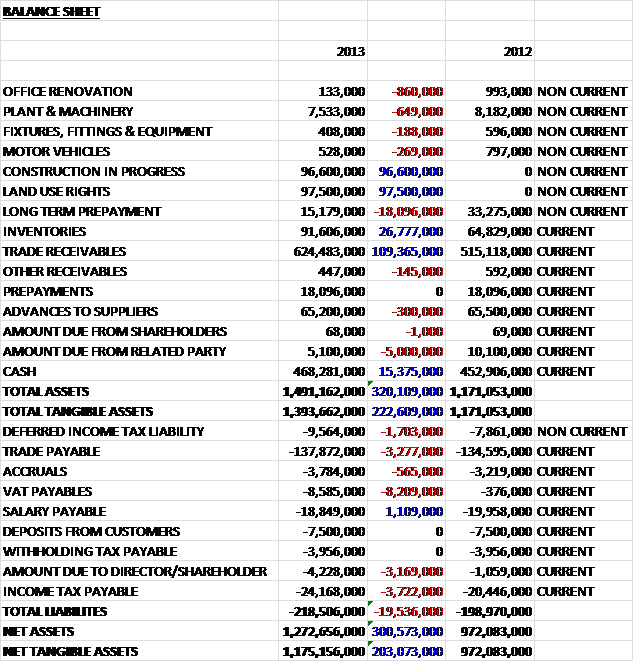

Overall assets increased by £32M. This increase was driven by a £10.9M growth in trade receivables, a £2.7M hike in inventories plus £9.8M and £9.7M worth of land use rights and construction in progress respectively(relating to the Quangang factory), only very slightly counteracted by a £1.8M fall in long term prepayments, relating to the amortisation of store renovation payments. Liabilities also increased with the largest growth being a £821K increase in VAT payable. Net assets at the year end point were some £30M higher at £127.3M which seems like good progress to me.

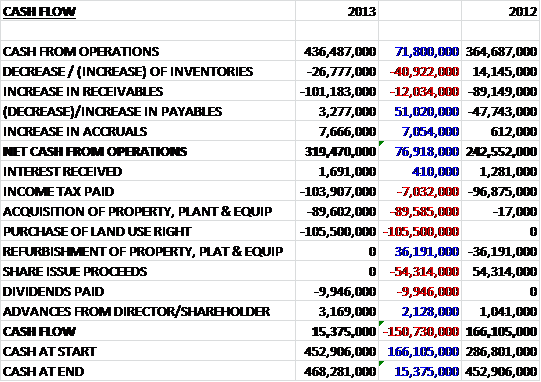

Before movements in working capital, cash from operations was some £7.2M higher at £43.7M. An increase in inventories and receivables, however, pushed the net cash from operations down to £31.9M, still some £7.7M better than last year. Although the average trade receivable turnover days fell from 121 to 106 days, this still seems rather high. The group then spent quite a bit on capital expenditure, £9M on the acquisition of property, plant & equipment and £10.6M on the purchase of land use rights. After dividend payments of just under £1M the cash flow for the year was a still respectable £1.5M but it was £15.1M lower than in 2012 due to the capital expenditure this year.

Profit in the shoes segment stood at £21.3M which was very similar to the profit recorded in the Apparel & Accessories segment, which was £21.2M. Management expect competition to intensify in 2014 as other branded sportswear companies continue to push into tier three and four cities. Having said that, the Chinese government is determined to restructure the economy, encouraging internal demand and continue the process of urbanisation which suggests the market does have good growth potential in the medium term. The group plans to expand its market in Western China and seem to be making this a priority. They have developed a new brand (Nibo) which is based on a European fashion concept and is due to be launched in 2015.

In September 2013 the group signed an agreement to purchase land use rights to develop a Naibu Industrial Zone. This zone will include R&D, manufacturing and logistics facilities relating to the development of shoes, apparel and sports equipment and will be in Dazhu County, Sichuan Province. The group will pay £6M for the rights, £800K having been already paid as a deposit. It is expected that the total cost of the project will be in the region of £30M and there will also be a new factory with 12 production lines.

Operations in the new Quangang plant have not commenced as planned due to an unexpected shortage in labour pushing labour costs up. If unsufficient workers can be found for six production lines to begin production by August the group will consider disposing of the new factory, which seems like a pretty ridiculous situation to be in. In the meantime, the group is continuing to produce shoes at the Jinjiang facility but the majority of shoe production is being outsourced as there only seems to be two production lines at the plant. The Dazhu factory, in the new Industrial zone is due to be operational in early 2016, although if they can’t find the staff for that one, who knows what will happen.

Overall then, profits were up in both product markets, net assets continued to rise and the group was cash generative even after the heavy capital expenditure. The final dividend remains unchanged at 4p and at the current share price the dividend yield is a stonking 10.5%, rising to 11.4% on analyst forecasts next year. The shares are arguably even more undervalued on the P/E ratio level as at the current price this stands at just 1.1. Niggling doubts remain about the legitimacy of the company, however, and the situation at the Quangang seems ridiculous – a new factory has been built but there are no staff to work in it! The fact remains that this company is ridiculously undervalued if it is legitimate, however, and I still see this as a strong hold.

On the 5th August the group released a statement covering trading during the first half of the year. Revenue grew by 8.4% when compared to the same period of last year but this was overshadowed by the news that they have failed to find enough workers for their newly acquired factory and because the shortage of labour is expected to continue for the forseeable future, they have put the factory up for sale. In the interim, the shoes will be subcontracted to other companies. In Dazhu, the group paid the second installment of £3M for land use rights, with the final tranche of £2.2M due when the land use certificate is granted, which is expected to be in October. The factory should be operational by Q2 2016. I have to say this is looking rather poor. Why did Naibu not forsee a labour shortage? Why will anyone else be interested in taking over a factory they can’t staff? Why go to the expense of acquiring the factory if the shoes can be manufactured by OEMs at a similar cost? What will happen to all the cash spent on the factory? I have to say, that without answers to the above this is looking a more and more risky investment.