Tristel has now released their interim results for the year ending 2018.

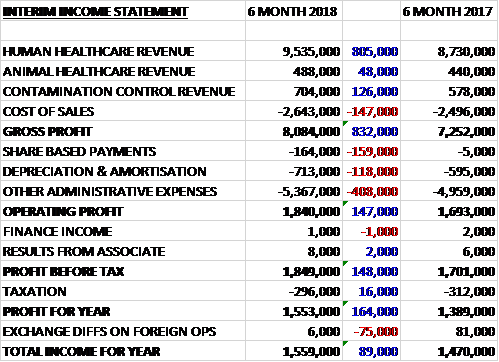

Revenue increased when compared to the first half of last year. Human Healthcare revenue increased by £805K, contamination control revenue grew by £126K and animal healthcare revenue increased by £48K. Cost of sales also increased to give a gross profit £832K higher. Share based payments increased by £159K, depreciation/amortisation was up £118K and other admin expenses grew by £408K, including £500K of costs incurred in the US regulatory programme, giving an operating profit £147K higher. Finance coats were broadly the same and tax charges declined by £16K which meant that the profit for the period was £1.6M, a growth of £164K year on year.

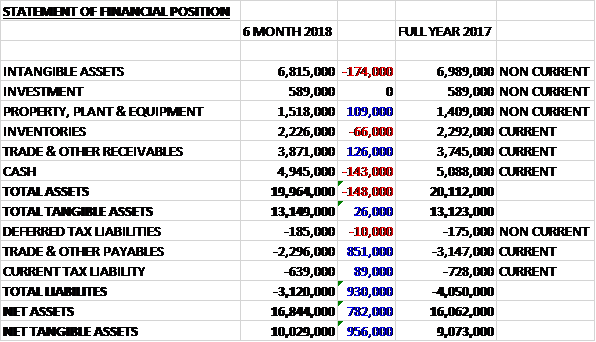

When compared to the end point of last year, total assets declined by £148K driven by a £174K fall in intangible assets and a £143K decrease in cash, partially offset by a £126K growth in receivables and a £109K increase in property, plant and equipment. Total liabilities also declined during the period, mainly due to an £851K decline in payables. The end result was a net tangible asset level of £10M, a growth of £956K over the past six months.

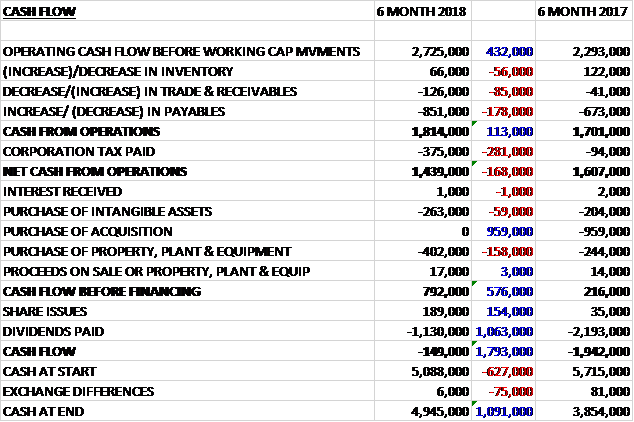

Before movements in working capital, cash profits increased by £432K to £2.7M. There was a cash outflow from working capital and tax payments increased by £281K to give a net cash from operations of £1.4M, a decline of £168K year on year. The group spent £402K on property, plant and equipment along with £263K on intangible assets to give a free cash flow of £792K. This did not cover the £1.1M spent on dividends and there was a cash outflow of £149K for the half year and a cash level of £4.9K at the period-end.

The gross profit in the Human Health division was £7.3M, a growth of £760K year on year. The gross profit in the Animal Health division was £309K, a decline of £23K when compared to the first half of last year. The gross profit in the Contamination Control division was £453K, an increase of £95K when compared to the first half of 2017.

Overseas sales grew strongly, up £1.2M whereas UK sales registered a decline of £200K due to the non-repetition of a £200K bulk purchase from the NHS. There was a particularly strong performance in Central Europe and Australasia. The Hong Kong business, traditionally managed through distributors, has declined recently so the group have terminated their distributor agreement and will employ their own team in the market. They have secured a cooperative hand over of the business, including two government contracts. They expect the increased margin from selling directly to exceed operational costs in the next year but in the second half of this year there will be an exceptional early termination payment of around £200K.

The group are working to reinvigorate sales growth in the UK market. In several key clinical departments in which they enjoy very high penetration in the UK, further growth opportunities are limited. In response they have developed new products for rinse water management in endoscope washing machines, and for surface disinfection in hospitals, and have high hopes for their success. Rinse water management involves both a capital and consumable sales and whilst first half revenues were modest, they have already achieved sales from sixteen installations in the UK and Australia. The new range of surface disinfectants will come to market in the second half of the year.

The group are progressing steadily with their planned entry to the North American hospital market having satisfied the additional data requirements of the EPA. A decision is expected during the second half of the year and the expectations continues that sales in North America will start next year.

The group have decided to employ their own team in the Hong Kong market having used distributors in the past. They expect the increased margin from selling directly to exceed operational costs in the next year but in the second half of this year there will be an exceptional early termination payment of around £200K.

Going forward, the group are on track to meet their objectives.

At the current share price the shares are trading on a PE ratio of 35.2 reducing to 33.5 on the full year consensus forecast. After a 14% increase in the interim dividend the shares are yielding 1.5% which increases to 1.6% on the full year forecast.

Overall then this has been a decent period for the group. Profits were up, as were net assets. The operating cash flow did decline, although this was due to working capital movements and cash profits grew. There was some free cash generated but this did not cover dividends. The overseas business seems to be very strong but sales were more sluggish in the UK where the group has reached market saturation point for most of its products. It is now developing new ones, however, so hopefully that will help going forward.

The entry into the North American market seems to be progressing to plan but all this news is in the price. The shares are not cheap with a forward PE of 33.5 and yield of 1.6% and I find it hard to justify a purchase at these levels.

On the 26th March the group announced that it had entered into a manufacturing and marketing agreement with Parker Labs USA whereby Parker will manufacture the group’s Duo chlorine dioxide foam disinfectant for the American market and will market the product in the ultrasound marketplace throughout the region. This collaboration prepares the group for its entry into the US infection prevention marketplace in advance of the grant of approval by the US EPA for Duo.

On the 23rd April the group announced that the US EPA has registered their foam-based chlorine dioxide product Duo. This enables the group to market the product to clean and disinfect hard, non-porous surfaces. The federal registration will be followed by state by state approvals which the group expects to complete by the end of 2018. They anticipate first revenues from the US in the year ending 2019 and will continue to pursue further registrations with the PEA and the Food and Drug Administration to build a broadly-based business in the US.

On the 13th July the group released a trading update covering the year as a whole. Results will be in line with expectations. They will report turnover of £22.2M and pre-tax profit of £4.4M, an increase of £300K. The group has no debt so net cash has increased from £5.1M to £6.7M.

In North America they are filing an additional submission to expand the allowable microbiological efficacy claims to enhance the competitive advantage of the duo product. They are also in the process of filing registrations in the first five selected states and are adding a second foam-based product format to their registration. Manufacture scale-up is underway at Parker labs. They have lodged a pre-submission review with the FDA who will provide a written response to the pre-submission review 90 days from receipt.

MODT is in the process of completing a further $5M fund raising as it continues the global roll out of its EVA System mobile colposcope. Tristel will participate in this funding up to its 3.22% shareholding. The group is deepening its relationship with MODT by combining the disinfection compliance audit app that is has developed with MODT’s app, contracting the software support functions to MODT and becoming MODT’s distributor in the UK, Australia and New Zealand.

It was also announced that Chairman Francisco Solar is retiring at the AGM in December.

All decent enough but this share is expensive and some success in the US is already priced in.