AG Barr has now released its final results for the year ended 2018.

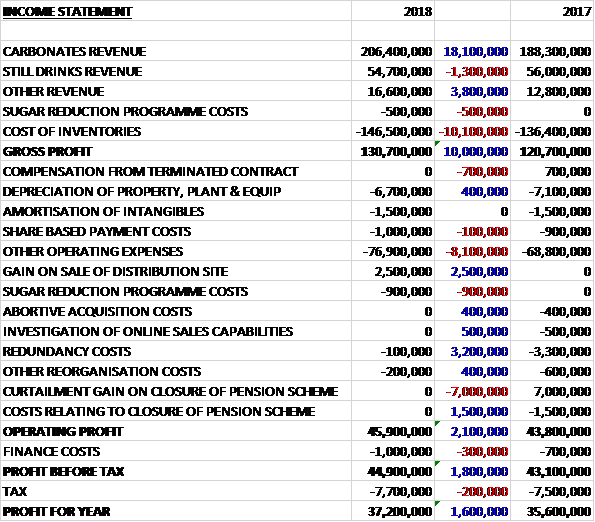

Revenue increased when compared to last year as a £1.3M reduction in still drinks revenue was more than offset by an £18.1M increase in carbonates revenue and a £3.8M growth in other revenue. There was a £500K cost associated with the sugar reduction programme and other cost of sales increased by £10.1M to give a gross profit £10M higher. Depreciation was down £400K but there was no compensation from terminated contracts, which brought in £700K last year, and other operating expenses grew by £8.1M. There was a £2.5M gain on the sale of the distribution site, however, and a £900K admin cost associated with the sugar reduction programme. We also see no pension income, which was £5.5M last time, and redundancy costs fell by £3.2M. All of this meant that the operating profit was £2.1M higher. Finance costs increased by £300K and tax charges were up £200K to give a profit for the year of £37.2M, a growth of £1.6M year on year.

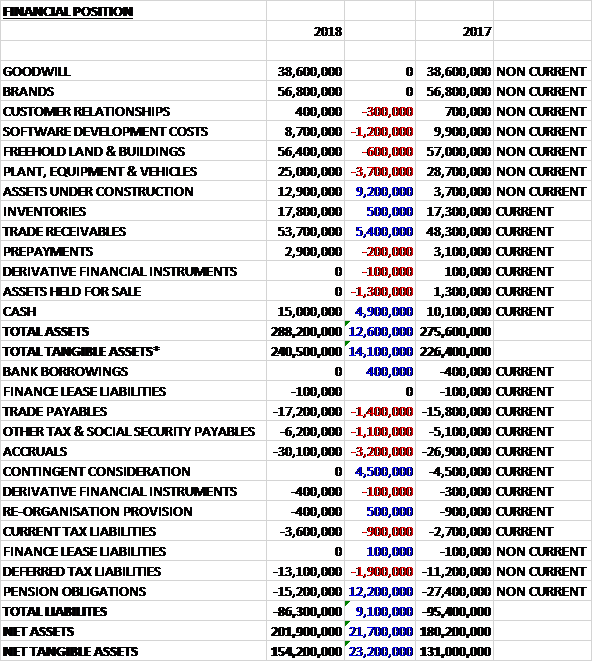

When compared to the end point of last year, total assets increased by £12.6M driven by a £9.2M growth of assets under construction, a £5.4M increase in trade receivables and a £4.9M growth in cash partially offset by a £3.7M fall in plant, equipment and vehicles, a £1.3M decline in assets held for sale and a £1.2M decrease in software development costs. Total liabilities declined during the year as a £3.2M increase in accruals and a £1.9M growth in deferred tax liabilities were more than offset by a £12.2M decrease in pension obligations and a £4.5M decline in contingent consideration. The end result was a net tangible asset level of £154.2M, a growth of £23.2M year on year.

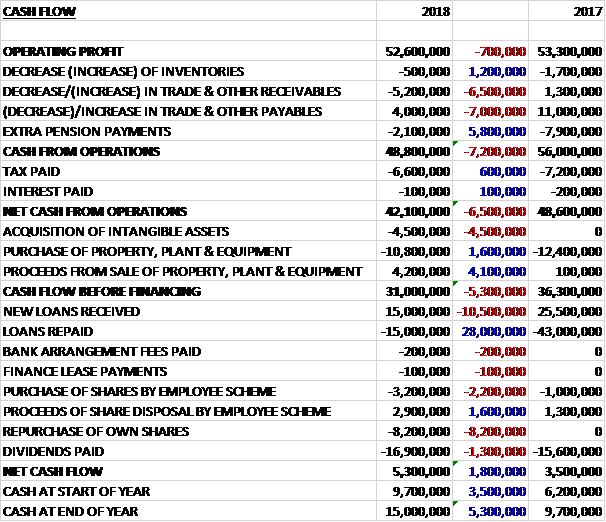

Before movements in working capital, cash profits declined by £700K to £52.6M. There was a cash outflow from working capital and despite tax and interest payments reducing by £700K the net cash from operations came in at £42.1M, a decline of £6.5M year on year. The group spent £4.5M on intangible assets, and £10.8M on property, plant and equipment, although they recouped £4.2M from the sale of a property to give a free cash flow of £31M. There was a neutral loan position but £8.2M was spent buying back shares and £16.9M was paid out in dividends. This all gave a cash flow of £5.3M and a cash level of £15M at the year-end.

The gross profit in the Carbonates division was £104.3M, a growth of £7M year on year. Irn-Bru sales were up 5.7% in volume and 8% in revenue. Barr Flavours, KA, Sun Exotic and OMJ have all delivered volume growth. The Rockstar brand had a strong year, delivering double digit volume gains and maintaining pricing in the face of strong completion.

The gross profit in the still drinks and water division was £18.1M, an increase of £1.1M when compared to last year. This is despite some supply driven constraints for Snapple in the earlier part of the year. Revenue was down 2.3% but margins improved considerably.

After several years of double digit revenue growth the international business grew revenue by just 3.8% as a result of the continued export drive by the Funkin business, tempered by complexities created by the reformulation programme and some local distributor changes.

The Funkin business continued to perform strongly with sales growth of 25%. The key on-trade business has grown volume and margins in each of its product segments, benefiting from continued cocktail growth. The drive into take-home with the brand has started with the launch of the shaker pack in supermarkets. A £4.5M cash earn-out accrued at the time of acquisition was paid to the previous owners of the brand during the year.

The UK soft drinks market has performed reasonably well across the last year with value growth of 2.9% and volume growth of 0.5%, reflecting the underlying inflationary environment. The key driver of value growth has been branded carbonates, where some significant reductions in promotional investment have led to higher realised prices but lower volumes. The water category continues to drive volume growth, generally at the expense of value. Against this backdrop the group saw value growth of 8.7% and volume up 7.7% with market share growth balanced across sales channels.

Irn-Bru sales were up 8%, Rubicon sales increased by 5.3% and Funkin sales grew by 25%. Across the franchise brands, Rockstar had a good year with sales up 14.3% due to product distribution growth and growth in new overseas territories. Snapple, however, saw a reduction in volumes as a result of retailer range rationalisation in a small number of European markets and some supply issues across Q2 and Q3. Overseas sales were up just 3.8%, reflecting the complexity of the reformulation programme created in their export led international model and some local distributor changes.

The group have announced a new long-term partnership agreement with San Benedetto. From January 2018, the group became the exclusive UK and Ireland distributor of San Benedetto’s Prima Spremitura sparkling citrus fruit drinks. The group have also added another new brand partner – Bundaberg Brewed Drinks. Starting in April 2018, they have entered into an exclusive long term agreement in relation to the brand in the UK. Best known for its Ginger Beer, the Australian brand is already established in the UK.

Over the past year the group has added further production capacity with the installation of a new PET bottling production line at Milton Keynes, at a capital cost of £10M. They have also started a replacement to their syrup room in Cumbernauld. Capex in 2019 is expected to be at a slightly higher level than this year, primarily driven by the phasing of the last payment on the PET line, the continuation of the syrup room upgrade and the ongoing maintenance and optimisation programmes.

Margins have been negatively impacted by the continued weakness in Sterling, affecting input costs such as sugar and packaging which are prices in Euros.

In response to changing consumer requirements, the group have extended their reformulation programme, taken in advance of the implementation of the soft drunks industry levy in April. They now expect that up to 99% of the portfolio will contain less than 5g of sugar per 100ml. Whilst it is still early days, apparently the consumer response to the new product has been encouraging.

During the period there was a £2.5M gain on sale made on the disposal of the Walthamstow distribution asset. There have so far been £1.4M of costs incurred as part of the ongoing sugar reduction programme which has exceeded the level of expenditure that would normally be incurred in the course of new product development.

Going forward the UK economic landscape is expected to remain uncertain for business as a whole with regulation, changing customer dynamics and consumer preferences adding further volatility to the soft drinks industry. The board remain confident in their ability to grow the business and deliver long-term value, however.

At the current share price the shares are trading on a PE ratio of 23.5 which falls to 21.9 on next year’s consensus forecast. After an 8% increase in the total dividend, the shares are yielding 2.4% which increases to 2.6% on next year’s forecast. At the year-end the group had a net cash position of £15M compared to £9.7M at the end of last year.

On the 30th May the group announced that finance director Stuart Lorimer purchased 7,164 shares at a value of just under £50K.

Overall then this has been a decent year for the group. Profits were up and net assets increased. The operating cash flow did decline but free cash generation remained healthy. The carbonates business did well, with all segments seeing growth and still drinks also performed well despite some supply issues around Snapple. The market in general has been OK, with lower promotional activity giving rise to higher values and the group has outperformed the market.

There are some issues, the continued weakness in Sterling is unhelpful and the reformulation programme obviously carries with it some risks. The share are also not cheap with a forward PE of 21.9 and yield of 2.6%. Despite this, there is net cash and these shares seem a solid prospect so I continue to hold.

On the 1st August the group released a trading update covering the first half of the year. Revenues are expected to increase by 5%. The soft drinks market as a whole was up 4.5% in value terms and 1.4% in volume. It benefited from hot early summer weather across the UK and the value increase associated with the implantation of the Soft Drinks Industrial Levy in April.

In the period they completed the implantation of their reformulation programme and have grown market share. The Irn-Bru brand in particular has continued its positive growth momentum, with regular Irn-Bru increasing its volume and value share of the total soft drinks market alongside strong growth in Irn-Bru Xtra.

There was further growth in Rubicon Spring and Street Drinks by Rubicon has recently been launched. The new partnership brands, San Benedetto and Bundaberg have made encouraging early progress and Funkin continues to perform strongly.

Going forward, the external landscape remains volatile. In addition they have seen the implementation of the Soft Drinks levy, the impact of which is still to be fully determined. The group have been investing in their brands and people which has a moderate impact on margins in the current year but overall full year profit expectations remain unchanged.