Air Partner has now released their interim results for the year ending 2018.

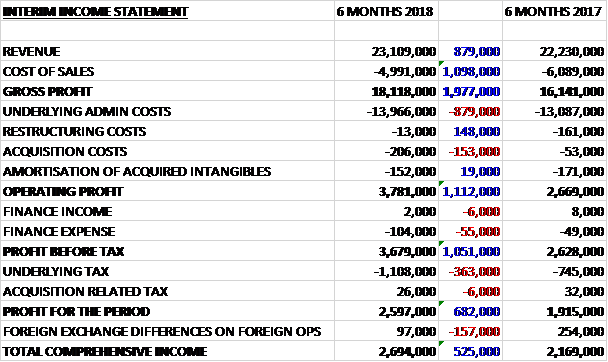

Revenues increased by £879K when compared to the first half of last year and after cost of sales decreased by £1.1M the gross profit grew by £2M. Underlying admin expenses were up £879K and acquisition costs increased by £153K but restructuring costs were down £148K and the operating profit was £1.1M higher. Finance expenses grew by £55K and the tax charges increased by £369K, all of which meant that the profit for the period was £2.6M, a growth of £682K year on year.

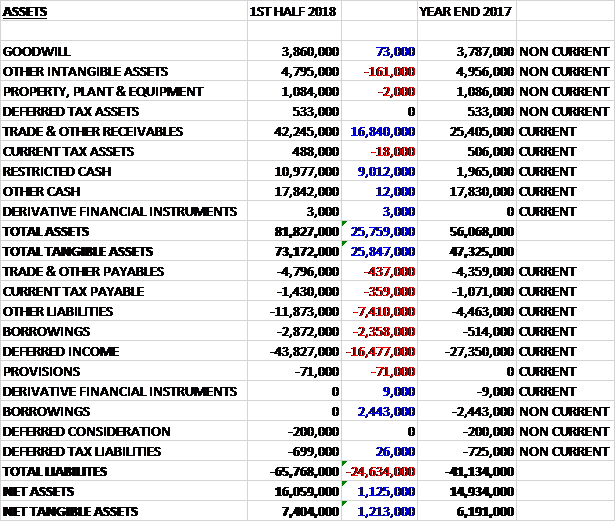

When compared to the end point of last year, total assets increased by £25.8M, driven by a £16.8M growth in receivables and a £9M increase in restricted cash. Total liabilities also increased during the period due to a £16.5M increase in deferred income and a £7.4M growth in “other” liabilities. The end result was a net tangible asset level of £7.4M, a growth of £1.2M over the past six months.

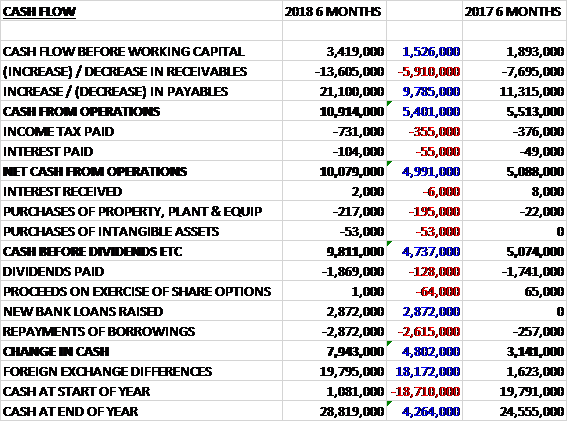

Before movements in working capital, cash profits increased by £1.5M to £3.4M. There was a large cash inflow from working capital due to an increase in payables relating to the larger tour operations programme and the timing of flights, and after tax payments were up £355K and interest charges increased by £55K the net cash from operations was £10.1M, a growth of £5M year on year. The group spent £217K on tangible fixed assets and £53K on intangible assets to give a free cash flow of £9.8M. This easily paid the £1.9M of dividends, and also would have done even without the working capital contribution. The cash flow for the period was £7.9M and the cash level at the period-end was £28.8M.

The underlying operating profit in the Commercial Jet Broking business was £2.7M, a growth of £840K year on year. This growth was driven by pleasing performances from all territories with good business from both new and existing customers. Across Europe they have benefitted from the European Tour Operating programmes and their expertise in serving sports teams with flights to the US, China, Singapore, South America and Europe arranged for football clubs during the pre-season tours. In the UK they have won a new contract with a premier league club, bringing the total number of football teams they work with to 35. They have also renewed their contract with a major German automotive company for a further three years. Finally, the UK and US teams have worked together to deliver a programme for a large global insurance company.

The underlying operating profit in the Private Jet Broking business was £1.4M, a decline of £88K when compared to the first half of last year, reflecting a lower spend over the period from some key clients and the continued investment in the sales teams. In the US, where they expanded the New York office last year and brought in new management to bring greater focus to the region, they have seen a sharp increase in corporate and high net worth individual business, with overall client numbers increasing by nearly 70% over the period. European private jets business remains small with slow growth.

The remarketing business has had a good start to the year having been rebranded under the Air Partner umbrella. Over the period, it sold and delivered two B737 aircraft and a GE engine for Kenya Airways; two 747s on behalf of China Airlines and won an exclusive contract with Saudia to market 15 B777 aircraft.

The underlying operating profit in the Freight Broking business was £577K, an increase of £271K when compared to a soft comparison in the first half of 2017. While the automotive sector remained strong, this growth arose from the international offices which benefited from contracts to the Middle East.

The underlying operating profit in the Consulting & Training business was £408K, broadly flat year on year. Over the first half, Baines Simmons has won new safety and training contracts with tier 1 national carriers and with the RAF of Oman. The pipeline for the second half remains encouraging. The business has won a four year contract with the European Defence Agency to provide consulting and training services to all EU member states and is also working with various airlines. They have also seen a strong performance in Academy Training.

At the end of last year, the group acquired fatigue management consultancy Clockwork Research. Trading has been challenging but with a good pipeline of projects and the board are confident in the longer term prospects for the business.

After the period-end, in September, the group acquired Safe Skys for a total consideration of £3M. The business is an environmental and air traffic control services provider to UK and international airports with a particular focus on wildlife hazard management and bird control.

Going forward, current trading is in line with expectations and the group enter the second half of the year with confidence that their expectations for the full year will be met.

At the current share price the shares are trading on a PE ratio of 26.3 which falls to 13.8 on the full year consensus forecast. After a 6% increase in the interim dividend, the shares are yielding 3.8% which increases to 3.9% on the full year forecast. Excluding the Jetcard cash, the group had a net cash position of £10.6m at the period-end compared to £1M at the year-end.

Overall then this has been a robust period of trading for the group. Profits increased, net assets grew and the operating cash flow improved with a decent amount of free cash being generated. The good performance seems to have been driven by the commercial jet broking business, buoyed by a busy European tour operating season and increased work for sports teams. Clockwork Research seems to be struggling so the jury is still out on the acquisition strategy but the underlying business is doing well and a forward PE of 13.8 and yield of 3.9% looks decent value to me. I continue to hold.

On the 3rd April the group announced that it had identified an issue relating to its accounting for receivables and deferred income. The issue principally relates to the collection of receivables from customers and accounting for uncollected amounts since 2011. Certain uncollected receivables were inappropriately offset against deferred income rather than being expensed.

The board believe the total cumulative impact arising between 2011 and 2018 will be around £4M. Aside from this issue, the group is trading within expectations. This is clearly disappointing but the underlying trading does not seem to have been affected so I am minded to hold on for now.