Asian Citrus has now released its full year results for 2014.

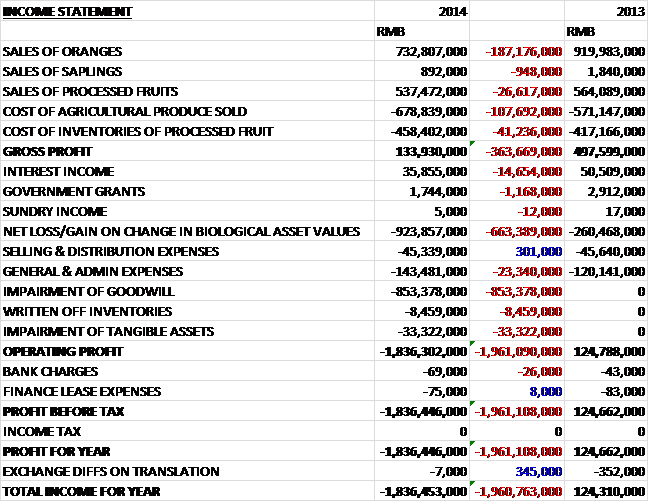

When compared to last year revenues were lower across all products with oranges down £18.7M due both to lower yields and reduced sales prices, and processed fruits some £2.7M lower. Cost of sales were up with the cost of agricultural produce up by £10.8M, mainly due to depreciation and increased use of fertilizer and pesticides, and the cost of processed fruit inventories were up £4.1M to give a gross profit down by an eye watering £36.4M. Interest income was down £1.5M and general/admin expenses were £2.3M higher due in part to the loss on the disposal of plant and machinery along with written off inventories. The big movements, however, were the non-cash charges. The net loss on biological assets was some £66.6M higher and there was an £85.3M impairment of goodwill due to current business conditions at Beihai BPG. This meant that the loss for the year was a massive £184M, a £1961M reversal on last year.

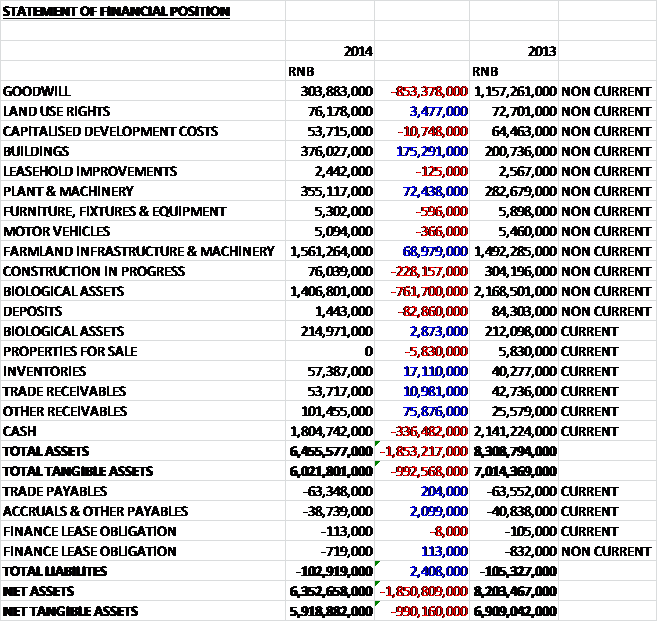

Overall total assets fell by £185.3M when compared to last year. This was driven by an £85.3M fall in Goodwill, a £76.2M reduction in the value of biological assets, a £33.6M fall in cash levels and a £22.8M reduction in the value of construction in progress, some of which was transferred to the Buildings asset. Liabilities were down by just £241K due to a £210K fall in accruals and other payables. Overall, net tangible assets were some £99M lower at £592M.

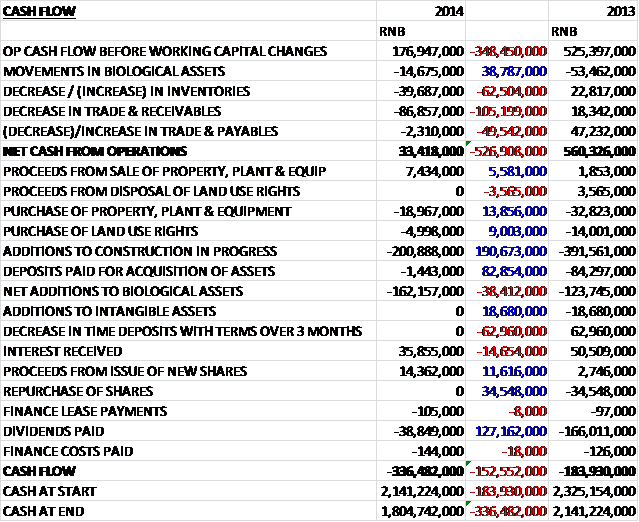

Before movements in working capital the cash generated from operations fell by £34.8M to £17.7M. An increase in inventories and decrease in receivables meant that net cash from operations deteriorated further by £52.7M to £3.3M. The group reigned back its cash spending in many areas but despite nearly halving still spent £20.1M on new constructions. The next largest spend was the £16.2M paid for biological assets which is clearly more cash than the group is getting from operations so cash flow this year was an outflow of £33.6M, some £15.2M less than in 2013 to leave a still fairly comfortable £180.5M in the bank at the year end.

The loss recorded for the fruits themselves was £96M compared to a £3.2M profit last year. The production yield at the Hepu plantation declined by nearly 18% due to the replanting programme to replace the existing winter orange trees, the continued impact of the citrus canker outbreak and the impact of frosts in the first part of the year. This was combined with a 3% decrease in the average selling price and increased costs due to the inclement weather to reduce growth margins at the plantation from 43% last year to 13% this year.

At the Xinfeng plantation the production yield decreased by 4% and the gross profit margin collapsed from 33% to 3% due to reduced sales, the persistent heavy rainfall and the dyed oranges being sold by other suppliers in the area which negatively impacted sales prices.

Processed fruit profits were just £1.3M, down from £13.9M in 2013 as revenues of juice concentrates declined due to a decrease in sales of juice concentrates, a fall in fruit juice trading and a decline in the selling price of these products due to the competitive market. The new plant in Baise City, Guangxi completed a successful trial production but it takes three years for the plant to run at full capacity.

The group are looking at methods to reduce the cost of pesticides and fertilisers, exploring new export opportunities and changing the product mix in order to improve margins. They have also been collaborating with scientists to provide advice on production and product improvements and to attempt to find ways to recover from the citrus canker outbreak, which is still causing issues for the Asian Citrus

After the reporting date Typhoon Rammasun caused widespread damage to the group’s assets which has caused inventories to be written off by £846K, impairment of property plant and equipment to the tune of £1.6M and further impairment of biological assets of £1.2M. The typhoon destroyed all banana trees planted in 2013, damaged some infrastructure and caused a significant volume of premature fruit drop from the orange trees in the Hepu plantation. Also, it caused a temporary suspension in activities at two of the fruit processing plants. After the damage had been cleared, 220,000 banana trees were re-planted with an expected harvest by the end of 2015, although it will take several years for the Hepu plantation and harvests to fully recover. The weather problems didn’t end with the typhoon as production at the Hunan plantation was delayed due to the impact of frosts but is scheduled to begin in 2016 with oranges initially, and grapefruits to follow.

There have been a number of changes in the board make up over the year. Mr. Tong Wang Chow, Peregrine Moncreiffe and Mr. Ma Chiu Cheung have all stepped down to be replaced by Mr. Ng Hoi Yue, Mr. Tonh Hung Wai, Mr. Chung Koon Yan, Mr. Ho Wai Leung and Mr. Ng Cheuk Lun. Importantly, the positions of chairman and CEO are now held by two different people, as opposed to just the one last year and now Mr. Ng Ong Nee is CEO. Hopefully the new CEO will attend the AGM unlike the outgoing director who was apparently too busy.

Due to the poor performance this year, there has not been a dividend announced. There seems to be a plethora of problems happening to the company at the moment. Heavy rains have leached nutrients from the soil, caused the outbreak of citrus canker that has not yet been eradicated; frosts have delayed the start of the new plantation and the typhoon has destroyed all the banana trees. This makes me wonder whether planting banana trees in typhoon affected areas is really a good ideal. Also, prices have been lower for both bananas and juices and the value of biological assets continues to fall. The cash buffer is still fairly decent but the operating cash flow at the moment doesn’t even cover the cost of biological assets. I still see potential here but things seem to be against Asian Citrus at the moment so I am holding off.

On the 7th November the group announced the results of negotiations over the winter orange contracts for the upcoming crop. So, is it good news? Well, it’s ACHL so of course it’s now. The good news first – the average selling price at the more important (for winter oranges) Xinfeng plantation increased by 2.6% when compared to last year but the quantity supplied at 113,600 tonnes, represents a fall of 7.8%. This is being blamed on “cryogenic freezing rain”. Wow, that sounds pretty nasty… Also, frosts have apparently affected the Orange blossom. At the much maligned Hepu plantation, the selling price has collapsed by 40% as canker ravaged oranges don’t look too good apparently. The price is almost inconsequential though because the group only managed to sell just over 7,000 tonnes after Typhoon Rammasun took its toll, representing a 71% decline. Clearly as a result of the above there will be a reduction in revenue and profit generated for the year ending 2015. I keep waiting for a point where these shares become investable and the inherent value tied up in the group is released but I continue to wait after this update.

On the 30th January the group released an updated trading statement. As already mentioned, the turnover and profits will be lower than the corresponding six month period last year. The winder orange crop at Hepu managed just 7,146 tonnes, which was in line with the previous indication. Hurricane Rammasun caused widespread crop loss resulting in a 71% decrease on volumes achieved last year. The winter crop at Xinfeng was 103,847 tonnes, below the previous guidance of 113,600. The crop here was affected by the cryogenic freezing rain damaging the fruit blossoms and the high temperature and drought from September to December. In total, production of winter oranges decreased by 25% to 110,993 tonnes. In addition to this, the average selling price also fell, down by nearly 3% on last year. The cause of the reduction is blamed on Typhoon Rammasun and the previously unmentioned Typhoon Seagull along with the poor appearance of the fruits following the Canker outbreak. Profitability was also impacted by a higher volume of fertilizers and pesticides following the typhoons and the canker – these costs are likely to continue in the short term.

As far as the processed fruits were concerned, unfortunately they did not provide much joy either. Production was down some 17% to 23,952 tonnes and there was additional margin pressure. No reasons were given for these particular declines. So, we have the following.

- Typhoon Rammasun

- Typhoon Seagull

- Cryogenic freezing rain

- High temperatures and drought

- Citrus Canker

- High costs and lower realised prices

- Processed fruit volumes declining

- Reducing margins on processed fruit.

This is all very terrible bad luck and I don’t see any hint of a light at the end of the tunnel. I have decided to stop updating on this company but may take another look if some of these issues can be overcome.

On the 3rd February the group announced that Huge Market Investments had sold 17,400,000 shares in the company. After the transaction they hold 54,426,722 shares or the equivalent of 4.36% of the total share capital. They must have taken quite a loss on this sale so this is not a vote of confidence.