Shaft Sinkers have now released their full year results for the year ending 2013.

![shaftincome2013]](http://www.shareresearch.co.uk/wp-content/uploads/2014/07/shaftincome2013.png)

Revenues were substantially down on last year driven by a £66.5M fall in South African sales, somewhat mitigated by a £26.1M increase in revenue from the rest of the world. There was some progress on staff costs, down by just under £41M with other direct expenses increasing slightly. This lead to a gross profit some £2.6M lower than last year. There was £1M less depreciation compared to 2012 and £1.4M was made on the sale of property relating to an office in South Africa which has been sold and leased back, but £2.7M less was made on foreign exchange conversion and at £3.9M legal fees were £2.8M higher than last year and starting to take their toll on results. Other operating costs were substantially lower, though, so operating profit was “just” £1.4M lower than in 2012 at £3.9M (there would have been an improvement on last year had the legal fees remained the same). As far as financial costs were concerned, there was £479K less paid on loan interest and £411K less interest paid to revenue authorities. A slightly lower tax bill then made the profit for the year £363K down on 2012 at £2.1M.

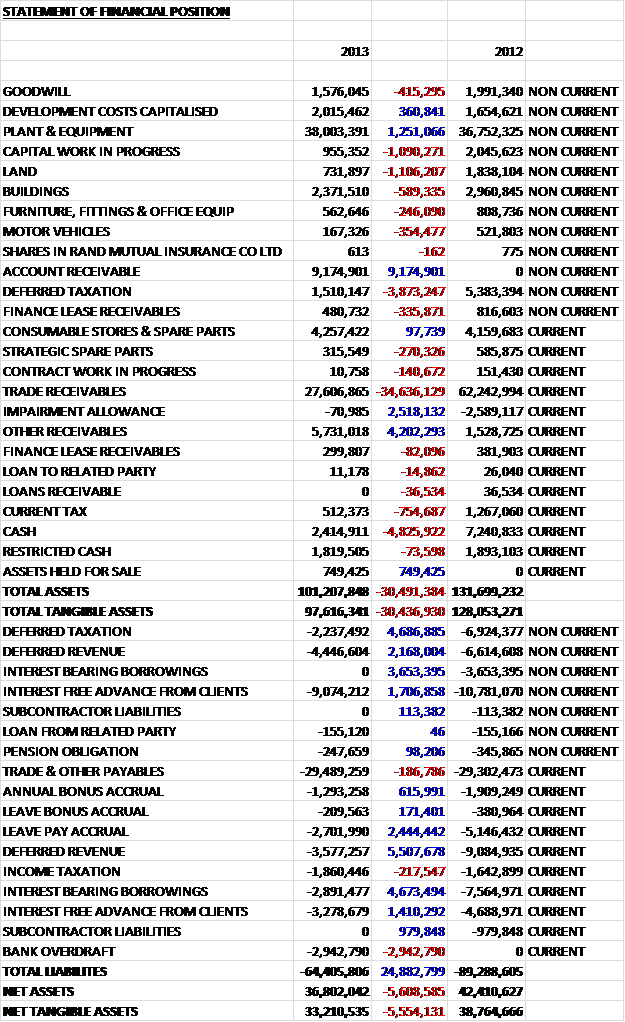

Overall assets fell by£30.5M when compared to the end point of last year. The fall was predominantly driven by a £34.6M decline in the value of receivables but a £4.8M fall in cash and a £3.9M decline in deferred taxation assets did not help. These were only partially mitigated by £9.2m of account receivable, relating to the quantity that the group is trying to claim from Eurochem (moved from receivables), and a £4.2M increase in other receivables. The small increase in development costs capitalised relates to automated mine shaft inspection IP. Total liabilities also fell during the year driven by a £5.5M fall deferred revenues, a £4.7M fall in deferred taxation, an £8.3M decline in borrowings, a £2.4M reduction in leave pay accrual and a £2.2M decline in deferred revenue, although the overdraft did increase by £2.9M. The result of all this is that net tangible assets fell by £5.6M to £33.1M which is rather disappointing.

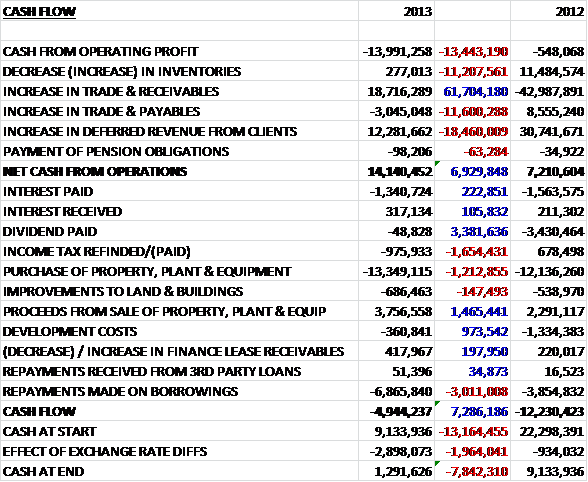

Before movements in working capital, there was a pretty terrible £14M cash outflow. A huge swing in receivables and a £12.3M cash advance from clients meant that the net cash from operations was £14.1M, some £7M better than last year. Sadly this did not quite cover the £13.3M spent on plant and equipment and £1.3M in interest. The group did manage to claw £3.8M back from flogging a South African office and this helped to repay £6.9M of borrowings resulting in a £5M cash outflow. This leaves the cash level at the end of the year at precarious £1.3M, although borrowings are now fairly negligible it is a bit of a concern that this cash flow includes quite a lot of deferred income.

The group is still feeling the effects of the legal proceedings with Eurochem with higher legal fees. The outcome of the proceedings will only be of practical effect in early 2015 but the case is going to take its toll before then.

South African profit before tax was £1.2M, down from £4.5M in 2012. The operations were significantly impacted by the difficult operating environment this year and some contracts were cancelled in response to declining commodity prices and rising operating costs in the country. There were a number of contract extensions awarded, however, with Afplats, Lonmin and Impala agreeing to an additional £47.6M of work. During the year, the group managed to reduce the level of outstanding variation orders during the first half of the year but unfortunately they began to grow again during the second half.

There have been a number of cost cutting initiatives such as removing one layer of operational management and the reduction of South Africa headcount but this was offset by significant underperformance from a number of operations with Impala 17 and Styldrift being particularly disappointing. Styldrift suffered poor performance over the last two months of the year due to “poor planning”. The Impala 17 project was severely impacted by safety stoppages and a generally poor safety record during the year. A third party health and safety expert firm is performing an independent assessment and it found a number of issues that were not dealt with effectively and a number of recommendations have since been adopted in order to improve safety reporting. As a result, the group lost £600K on the project during the year and a further £900K so far in the next year. Some new financial terms have been agreed which should improve the financial performance of the project from April 2014 but Impala is retendering the project from September which is a real blow and reduces the order book, post balance sheet date, by another £13.9M. The Moab project was terminated and the group has some unrecovered costs relating to that.

After the end of the year, a further strike was initiated affecting South Africa’s platinum producers which led to suspended operations at Impala 16 and Lonmin and the current situation seems to be deadlocked with little signs of movement. Shaft’s employees are not on strike but they have been prevented from working at the affected sites. There are contractual provisions to ensure the group can recover some costs on the event that clients are affected by strikes but the action will still affect profitability on those projects.

The METS division managed a project to design, engineer and supervise the manufacture of the head gears for the Hindustan Zinc project. It also designed a new main sinking methodology that gives a safer and more cost effective sinking operation, particularly for shallower ventilation shafts. This new method was used on the Hindustan Zinc project.

ROW profit before tax was £3.1M, up from £580K last year. Work at the Kibali goldmines project in the DR Congo proceeded well, and the start of the main sinking phase proceeded in November. The project has performed in line with budget and the shaft reached a depth of 483m ahead of schedule. The Hindustan Zinc project progressed more slowly than expected due to problems with a civil engineering subcontractor during the first half of the year. The group dismissed the contractor and took charge of the responsibilities themselves, however progress in the second half of the year continued to be poor which resulted in higher than expected costs and lower revenues as they are inked to the speed that the shaft is sunk. Some mitigating measures have been undertaken and it is currently experiencing a much better performance.

During the year the group completed collaborations with China Nonferrous Metal Industry’s Foreign Engineering and Construction Co and India’s Tata Projects ltd which should improve market access to those two countries. There was also an early stage collaboration with Laing O’Rourke in the UK.

The outlook for 2014 remains difficult and there is no clear sign of when sentiment will improve. The situation with industrial action in South Africa is also very concerning, with no real prospect of it being resolved any time soon. However, it could be argued that at times of less capital expenditure, mining companies may be tempted to focus on extending the life of existing mines with further shaft sinking opportunities. The order book declined when compared to the end of last year but remained fairly significant at £238M but the group were not awarded any new contracts during the period, although there are outstanding tenders to the value of £970M. The Kazchrome contract remains unallocated and I suspect it will not be awarded until the client knows Shaft can fight off the legal claims which will destroy the group should they be found guilty. The group expect cash flow to be tight in the coming year, which does not bode well.

Although the group’s net debt position has improved to £1.6M, this is made up of £1.8M worth of restricted cash which is held by Standard Bank as a security for a performance guarantee issued in respect of a project and these funds remain restricted as long as this performance guarantee remains in place. There is also a £2.9M payment on the loan due in December 2014. At the current share price the P/E ratio is 1.7 but there don’t seem to be any forecasts for future earnings. Due to the difficult year the board has sensibly not recommended a final dividend. Things seem to be very hard for Shaft. Until the end of the legal claims, I can’t see them winning any more contracts. The HZC problems are a shame and the ongoing issues in South Africa are going to squeeze cash flow in the coming year. I have very little value left here but if I did, I would sell.

On the 19th May the group released an interim statement covering the first quarter of the year. Things are not going well.

The group experienced significantly lower margins as a result of operational underperformance and higher operational costs which lead to a loss before tax of £2.7M, some £700K worse than the same period of last year. This means that the group is experiencing an increasingly tight cash position and is selling assets and trying to recover receivables – desperate stuff.

The Kibali project continues to be the one shining light, performing in line with expectations. The progress at the HZL project showed improved progress due to measures implemented at the end of last year and the North ventilation shaft has now been started. The main shaft sinking was still behind schedule, however, which resulted in reduced revenues. Continued industrial action in South Africa resulted in the suspension of work at Lonmin and Impala 16 which impacted revenues and profits in those projects. Operational underperformance continued at Impala 17, impacted by continued safety stoppages. Performance at Styldrift was below expectations due to poor operational performance on the main and service shafts and subsequent delays in the construction of underground infrastructure. The group experienced good performance at the Leeuwkop project as a number of issues that occurred at the end of last year were resolved.

The group’s net debt position is now at £3.3M and there were no significant developments relating to the Eurochem claim. The arbitral hearings will take place in June and legal fees during the period were £1.2M. Although things seem to be improving outside South Africa, there continue to be real issues within the country and with the increasingly tight cash position, things are not looking good for Shaft.

On the 10th July the group released a statement that should come to no surprise. Since May their cash position has further deteriorated to the extent that it has engaged with various parties regarding the urgent provision of new financing to satisfy near-term liquidity requirements. Negotiations are continuing with the objective of preserving value for shareholders whilst also enabling the company to continue trading. Things sound very serious now and I would be quite surprised if shareholders come out of it with much value intact.

On the 23rd July the group announced additional work awarded by Afplats on its Leeuwkop project. The work involves the continuation of sinking activities on the main shaft from a depth of 984m to 1,307m as well as the construction of two station breakaways for the establishment of horizontal tunnels to access the ore body at depths of 1,207m and 1,237m. The work is scheduled to complete in the second half of 2015 and has a total value of £7M. Clearly this is good news but in reality it is a drop in the ocean compared to the other woes that the group is experiencing.

On the 6th August the group announced that it had signed a contract worth £37M with Kazchrome which will entail the sinking of the Skipovaya vertical shaft to access the ferrochrome ore body which will be mined to supply the Donskoy processing plant in Kazakhstan. The scope of the work will include the sinking and lining of an 8m diameter skip shaft to a depth of 1,453m. The contract starts in September this year and is due to be complete in 2018. It is good that the group has finally wrapped this up after many months of negotiations. It is not a huge contract, but represents further diversification and potentially a much needed source of initial cash flow.

On the 22nd August the group announced that it had entered into a loan agreement wit Hillside Intl where they will loan the group £3.5M to provide Shaft with adequate working capital to secure a funding package appropriate to its longer term needs. In that regard, the board has commenced preparations to raise up to £9.2M by way of an issue of convertible loan notes and at this time the loan from Hillside will be repaid and they will subscribe to £3.5M of the loan notes. The Hillside loan is repayable on the 21st November when the group will pay Hillside a few of 2%. should the loan not be paid back at this point, this will increase to 20%. As part of the agreement Hillside will appoint two directors to the board, Mr. Robin Haller and Mr. Alexander Haller. Current shareholders will be invited to subscribe to €5M of the loan notes by way of an open offer. It is currently envisaged that the loan notes will be denominated in notes of £10,000 with an issue price of £7,200 per note and a redemption price of £10,000. The notes will have a maturity date of three years.

The minimum amount raised on the notes will be £3.5M plus €2.4M and the maximum is anticipated to be £9.2M. In the event that the maxim is raised and all notes are converted into ordinary shares, the percentage of voting rights represented by them will be 78%. This is a pretty huge dilution for the current share holders. The conversion price will be equal to 7.639p and the effective subscription price in the event of conversion is 5.5p. Also announced at the same time, the Chairman, Stephen Oke and non-exec director Roger Williams resigned from the board with immediate effect. Overall then, this represents a potential huge dilution for current share holders and at £7,200 per note, this is quite a gamble for a company that will not be in existence if it loses the court case. I am reluctant to take these up.

On the 26th August, the group announced that it had replaced Stephen Oke with Marius Heyns as chairman. Marius has long experience in civil engineering and before taking up the role spent ten years as CEO of South African engineering group Basil Read.

On the 1st October the group announced that it has increased the cash loaned from Hillside immediately to £5M, an increase of £1.5M. This now means that Hillside will subscribe £5M for Convertable Loan Notes. Also it was announced that they were unsuccessful in the retendered Impala 17 contract. Whilst the loss of the contract itself is disappointing, it was not a bit earner for the group but this might affect the other Impala contract. Also, the fact that Shaft need to find an extra £1.5M of cash immediately is a bit of a concern. This is all looking like a bit too much of an ask to retain much value here so I have decided to sell out. This has been a disaster really!