Trifast has now released their final results for the year ended 2018.

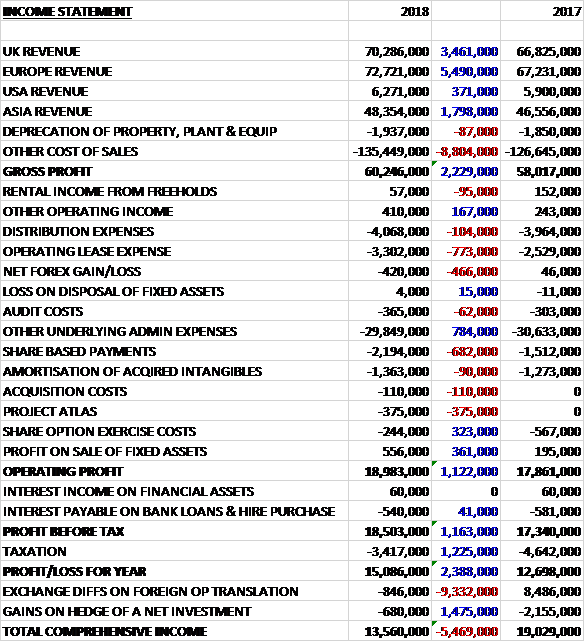

Revenues increased when compared to last year due to a £5.5M growth in European revenue, a £3.5M increase in UK revenue, a £1.8M growth in Asian revenue and a £371K increase in US revenue. Cost of sales was also up to give a gross profit £2.2M higher. There was a £773K increase in operating lease payments and a £466K negative swing to forex losses but other underlying admin expenses increased by £784K. Share based payments were also up £682K but there was a £361K increase in the profit from asset sales to give an operating profit £1.1M higher. Tax charges fell by £1.2M reflecting historic EU loss relief claims in the UK and EU dividend relief claims to cover dividends paid up to Trifast PLC up to 2009 (£1.2M net effect), which meant that the profit for the year was £15.1M, a growth of £2.4M year on year.

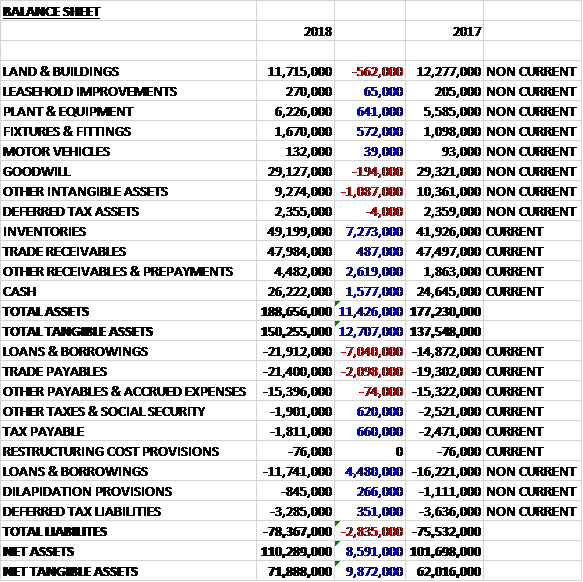

When compared to the end point of last year, total assets increased by £11.4M driven by a £7.3M growth in inventories, a £2.6M increase in prepayments and a £1.6M growth in cash, partially offset by a £1.1M decline in other intangible asserts. Total liabilities also increased during the year due to a £2.6M growth in borrowings and a £2.1M increase in trade payables. The end result was a net tangible asset level of £71.9M, a growth of £7.9M year on year.

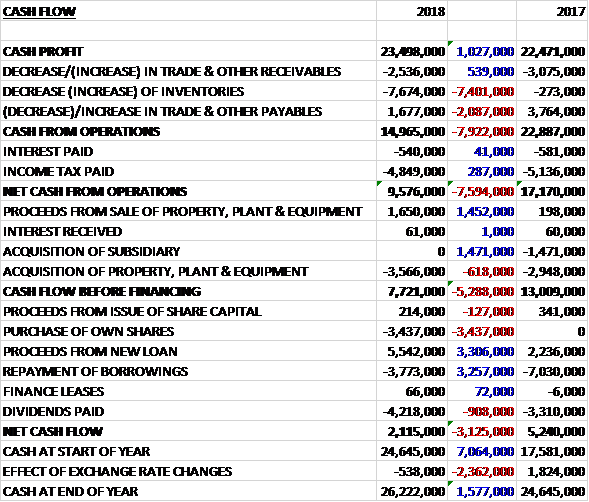

Before movements in working capital, cash profits increased by £1M to £23.5M. There was a cash outflow from working capital and despite tax payments reducing by £287K the net cash from operations was £9.6M, a decline of £7.6M year on year. The group made proceeds of £1.7M from the sale of assets but spent £3.6M on new property plant and equipment to give a free cash flow of £7.7M. Of this, £3.4M was spent purchasing shares, £4.2M on dividends but the group received a net £1.8M from new borrowings to give a cash flow of £2.1M and a cash level of £26.2M at the year-end.

The underlying profit in the UK business was £8.3M, a growth of £1.9M year on year despite the ongoing uncertainty surrounding Brexit. The biggest increase in revenue continues to be seen across the European distribution businesses, growing 23%. Outside of this, growth has largely come from increased sales to the core multinational OEMs across a number of sectors. In addition, there has been an operating margin increase reflecting the benefits of the revenue growth over a semi-fixed cost base.

The underlying profit in the European business was £9M, a decline of £712K when compared to last year. The business exited the year strongly, however, with revenues in H2 growing by 5.2% with full year revenues up 3.8% despite following abnormally high sales volumes in the Italian domestic appliances business last year as they supported a global product recall programme for a key customer. The most significant gains this year have arisen in the automotive sector in the Netherlands and Sweden, with these sites seeing revenue growth of 15.4% and 13.6% respectively.

The gross margin declined specifically within the Italian business where the impact of purchase cost increases in the second half of 2017 have continued into 2018. In addition to this there was a planned increase in fixed production costs as the group invested in manufacturing capacity to support future growth. Positive margin improvements in other parts of the European business have helped offset some of this decline.

The underlying profit in the US business was £52K, a decrease of £282K when compared to 2017, although revenues increased by 8%, driven predominantly by the automotive sector, as a strong second half offset a slow first half of the year due to Hurricane Harvey. Gross margins in the US have declined as a result of the product mix changes and an increased focus on the automotive sector, exaggerated by reduced sales volumes due to the hurricane as well as one-off set up costs relating to the start of production for one of the region’s biggest automotive customers. Low underlying operating margins continue to be expected in this region given the level of investment for future growth being made.

The underlying profit in the Asian business was £8.5M, an increase of £456K year on year. Trading has increased almost across the board with Shanghai showing the strongest revenue growth at nearly 10%. This is mostly in the automotive sector as the group expand into a number of their multinational OEM customers both locally and into Japan.

The group announced Project Atlas, a multi-year investment in their IT infrastructure and underlying business processes with a budgeted cost of up to £15M. So far they have incurred costs of £400K, largely relating to project team and consultancy costs. The project is about more than just an IT platform, with that element representing about a third of the overall cost. A significant proportion of the spend has been aligned to a review and redesign of their business processes which should drive improvements in their operating and commercial effectiveness. The board expects there to be material benefits of the investment programme. The estimated ROI is 25% per annum by 2023

During the year a factory previously rented to an automotive tier 1 company in Malaysia was sold for £1.7M, generating a profit of £600K.

In manufacturing, their capex plans will continue to increase capacity, most notably at both the Italian and Singapore sites. This will reduce the per part production costs by bringing more manufacturing in-house in the future. On the distribution side of the business, they have already expanded warehouse capacity in Shanghai and Northern Ireland to support the strong growth in those markets. In 2019 they will see further targeted expansions in some of their other high growth sites such as the Netherlands. Moving into their new sire in the US in April 2018 represents one of their biggest warehousing investments in recent years. This has increased capacity significantly, to not only better support existing trading levels but also to future-proof the business for further growth.

In Europe the group continue to invest in their expanding greenfield distribution site in Spain and the setup in November of a TR Innovation and Technical Centre in Gothenburg is already helping to develop their presence in this developing market.

In April the group acquired Precision Technology Supplies for an initial consideration of £8.5M and a further contingent consideration of up to £2.5M. Based in the UK, the business is a distributor of stainless steel industrial fastenings and precision turned parts, primarily to the electronics, medical instruments, petrochemical, defence and robotics sectors. Last year the business reported pre-tax profits of £700K and the acquisition generated goodwill of £2M so on the surface this seems like a decent price. The acquisition widens the group’s stock range, enhancing their customer offering and should provide support to the distributor sales.

Going forward, the current year has started well with a robust pipeline in place and the board remains confident of delivering on its expectations. Wider macroeconomic factors continue to exist that the group cannot fully mitigate, including the ongoing volatility in the forex and raw material markets, the expected wash through of input cost pressures in the UK due to the weakness of Sterling and the wider potential implication of Brexit.

After a 10% increase in the total dividend the shares are yielding 1.6% which increases to 1.7% on next year’s consensus forecast. At the current share price the shares are trading on a PE ratio of 19.3 which falls to 16.5 on next year’s forecast. At the year-end the group had a net debt position of £7.4M compared to £6.4M at the end of last year.

On the 14th June the group announced that Chairman Malcolm Diamond sold 250,000 shares at a value of £666K. No reason was given which is a little concerning.

Overall then this has been a good year for the group. Profits were up, net assets increased and although the operating cash flow was down, this was due to working capital movements and cash profits improved with a decent amount of free cash also being generated. The UK and Asian businesses did well, with particular growth in automotive but the European and US businesses both saw profits decline. In Europe this was put down to increased purchasing prices in Italy along with investment in future growth. Investment also affected the US, in addition to the effects of the hurricane in H1.

Project Atlas is a considerable use of future cash, with some £15M being invested but hopefully will aid the group in future but forex movements and raw material price hikes are risks going forward. The New Year seems to have started OK but the shares are not hugely cheap with a forward yield of 1.7% and PE ratio of 16.5. The director sale is also a concern, but overall I see nothing major here to force a sale.

On the 26th September the group released a trading update covering the year as a whole when trading was in line with management expectations. Demand remains reassuring across Asia and Europe and although relatively small, the US is growing well this year from a mix of increasing electronics and automotive sales. In the UK they have seen a solid performance across their major market with the exception being automotive where volumes are being hampered by diesel0led transitory reductions and changes to product cycles and model builds.

Globally automotive remains the strongest sector for organic growth as they continue to increase their market share and site penetration with their tier 1 and OEM customers. The increase in electric vehicle production is a significant growth opportunity for them providing additional access points as many more new platforms come on line, battery technology develops and the demand for charging stations accelerates.

The current solid revenue growth is not being reflected in operating margins, however, as they continue to invest for the future. Capital investments in Singapore, Italy and Taiwan are building their capacity and capabilities in these locations. The recent warehouse expansions in the US, Netherlands and Shanghai support the strong growth seen across those sites.

The PTS acquisition has settled well into the group and remains on target to be earnings enhancing in 2019.

In the UK they have seen the impact of input cost inflation in the period as a result of the weak pound but outside of this they believe that the operational and financial impact of any Brexit scenario will be manageable. They are also closely monitoring the escalating trade tensions between the US, Europe and China but they don’t expect the effects of this to be material for the group.

Overall the group remains on track to deliver results for 2019 in line with management expectations. This all looks fine, I am thinking of buying back in here.