Air Partner has now released its interim results for the year ending 2017.

Revenues were broadly flat when compared to the first half of last year but cost of sales declined by £4M which gave a gross profit nearly £4.1M above that of last time. Underlying admin costs increased by £3.3M but an increase in restructuring costs and the amortisation of acquired intangibles was mostly offset by a decline in acquisition costs so the operating profit was £770K up. Finance costs increased by £41K and tax charges grew by £269K so the profit for the period came in at £1.9M, a growth of £465K year on year.

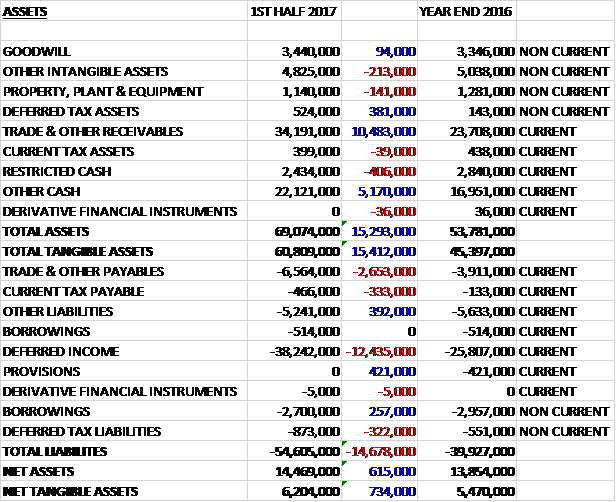

When compared to the end point of last year, total assets increased by £15.3M to £69.1M, driven by a £10.5M growth in receivables and a £5.2M increase in non-restricted cash, partially offset by a £406K decline in restricted cash. Total liabilities also increased during the period due to a £12.4M growth in deferred income and a £2.7M increase in payables. The end result is a net tangible asset level of £6.2M, a growth of £734K over the past six months.

Before movements in working capital, cash profits declined by £640K to £1.9M. There was a cash inflow from working capital compared to an outflow last year with the increase in receivables reducing considerably. After tax payments increased by £118K and interest was up £41K, the net cash from operations came in at £5.1M, an improvement of £6.3M year on year. The group only spent £22k on capex which left them with free cash of £5.1M, easily enough to cover the £1.7M paid out in dividends and a £257K loan repayment so the cash flow for the period was £3.1M and the cash level at the period-end was £24.6M.

The profit in the Commercial Jet Broking business was £1.9M, a growth of £271K year on year with the increase driven by strong trading in the UK and Europe, albeit with some continuing challenges in the US. Within the UK Commercial Jet team, they increased their focus on developing a clearer sales strategy, invested in key talent, particularly in the sports sector, and focused on improving the service levels they provide to their customer base. Success stories for the UK include a strong contribution from the sports sector, with flights conducted for a number of Premier League football teams, continued success from their oil and gas clients, along with continued government work.

In Europe, growth has been driven through an increase in their tour operations programme, the sports sector, with flights for Euro 2016, football clubs and major cycling events; and continued successes in the automotive industry. Although H1 performance in the US was below board expectations, prospects for H2 look promising as a result of government and election related contracts.

Cabot Aviation has had an encouraging start to the year, primarily through the successful remarketing of two Kenya Airways B777-2000ERs to Omni International. They continue to hold the mandate to remarket a further two B777-200Ers and two 737-700s on behalf of Kenya Airways together with a B787 for a cruise operator and two B747-400s for China Airlines.

The profit in the Private Jet Broking business was £1.5M, an increase of £525K when compared to the first half of last year, largely driven by a very strong performance in the UK, a solid performance in Europe, with the US showing signs of improvement after a disappointing performance last year. JetCard cash deposits stood at £16.1M at the period-end, an increase of £2.5M and the number of JetCards increased by 9 to 218 with utilisation increasing by 25% in the period.

The profit in the Freight Broking business was £306K, a decline of £88K when compared to the first half of 2016 as a strong performance in automotive in Europe was not enough to compensate for the lack of any government aid agency work during the period.

The Baines Simmons business provided a maiden profit of £1K during the period after it was acquired in August 2015. There have been a number of contract wins during the period, including the renewal of the Isle of Man aircraft registry for a further ten years and the provision of in-house training at BAE Systems, focusing on the Typhoon aircraft.

Richard Jackson joined the board in September having spent eleven years at the Civil Aviation Authority as group director of consumer protection. Amanda Wills was appointed to the board in April, she is a former CEO of Virgin Holidays. Shaun Smith, group finance director of Norcros also joined the board in May.

Given the strong first half performance and current trading the board remains confident that its expectations for the remainder of the financial year will be achieved. So far the group has not noted any adverse impact on trade as a result of the Brexit vote but JetCard and Cabot Aviation revenues within the UK are denominated primarily in Euros and US dollars respectively, which provides an upside as a result of the weakening of Sterling. Where possible, however, the group uses natural hedging to minimise its forex exposure.

At the current share price the shares are trading on a PE ratio of 21.1 which reduces to 10.3 on the full year consensus forecast. After a 10% increase in the interim dividend, the shares are yielding 5.2% which is expected to remain the same for the full year. At the period-end, excluding the jetcard cash, the net cash position was £5.2M compared to £1.4M at the same point of last year.

On the 13th December the group announced the acquisition of Clockwork Research, a fatigue risk management consultancy. The acquisition is being funded from existing cash resources and is expected to be earnings enhancing in the first year of ownership (last year the business made revenues of £700K). The business delivers fatigue risk management solutions for clients across various sectors of the aviation industry, including commercial air transport, business jets, cargo operations, air medical and search and rescue services as well as regulation authorities. In addition to projects in the aviation sector, over the last eleven years it has expanded activities into other safety-critical operating environments such as oil and gas and mining.

There is no mention of how much the consideration is but this seems like a small acquisition.

On the 2nd February the group released a trading update for the year as a whole. Trading in the second half of the year remained in line with expectations and the integration of Clockwork Research is progressing well. It was also announced that Chairman Richard Everitt is standing down at the AGM having been at the group for seventeen years – he has been appointed as Chairman of the Dover Harbour Board last year.

Not too much to go on here but it all looks fine.

On the 28th June the group announced that trading in the new financial year had started in line with their expectations and they remain optimistic for the rest of the year. It was also announced that Richard Everitt was standing down as Chairman to be replaced by current senior independent director Peter Saunders.

On the 25th July the group announced that the remarketing division had been appointed by Saudi Arabian airlines as its exclusive remarketing agent in respect of 15 Boeing 777-200ER aircraft.

On the 25th August the group released a trading update covering the first half of the year. They have made a strong start to the year with underlying pre-tax profit at least £4M compared to £3M in the first half of 2016. They also retain a strong net cash position. The broking division has performed well across all product lines while the consulting and training division is delivering solid results with an encouraging pipeline of opportunities to be secured in H2. Overall the board remains comfortable with their expectations for the full year.