Swallowfield has now released its final results for the year ended 2015.

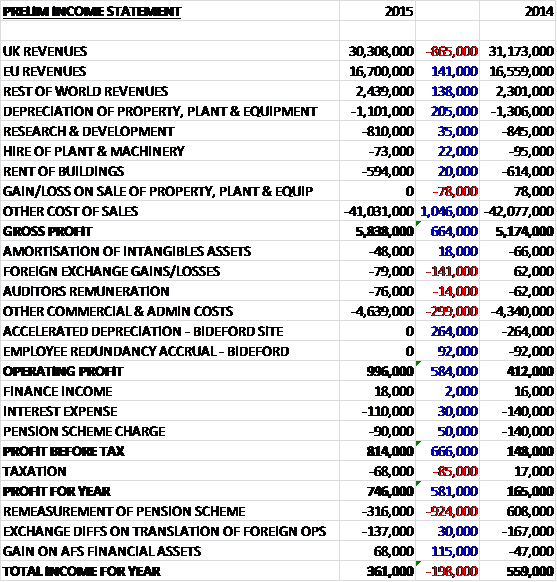

Revenues fell when compared to last year as a £141K growth in EU revenue and a £138K increase in ROW revenue was more than offset by an £865K decline in UK revenue. Although due to a weakening Euro and strengthening US dollar, revenues on a constant currency basis would have been £900K higher. Depreciation fell year on year, however, and other cost of sales declined by more than £1M to give a gross profit £664K above that of 2014. We then see a £141K negative swing in foreign exchange gains/loss and a near£300K fall in admin costs, although there was a lack of £366K in exceptional items that occurred last year so that the operating profit increased by £594K year on year. Finance costs fell by £78K but tax increased by £85K so that profit for the year came in at £746K, an increase of £589K year on year.

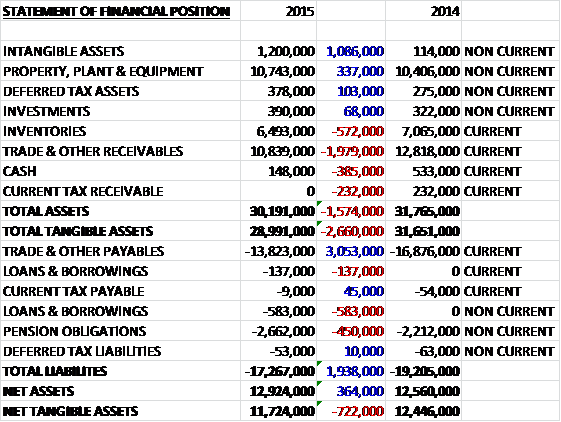

When compared to the end point of last year, total assets fell by £1.6M driven by a £2M decline in receivables, a £572K fall in inventories and a £385K decrease in cash partially offset by a £1.1M increase in intangible assets and a £337K growth in property, plant and equipment. Liabilities also fell when compared to last year as a £3.1M decline in payables was partially offset by a £720K increase in loans and a £450K growth in pension obligations. The end result is a net tangible asset level of £11.7M, a decline of £722K year on year.

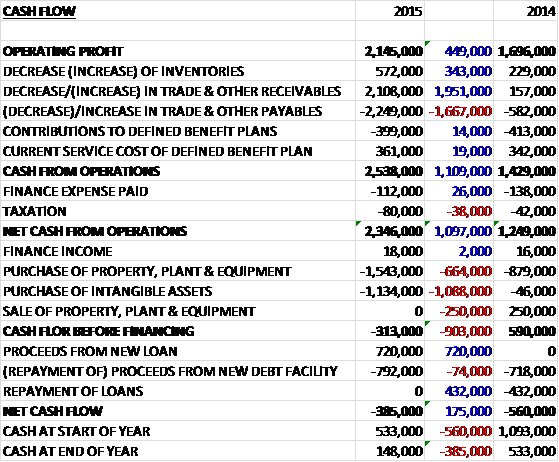

Before movements in working capital, cash profits increased by £449K to £2.1M. A decline in receivables was broadly offset by a fall in payables but a fall in inventories meant that the cash flow from operations grew by £1.1M which, after tax and interest, became £2.3M, an increase of £1.1M year on year. The group then spent £1.5M on property, plant and equipment, along with £1.1M on intangible assets – both much higher than last year due to the timing of a major aerosol capital project plus the investment in the cost base optimisation project at Bideford so that before financing there was a £313K cash outflow. After a small net repayment of loans, the cash outflow for the year stood at £385K to give a cash level of £148K.

During the year the group have secured important new contracts in their drive and build categories that will support further growth. They have also made their first shipments of their premium beauty brand Bagsy and the value brand Tru continued to build its retail presence. An increase in margins offset a slight softness in revenues against expectations due to the delayed availability of some materials and the continuing weakness of the Euro. The overall negative effect of the Euro weakness on profits was £400K during the year.

The group are focusing on the drive categories of personal care aerosols, lip balms, deodorant sticks and roll-ons. They grew direct contribution margin of 9% and have secured two significant contracts with major global brand owners that will contribute to further growth next year and beyond.

In the year they introduced their new plastic aerosol product in a post-foaming shower gel format. This project has taken three years to develop and included many innovations to overcome the challenges of pressurisation precision, crimping technology, gassing techniques, formulation compatibility and shrink-sleeving onto heat sensitive PET. It has enabled them to secure a long term contract with one of their largest customers and provides them with the opportunity to extend this technology to other product categories and customers.

The group have also utilised their product development expertise to create new ranges of products under their own brands as well as those of their customers. They are positioned to avoid any direct conflict with the existing customer base. Through targeted campaigns and the use of low cost customer engagement channels such as social media, it is believed that they can build strong brand awareness to support product sales with moderate and sustainable investment levels.

Following the acquisition of the Real Shaving Company brand, it has been integrated successfully and it is performing well. In addition to its financial contribution, the brand has also added further sales channels which the group will leverage for the other owned brands. Customer response to the plans for the brand has been positive and first listings for the new aerosol products have been agreed. The brand was acquired for £1.15M.

The development of the Swallowfield brands progressed during the year. The premium brand, Bagsy, was introduced in June exclusively online and will be launched with a major national department store chain in October. Distribution of the value brand Tru has been extended – it is now present in there UK retailers and one in Europe. The new male haircare brand, MR, will be launched in October into 350 stores of a leading high street health and beauty retailer. The group continues to work on a number of projects which may lead to the establishment of new capabilities but the success so far of the own brand products means that resources are being deployed in areas that accelerate progress there.

During the year the group completed the consolidation at the Bideford site into two buildings from three, relocating selected manufactured lines to Tabor in the Czech Rep. This project delivers full year savings of £230K. They have also identified a project to implement a coordinated upgrade of the energy and waste infrastructure at the main Wellington site, which aims to generate savings of about £150K per annum and is expected to be completed in 2016.

Although it still causes some issues, the pension scheme seems to be improving. The group entered into a revised deficit recovery plan with the payment falling from £111.5K per annum to £108K per annum over ten years. Subsequent to finalising the valuation the group entered into a formal consultation with members to close the scheme to future accrual from Jan 2016.

Going forward the board believes that they will deliver further profitability growth in the following year.

During the year the group have reduced their dependency on certain clients but they do still rely on a relatively small number of important clients with one customer accounting for 14% of revenues and another one accounting for 11%. At the current share price the shares trade on a rather expensive looking 18.9 but this falls to a much more reasonable 10.3 on next year’s consensus forecast. At the year-end the group had a net debt position of £5.4M compared to £5.1M at the end of last year which I would like to see come down a bit actually. After the restatement of the final dividend, the shares now yield 1.6% which increases to 2.4% on next year’s consensus forecast.

Overall then, this seems to be a tentatively positive year for the group. Although net tangible assets fell during the period, profits increased along with operating cash flows. The group is still not producing any free cash, however, which means that the dividend payments are not really that prudent in my view. There seems to be a lot of activity with new brands as the first shipment of the Bagsy brand took place along with the first listings of the acquired Real Shaving Company brand. The Bideford consolidation should enable savings of £230K per annum which is quite material for a company of this size but the Euro weakness remains a headwind. With a forward PE ratio of 10.3 and a dividend yield of 2.4% the shares do not look that expensive and although risks remain, I am happy to hold on to my shares here.

On the 12th November the group released an AGM statement covering the first four months of the year and overall trading is line with expectations. Production has started on two significant new contracts with major global brands as previously announced which will positively impact on the second half of the year. Similarly, production and sales of the new plastic aerosol product are performing as planned. The premium beauty brand, Bagsy, is now being rolled out across Debenhams stores nationwide in time for the Christmas trading period and the men’s haircare range, MR, is now present in larger Boots stores across the country. Whilst the board anticipate the challenging retail conditions in the UK and the rest of Europe to continue, they expect to maintain their positive momentum and are confident in the prospects for the year as a whole. This all seems fairly good to me.