AG Barr have now released their interim results for the year ending 2019.

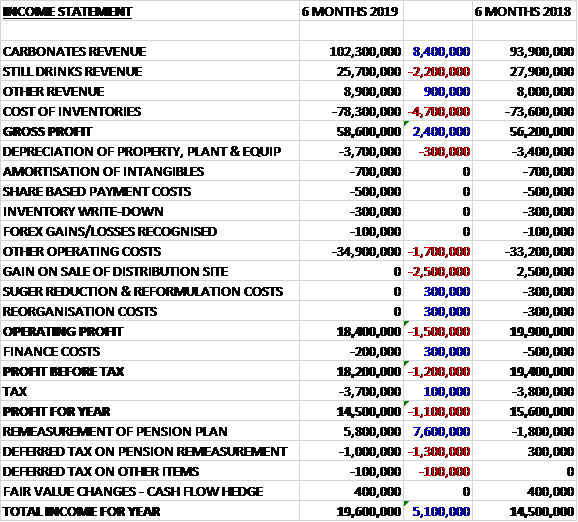

Revenues increased when compared to the first half of last year as a £2.2M decline in still drinks revenue was more than offset by an £8.4M increase in carbonates revenue and a £900K growth in other revenue. Cost of sales also increased to give a gross profit £2.4M higher. Operating costs increased by £2M and there was no sale of buildings, which brought in £2.5M last time. There was also no reformulation costs or reorganisation costs, which were both £300K last time which meant the operating profit declined by £1.5M. Finance costs were down £300K and tax charges fell by £100K to give a profit for the period of £14.5M, a decline of £1.1M year on year.

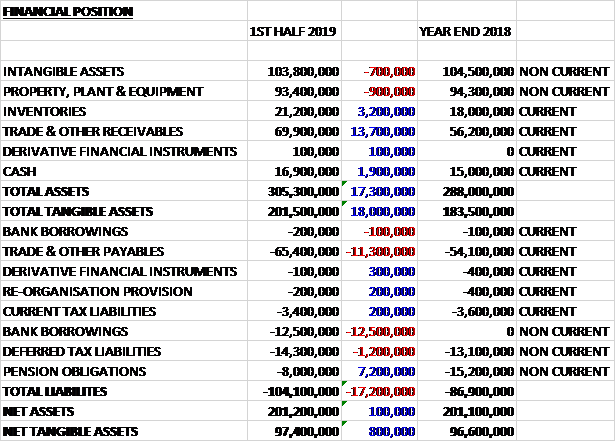

When compared to the end point of last year, total assets increased by £17.3M driven by a £13.7M growth in receivables, a £3.2M increase in inventories and a £1.9M growth in cash. Total liabilities also increased during the period as a £7.2M decline in pension obligations was more than offset by a £12.6M increase in bank borrowings and an £11.3M increase in payables. The end result was a net tangible asset level of £97.4M, a growth of £800K over the past six months.

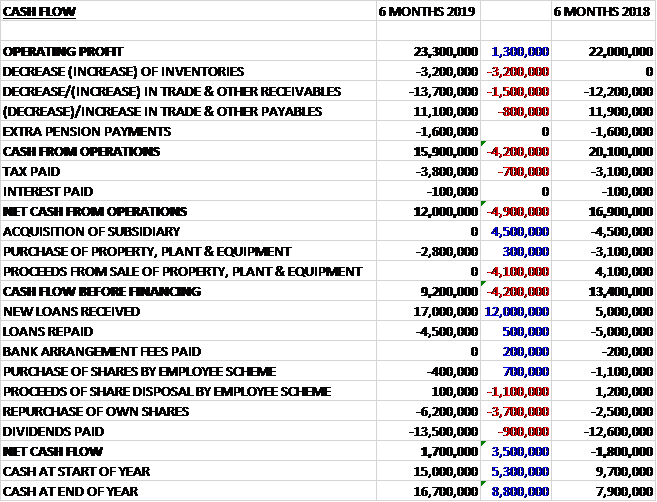

Before movements in working capital, cash profits increased by £1.3M to £23.3M. There was a cash outflow from working capital and tax payments increased by £700K to give a net cash from operations of £12M, a decline of £4.9M year on year. The group spent £2.8M on capex to give a free cash flow of £9.2M. This did not cover the £13.5M paid out in dividends or the £6.2M spent on share repurchases so the group took out a net £12.5M. This gave a cash flow of £1.7 for the period and a cash level of £16.7M at the period-end.

The gross profit in the carbonates business was £47M, a growth of £2.7M year on year. The gross profit in the still drinks business was £7.4M, a decline of £800K when compared to the first half of last year.

The gross profit in the other business was £4.2M, a growth of £500K year on year. The Funkin business continues to grow in its traditional areas and now also in new formats and new market segments. They have seen the take-home packs, initially launched last year, begin to gain sales traction in the grocery channel while the development of the Funkin draft cocktail proposition is rolling out into the on-trade and has already enjoyed success at outdoor events during the festival season.

Retail pricing increased across the market following the implementation of the Soft Drinks Levy in April. The total market grew by 7.7% in value terms and 3.8% in volume. The soft drinks market experienced the effect of weather extremes, from the significant snowfall in Q1 to the hot summer weather. The unusual demand pattern which arose was further compounded by the shortage of CO2 in the early summer which affected soft drinks supply for a number of weeks.

The group delivered strong volume market share gains, up 15% with a pleasing performance from IRN-BRU, particularly in England and Wales. Following the execution of the reformulation programme they have continued to invest in their core bands with particular emphasis on IRN-BRU, Rubicon and Strathmore. The period also saw the group initiate their trading partnerships with Bundaberg and San Benedetto, both of which have made a positive start and are already adding value.

The current trading strategy is delivering volume benefits which they aim to maintain for the rest of the year as they navigate their way through the changing market. As expected, the operating margin was 13.4% reflecting the volume focus and investments made.

There will shortly be a new accounting standard covering operating leases. Had it been implemented during the period, the effect would be to increase the net book value of property, plant and equipment by £6.9M with a corresponding finance lease liability of £8.2M. The net impact on retained earnings would be a charge of £1M. To date, £9.7M of operating lease rentals have been recognised in respect of the assessed leases. Based on management’s ongoing exercise on leases identified to date, under these standards, £8.6M of depreciation would have been charged plus a further £2.1M of interest charges.

Going forward the group plan to invest further across the second half of the year which they expect will have a moderate impact on margins but they remain on target to meet their profit expectations for the full year.

At the current share price the shares are trading on a PE ratio of 25.1 which falls to 23.4 on the full year consensus forecast. After a 5% increase in the interim dividend the shares are yielding 2.1% which is forecast to remain the same for the full year. At the period-end the group had a net cash position of £4.2M compared to £7.9M at the same point of last year.

On the 25th January the group released a trading update covering the year. Revenue is expected to be 5% up on last year at £277M. They gained further market share in the UK which saw volumes up 3% and value up 8%. The impact of the soft drinks levy has been evident across the market with value growth significantly outstripping volume and having taken the opportunity to drive volume growth during the period the group are now expecting to return to a more value led trading strategy.

They have invested across brands, assets and people which has supported growth but had a moderate impact on margins. They remain confident overall of delivering profit in line with board expectations, however. Going forward, further regulatory intervention is on the horizon but the board are confident of profitable growth next year.

Overall then this has been a fairly steady period for the group. Profits declined due to no freehold sales during the period, underlying profits were up; net assets increased but the operating cash flow deteriorated with free cash not covering dividends. This was not helped by adverse working capital movements, however, and cash profits increased. The Carbonates and Funkin businesses did well but the still drinks business saw profits decline, it is not clear why this was. This is a good company but the recent performance has been a bit lacklustre in my opinion and the shares are looking a bit expensive with a forward PE of 23.4 and yield of 2.1%. I’m tempted to take profits.