Alumasc have now released their interim results for the year ending 2018.

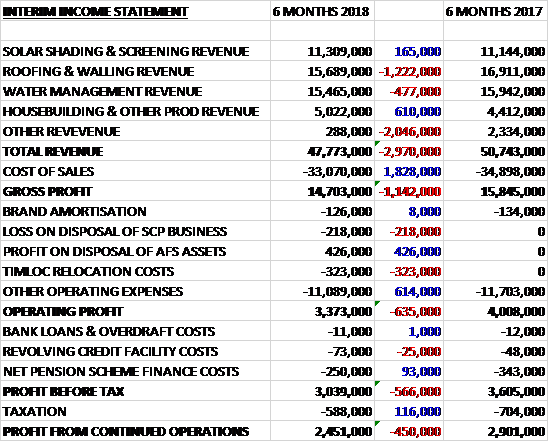

Revenues declined when compared to the first half of last year as a £610K growth in housebuilding revenue and a £165K increase in solar shading revenue was more than offset by a £1.2M decline in roofing and walling revenue, a £477K fall in water management revenue and a £2M decrease in other revenue. Cost of sales also declined to give a gross profit £1.1m lower. There was a £218K loss on disposal of the SCP business and £323K of relocation costs but there was a £426K profit on the disposal of the AFS assets and a £614K decrease in other operating costs to give an operating profit £635K lower. There was a £93K decrease in pension finance costs and a £116K fall in tax which meant that the profit for the period was £2.5M, a decline of £450K year on year.

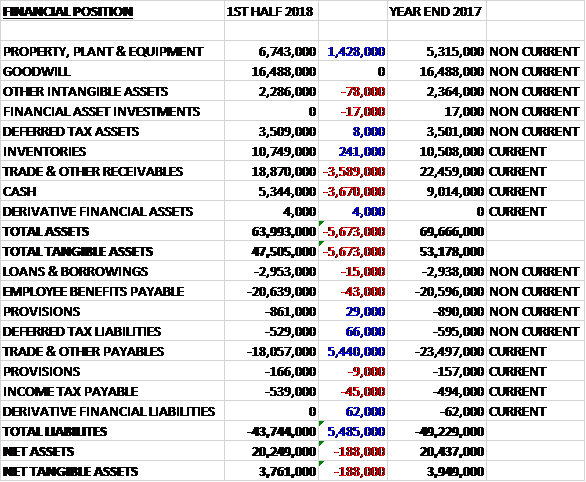

When compared to the end point of last year, total assets declined by £5.7M, driven by a £3.7M fall in cash and a £3.6M decline in receivables, partially offset by a £1.4M growth in property, plant and equipment and a £241K increase in inventories. Total liabilities also declined during the period due to a £5.4M decrease in payables. The end result was a net tangible asset level of £3.8M, a decline of £188K over the past six months.

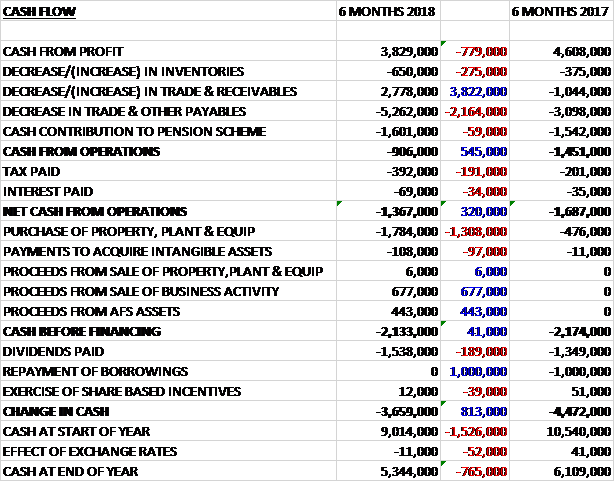

Before movements in working capital, cash profits declined by £779K to £3.8M. There was a cash outflow from working capital but this was less than last time and after tax payments increased by £191K and interest payments grew by £34K the net cash outflow from operations was £1.4M, an improvement of £320K year on year. The group also spent £1.8M on tangible assets, including £1M on the new Timloc factory, and £108K on intangibles put brought in £677K from the sale of a business and £449K from the sale of assets to give a cash outflow of £2.1M before financing. They then spent £1.5M on dividends to give a cash outflow of £3.7M and a cash level of £5.3M at the period-end.

The profit in the Solar Shading and Architectural Screening business was £731K, a growth of £100K year on year. After a slow start to the year, Levolux’s trading momentum grew strongly in Q2, resulting in a period where profits were ahead of last year. The business is benefiting from recent investments in UK and international sales resources, project and operations management capability and IT to grow revenues and margins. The business is now well placed to benefit increasingly from recent and expected order book growth in both the North American and Balconies and Balustrading businesses which is anticipated to have a positive effect on margins. The group are accelerating investment in people to seek to drive faster growth in North America. In the period the value of quotations for new work in North America amounted to £25.8M compared to £9.1M in the same period of last year.

The profit in the Roofing and Walling business was £825K, a decrease of £564K when compared to the first half of last year. After a strong start to the year Roofing revenues were similar to last year with a number of project delays experienced through the autumn, including a large green roof project now expected to complete in the second half of the year. Building contractors are being cautious in pricing and committing to new work in view of labour constraints and cost inflation, leading to a number of delays. The combination of project delays and cost inflation pressures impacted margins and this is being addressed through selling price increase, purchasing and other cost savings. The business is well placed to supply a higher number of projects for roofing refurbishing work in the education sector and this work is expected to start in Q4.

Revenues and profits at the Facades business were significantly below last year’s levels, reflecting further reduced government funding for refurbishment projects and uncertainties across the wider industry following the Grenfell tower disaster. The business was restructured in July, saving £300K per annum and the sales team has been re-organised to focus on driving specification sales working in conjunction with the technical sales team in the roofing business, in seeking to offset the lower level of government funding. Government funding support remains available in Scotland, however the phasing of the latest tranche of work is more second half biased this year so the board anticipate and uplift in the second half performance of the business.

The profit in the Water Management business was £1.5M, a decline of £350K when compared to the first half of last year. UK revenues in AWMS grew ahead of UK construction market growth rates, benefiting from increased specification sales and system selling across the “rain to drain” range.

Gatic’s revenues fell below expectations due to project delays which appears to have been in part attributable to the pace at which installing contractors were prepared to take on new work. After record export sales last year, the business had a quiet first half to this year for overseas work. Export spec levels remain buoyant and they are focused on converting these into further orders and sales in H2 but any further project slippage in this area would present a risk to the group’s full year performance expectations.

Divisional operating margins were impacted by the combination of lower sales at Gatic and commodity and other input cost pressures. The latter included the annualised effect of previously reported galvanized steel prices in the prior year impacting Gatic that could not be recovered; the EU customs duty imposed from August on certain imported cast iron products; higher aluminium costs; and currency-led inflation on imported materials.

Together with purchasing initiatives and internal efficiencies, AWMS should benefit from an increase in list prices from January 2018 and Gatic has also increased project pricing to recover the higher input costs. As was the case last year, the board expect divisional profitability to improve in the second half of the year as a result.

The profit in the Housebuilding and Ancillary Products business was £876K, an increase of £179K year on year. Timloc continues to outperform the growing UK new housebuilding market and again grew profits to new records, benefiting from new products including the “Above the Roofline” range launched last year. The business relocated from its two previous sites to a single, new build leased factory in East Yorkshire, a couple of months ahead of schedule. The relocation will enable the business to further expand and will provide additional manufacturing capacity.

There were three non-underlying items during the period. There was a £218K loss on disposal of the Scaffold and Construction products business; £323K relocation costs relating to the relocation of the Timloc business to a new purpose build leased premises; and there was a £426K profit on disposal of the group’s share of Amorim Isolamentos, a previously available for sale asset.

After the period-end the group acquired Wade International, a specialised drainage business, for £8M. The business manufactures and supplies metal drainage products and access covers and expands the group’s export sales capability for the Water Management division, particularly in the Middle East. Last year the business pre-tax profits of £1.4M and the board believe it will be earnings enhancing in the first full year following completion.

Going forward, group order books remain healthy at £25M, although this was below the £27.6M at the same point last year. Enquiries and specifications in the pre-order pipeline are buoyant across the group and continue to grow strongly at Levolux in particular. When taken together, these factors suggest an overall outcome for the year in line with previous expectations.

At the current share price the shares are trading on a PE ratio of 9.3 which falls to 8 on the full year consensus forecast. After a 3.5% increase in the interim dividend the shares are yielding 4.3% which increases to 4.5% on the full year forecast. At the end of the period the group had a net cash position of £2.4M compared to £6.1M at the end of last year.

On the 2nd February non-executive director Richard Saville purchased 5,000 shares at a value of £8,400.

Overall then this has been a bit of a difficult period for the group. Profits declined, net assets fell and although the operating cash flow improved, this was due to working capital movements and cash profits were lower. The drag on results has come from the facades business which has struggled following the Grenfell tower disaster and lower government investment. The water management business also suffered due to project delays. There is an expected improvement in the second half but there seems to be some uncertainty over timings and some projects seem to have a potential for further slippage. The solar shading business is doing well, however, with particularly good prospects in the US.

The uncertainty seems to be reflected in the valuation, with a forward PE of 8 and yield of 4.5% but I feel there is still potential downside here and I am not rushing to buy in here.

On the 16th March the group announced that non-executive director David Armfield purchased 20,000 shares at a value of £26K.

On the 15th May the group released a trading update. Construction activity was further impacted by adverse weather conditions that prevailed into the start of April. Market conditions continue to be slow in some segments which is restricting the pace of recovery and resulting in some projects that were previously forecast to contribute to this year now moving into the next financial year. In view of this, latest forecasts for the group’s performance are that revenues will be at least 7% below previous expectations and profit lower by 15-20%.

Activity levels across the group recovered in April, however, as the weather improved, and profit finished the month ahead of April last year. Latest forecasts for the group’s Q4 performance are also ahead of a strong prior Q4 comparator. The board is mindful of the mixed signals for the UK economic and construction activity but despite this have confidence in the longer term growth prospects for the group.