AG Barr has now released their interim results for the year ending 2018.

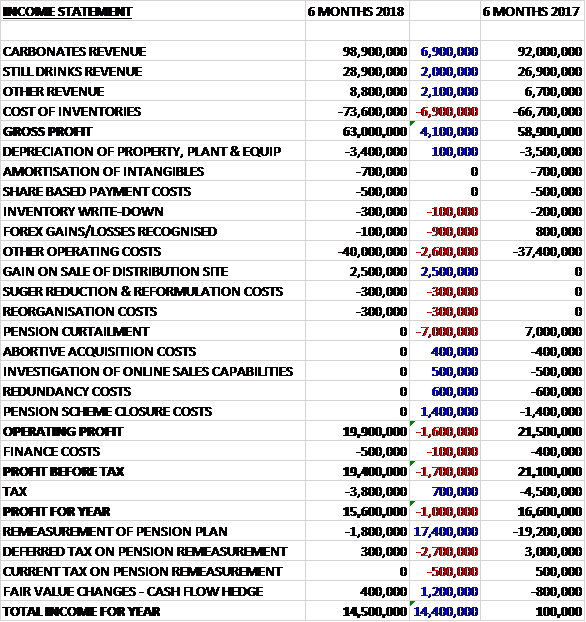

Revenues increased when compared to the first half of last year due to a £6.9M growth in carbonates revenue, a £2M increase in still drinks revenue and a £2.1M growth in other revenue. Cost of inventories also increased to give a gross profit £4.1M higher. There was a £900K negative swing to a forex loss and other operating costs grew by £2.5M. The group did make a £2.5M gain on the disposal of the distribution site, though and there were a number of one-off costs that didn’t recur this time. After the pension curtailment, which brought in £7M last time, the operating profit declined by £1.6M. Finance costs saw a modest rise but tax charges fell by £700K to give a profit for the period of £15.6M, a decline of £1M. If we remove distribution site sale this year, and the pension stuff last year, the profit comes in at £13.1M, a growth of £2.1M year on year.

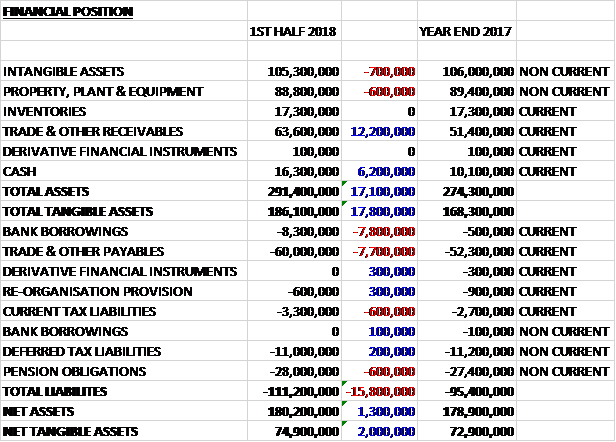

When compared to the end point of last year, total assets increased by £17.1M, driven by a £12.2M growth in receivables and a £6.2M increase in cash. Total liabilities also increased due to a £7.7M growth in bank borrowings and a £7.7M increase in payables. The end result was a net tangible asset level of £74.9M, a growth of £2M over the past six months.

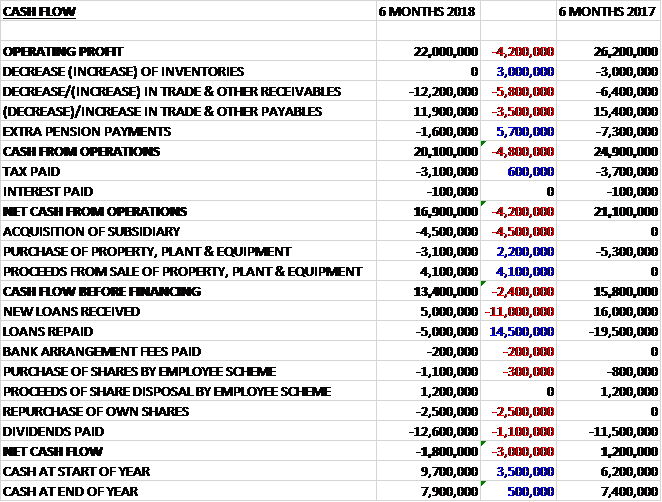

Before movements in working capital, cash profits declined by £4.2M to £22M. There was a modest cash outflow from working capital, and but tax payments reduced by £600K to give a net cash from operations of £16.9M, a decline of £4.2M year on year. The group spent £4.5M on acquisitions and £3.1M on capex but received £4.1M from the sale of the warehouse so the free cash flow was £13.4M. This just about covered the £12.6M of dividends but not quite the £2.5M of share buy backs so there was a cash outflow of £1.8M and a cash level of £7.9M at the period-end.

The underlying gross profit in the Carbonates division was £49.3M, a growth of £1.4M year on year. The underlying gross profit in the Still drinks division was £9.2M, an increase of £1.7M when compare to the first half of last year. The underlying gross profit in the other businesses was £4.5M, a growth of £1M when compared to the first half of 2017.

The group has maintained the strong sales momentum of the second half of last year during the period, growing revenue by 8.8% whilst the total soft drinks market grew by 4.2% in the same period. The increased brand investment along with the cost pressures relating to the continued weakness of Sterling, led to a moderate reduction in margins. The improved market reflected the impact of a seasonally better early summer weather and price inflation.

The group’s performance was particularly strong in England and Wales where they have gained new customers. The Funkin business continues to grow, benefiting from increased cocktail consumption, wider product distribution and further product innovation.

During the period, a £2.5M gain on sale was made on disposal of the Walthamstow distribution site, and the group has entered into a three year operating lease to continue to operate from there in the short term. To date, £300K of costs have been incurred as part of the ongoing sugar reduction and reformulation programme. These costs are forecast to significantly exceed the level of expenditure that would normally be incurred in the course of new product development. By the end of last year, the restructuring was largely complete but £300K of costs were incurred in the period, primarily being an increase in the redundancy provision and further recruitment costs.

During the period the group started a share repurchase programme of up to £30M which is expected to complete within two years. A total of 405,000 shares have been repurchased and cancelled at a cost of £2.5M.

Going forward, the soft drinks market has been negatively impacted in the short term by the poor weather since late July but assuming market conditions across the rest of the year are reasonable the group remains on course to meet the board’s expectations for the full year.

At the current share price the shares are trading on a PE ratio of 24.7 which falls to 20.9 on the full year consensus forecast. After a 5% increase in the interim dividend, the shares are yielding 2.3% which increases to 2.4% on the full year forecast. At the period-end the group had a net debt cash position of £7.9M comparted to £9.7M at the year-end.

Overall then this has been a rather decent period for the group. Profits were up, as was net assets. The operating cash flow did decline, however, but there was still a decent amount of free cash generated. The good performance has been boosted by the good early summer weather. Unfortunately this has not continued into the second half so things might now be a bit more difficult. These shares are not cheap at a forward PE of 20.9 and yield of 2.4% but the company is a good, cash generative business and I am a current holder.

On the 30th November the group announced that Commercial director Jonathan Kemp sold 3,900 shares at a value of £24K.

On the 1st February the group released a trading update covering the year. Total revenue is expected to be £277M, up 7.5% on the prior year. They have continued to outperform the total UK soft drinks market and increased their overall market share with latest data seeing the market value up 2.7%.

The group have not been immune to the external cost pressures faced by many UK businesses over the year, particularly in relation to the weakness of Sterling but the board remain confident of delivering profit growth in line with expectations. It is expected that 2018 will be another challenging year for UK business against a backdrop of continued uncertain economic conditions. In addition the soft drinks industry faces significant changes in regulation, customer dynamics and consumer preference.