Somero has now released its interim results for the year ending 2016.

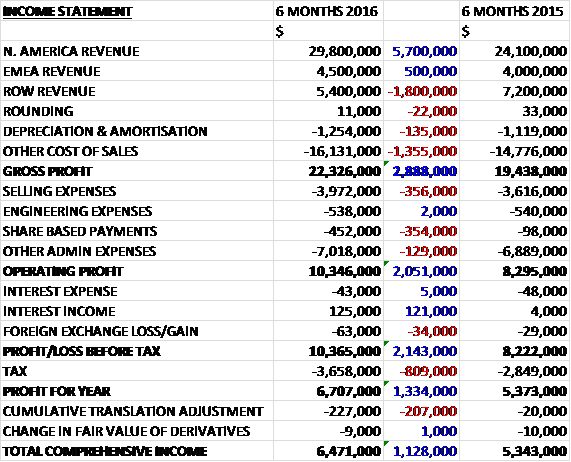

Revenues increased when compared to the first half of last year as a $1.8M decline in ROW revenue was more than offset by a $5.7M growth in North American revenue and a $500K increase in EMEA revenue. Depreciation and amortisation increased by $135K and other cost of sales was up $1.4M to give a gross profit $2.9M above that of last time. Selling expenses grew by $356K mainly due to increased personnel and marketing costs, share based payments were up $354K and other admin expenses increased by $129K which meant that the operating profit increased by $2.1M. We then see a $121K increase in interest income but also an $809K increase in tax charges to give a profit for the period of $6.7M, a growth of $1.3M year on year.

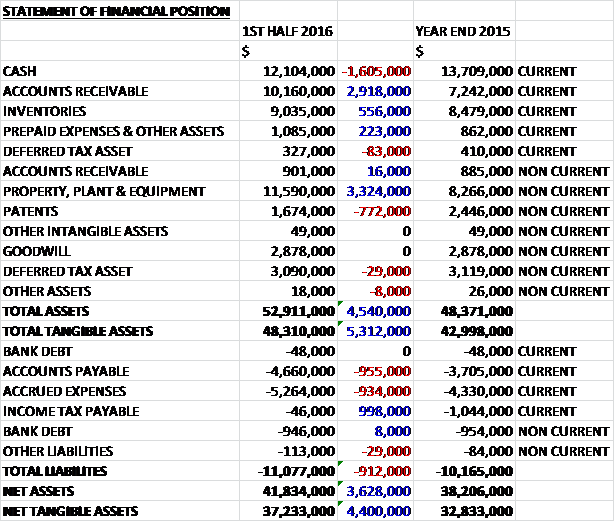

When compared to the end point of last year, total assets increased by $4.5M driven by a $3.3M growth in property, plant & equipment and a $2.9M increase in accounts receivable, partially offset by a $1.6M decline in cash. Total liabilities also increased during the period as a $998K decline in income tax payable was more than offset by a $955K growth in accounts payable and a $934K increase in accrued expenses. The end result was a net tangible asset level of $37.2M, a growth of $4.4M over the past six months.

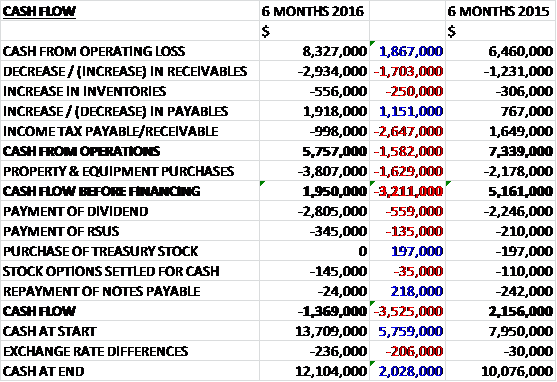

Before movements in working capital, cash profits increased by $1.9M to $8.3M. There was a cash outflow from working capital with a particularly large increase in receivables related to a high volume of North American sales occurring in June, and along with a $2.6M growth in tax payments which included final payment of amounts due for last year as well as an increased level of estimated tax this year, this meant that the cash from operations came in at $5.8M, a decline of $1.6M year on year. The group spent $3.8M on capex, partly related to the global HQ construction project to give a free cash flow of $2M which did not quite cover the $2.8M spent on dividends to give a cash outflow of $1.4M for the period and a cash level of $12.1M at the period-end.

On a product basis, the strong performance was driven by robust demand for recently launched new products and growth in other revenues due to sales in parts and services and the STS-11m Spreader.

Performance in the North American market remained strong supported by a healthy non-residential construction environment. The 24% revenue growth was in part driven by demand for new products. Sales in Europe grew by 37%, continuing a solid recovery trend and market conditions in China improved in the period as sales grew by 15%, driven by the positive impact of the long-term financing programme for customers that required installation of their machine shut-off payment protection tool. Their experience with this programme has been positive to date and in the period about 35% of sales in the country were financed under the programme.

Sales in Australia increased by 38% while India, Scandinavia and Russia reported sales that were modestly ahead of last year, or flat. In Latin America, South East Asia, Korea and the Middle East, sales were below previous year levels but the board expects improvements over the rest of the year.

Large line sales decreased to $12.4M primarily as a result of a decrease in volume to 34 units. Mid line sales increased to $5.6M due to an increase in volume to 30 units and small line sales increased to $7.7M due to an increase in volume to 89 units. Remanufactured sales decreased to $2.9M despite unit volume remaining flat at 23 units due to a change in mix, and 3D profiler system sales increased to $3M due to an increase in units sold to 30.

In the second half the group will launch the S-158C, an entry level small line machine designed for the Chinese and Indian markets, primarily focused on the productivity improvement value proposition. This machine is designed to benefit contractors with smaller sized slab projects and targets customers who are not ready to move to a higher level small line or boom-out laser screed machine. The product will have a small footprint, be affordable, easy to use and expand the number of customers using the group’s branded equipment.

In April the group completed construction and officially opened the new global HQ and training facilities in Florida. The final project cost was $4.8M, of which $3.3M was included in the capex for this half. Due to increased demand for training and education on concrete floor wide-placement and finishing best practices, the group are accelerating plans to design and construct a training environment to be located at the Fort Myers facility. It is expected that this project will be completed in Q1 2017 at a total project cost of $700K.

Positive trading momentum in North America has continued into the second half of the year reflecting a healthy non-residential construction market in the US. The ongoing construction growth and project backlogs customers are experiencing point to continued solid performance in the market for the rest of the year. After significantly strong trading in June to finish H1, the solid activity levels have carried over to July and August as the board continue to see significant opportunities across their markets. The board expects another successful year of growth in line with current market expectations.

At the current share price the shares are trading on a PE ratio of 14.3 which falls to 12.5 on the full year consensus forecast. After a 32% increase in the interim dividend, the shares are yielding 2.8% which falls to 2.7% on the full year forecast which doesn’t sound right to me. At the period-end, there was a net cash position of $11.1M compared to $12.6M at the end of the prior year relating to increased capex mainly.

Overall then this has been another decent period for the group. Profit was up, net assets increased and although the operating cash flow reduced with not quite enough free cash to cover dividends, this was due to historical tax payments and cash profits grew year on year. This good performance was driven by strength in North America, Europe, China and Australia with the rest of the world a little more difficult.

The big capital expenditure on the HQ has now been completed and the group still has a strong net cash position. The dividend yield of 2.7% is decent enough in this climate and the forward PE of 12.5 doesn’t look too taxing. At some point the cyclical nature of this share will come into play but at the moment this is a strong hold for me.

On the 10th January the group released a trading update covering 2016. In the second half of the year they continued to deliver profitable growth and cash generation. Due to a strong finish to 2016 combined with continued margin improvement, the board expect to report revenue slightly ahead of current market expectations and to report EBITDA comfortably ahead for the full year. In addition, given the strong cash generation, they expect to report net cash that is significantly ahead of market expectations.

Demand in the second half of the year remained robust across their core product range with particularly strong interest in recently launched new products, the large line S-10A and small line S-940 laser screed machines. Also contributing significantly to growth during the period were sales of large line S-15 laser screed machines, STS-11M spreaders, 3D profiler systems and parts driven by the high usage of their installed base of equipment by customers.

Geographically, second half performance in the core markets was solid with Europe contributing significantly to growth, North America contributing satisfactorily to growth and trading in China remaining healthy. Trading in Latin America and the Middle East improved considerably in the second half with Australia also contributing solidly to growth. In South East Asia, India, Scandinavia, Korea and Russia, however, trading levels were in line or down on the period year.

The board is confident in their ability to deliver another year of profitable growth in 2017, based on healthy market conditions in their core markets and encouraging growth opportunities in their other territories. Their confidence is further supported by encouraging pro-growth corporate tax reform and fiscal policy proposals in the US. They have also approved an increase to the dividend payout ratio from 30% to 40% of adjusted net income.

In addition, the strong cash generation of the business has built up cash reserves in excess of the targeted net cash level of $10M. They plan to review their cash position alongside cash requirements for current business needs and future investment during the first half of 2017. They will then assess the level of excess cash that may be subject to distribution back to shareholders through a special dividend later in 2017.

What a fantastic update! I remain a strong holder here and may even look to pick up more.