Sylvania Platinum is engaged in the extraction of platinum group metals, including Platinum, Palladium and Rhodium, from chrome dumps and current arisings, as well as investment in mineral exploration with all of the working operations being located in the Limpopo province of South Africa. The group is listed on the AIM exchange and has now released its final results for the year ending 2014.

When compared to last year, revenues increased driven by a $3.8M growth in sales at Tweefontein and a $3M increase in Mooinooi revenues, somewhat offset by small declines at Lannex and Doornbosch. Direct operating costs also increased, including a $1M increase in staff costs but gross profit was still some $3.5M higher at $4.3M. At the operating level, there were a number of one-off costs that affected performance. There was a detrimental $611K swing in foreign exchange losses, a $1.6M impairment of exploration assets relating to the group’s Everest North porject and a $1.3M impairment of investments in associates relating to the 25% interest in the Chrome Tailings Retreatment Project. In addition, last year there was a $9.9M gain on the disposal of a subsidiary, relating to the sale of the magnetite iron ore assets to Ironveld. So despite other general costs falling by $1.5M the operating loss was a negative swing of $8.3M. This was exacerbated by a more than doubling of tax charges relating to temporary differences in the value of property plant and equipment so that the loss for the year was $5.1M, a $9.5M reduction on the profit made last time, although it is worth noting that if we discount the sale of the subsidiary last time and the impairments, there would have been an improvement on 2013.

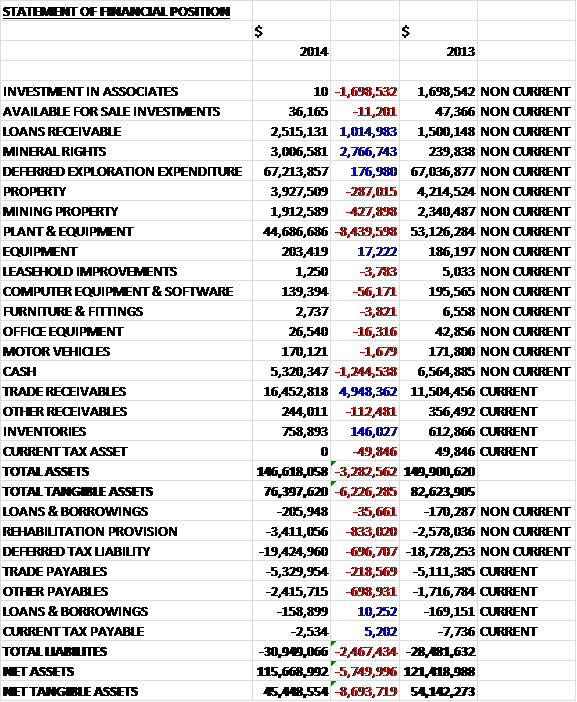

When compared to the end point of last year, total assets fell by $3.3M. This was driven by an $8.4M decline in the value of property, plant & equipment, a $1.7M fall in investments in associates and a $1.2M decline in cash levels, somewhat offset by a $4.9M increase in trade receivables, a $2.8M increase in mineral rights and a $1M growth in loans receivable relating to a loan given to Ironveld. Liabilities increased during the year, driven by an $833K increase in rehabilitation provisions, a $697K growth in deferred tax liabilities, which seems to relate to temporary differences in the value of property, plant & equipment, and a $699K increase in other payables. The result was an $8.7M fall in net tangible assets to $45.5M. This is a disappointing decline but the balance sheet seems to remain fairly strong.

Before movements in working capital, cash profits were some $3.9M higher than last year at $9M. This was eroded by a large increase in receivables so that the net cash generated from operations was $1M higher at $5.1M. This cash was soon swallowed up, however, as $1.2M was spent on property, plant & equipment, $3.5M was spent on exploration and evaluation and $1.1M was paid in loans to Ironveld which meant that there was a negative $453K cash flow before financing operations. A small payment for treasury shares later allocated to senior managers and some loan repayments meant that the cash outflow for the year was $896K, a vast $6.9M improvement on 2013 and meant that the cash at hand by the end of this year was some $5.2M.

Profits at Millsell were $2.2M which was a $400K improvement on profits in 2013. This is one of the most consistent production plants and increased production by 18% to 7,908 ounces for the year. Recovery efficiencies were slightly lower, associated with the final scrapings of the Waterkloof dump but it was a combination of the improved plant feed grades and higher plant throughput rates that led to the production increase. The second pass treatment of the 1MT primary dump is planned to commence in 2015 which should help maintain the consistency seen here at this mature plant. The total cash cost at the plant fell by 4% to $516/Oz against a sales price of $970/Oz averaged across the group.

Profits at Steelpoort were $1.1M, a decent $600K improvement on last year. This plant is still processing second pass treatment material from the old Steelpoort tailings dams and produced 7,751 ounces during the year which was a 12% increase on last year’s total and primarily due to an improvement in the recovery efficiency. Next year the plant will continue to process the same material and aim to further increase recovery efficiency and feed rates. The cash costs were 12% lower than last year at $673/Oz.

Losses at Lannex were $689K, which was a deterioration of $544K when compared to the lower losses last year. This was a challenging year for the plant with unexpected maintenance costs during the fourth quarter of the year and lower feed grades. This operation treats a combination of dump material from the old Lannex tailings dam complex and current arisings from the host mine’s Lannex operation. Despite the lower grades associated with the coarser outer walls of these tailings dams, the operation increased production to 8,028 ounces as the plant saw a significant increase in PGM plant throughput and a small improvement in recovery efficiency. Plans for the upcoming year are to start second pass treatment of the new Lannex tailings dam and to continue to treat current arisings from the host mine. Cash costs were 6% higher than last year at $725/Oz.

Losses at Mooinooi were $1.8M which was almost half the $3.5M of losses that occurred in 2013. The Mooinooi dump experienced a few production issues throughout the year but still managed to increase production by 54% to 6,918 ounces due to a 32% improvement in PGM plant feed tonnage and a smaller increase in recovery efficiency. In the second quarter there was a Section 54 stoppage notice at the plant which resulted in a 21 day production stoppage and various improvements in safety actions. The plant treats material from the old Mooinooi dumps and current arisings from the host mine’s Mooinooi plant. Costs for the year improved by 27% to $764/Oz. The Mooinooi ROM plant was also affected by the Section 54 stoppage but production for the year increased by 27% to 4,953 ounces. This plant treats MG2 material from the host mine’s Mooinooi and Buffelsfontein underground mines and the group achieved optimisation of a fine grinding toll milling circuit during Q3. Despite a 17% fall in cash costs to $1,084/Oz, they remained higher than target levels and the reduction in costs per ounce is the priority for this plant in the coming year and achieving a higher plant throughput is seen as the best way of achieving this.

Doornbosch enjoyed profits of $3.1M, although this was some $300K less than last year. This operation transferred focus in the second half of the year to treating lower grade second pass material from the old Doombosch dump together with final scrapings from the old Montrose areas and these sources are expected to be depleted during the first half of 2015. High grade pockets of material have been uncovered with the final scrapings of the Montrose footprint, however, which already assisted in boosting production during Q4. In all the plant produced marginally less than last year at 9,919 ounces but due to the new material being found, the plant had a record level of production in Q4. The plant feed grade should reduce and normalise once the operation converts to a combination of full second pass treatment of the current Doornbosch tailings dam and current arisings from the host mine during the next six months. The focus will be on increasing plant feed tonnes, improving grade and reducing chrome in concentrate in order to reduce smelter penalties. Due to a significant maintenance repair costs following an abnormal breakdown in the primary mill during the third quarter costs increased by 8% to $516/Oz.

Tweefontein had profits of $610K, a very pleasing reversal of the $905K of losses that occurred last year. The operation more than doubled production to 8,331 ounces due to a ramping up in production and higher stability after the plant commenced production in 2012. The plant is treating fines from the host mine’s Klarinet opencast mine, current arisings from the host mine’s Tweefontein operations and old dump material from the Tweefontein paddocks. The primary focus during the year was to stabilise production and to optimise recovery efficiencies with production levels expected to improve during the next financial year. The upgrade to the power supply infrastructure eliminated the need to run the diesel generators for extended periods, which helped reduce the cost to $648/Oz.

The outcome for an application for mining rights at Harriet’s Wish, Aurora and Cracouw is still pending but following a decision to scale down exploration, only essential exploration activity has been conducted with no further activities envisioned in the short term. An environmental impact assessment was submitted to the MRA on Volspruit in January and a flood event at the river was witnessed in Q3 which provided essential data that backed up a report from the environmental assessment practitioner that the proposed activity does not pose any significant risk to the environment that cannot be managed through mitigatory measures and therefore the EAP recommended that the project proceed with a decision from the DMR regarding mining rights imminent.

As part of the Volspruit project, the company purchased the surface rights to the Grasvally and Zoetveld farms adjacent to Volspruit in 2013 and in 2014 entered into an agreement to purchase the prospecting rights over this land for a consideration of $2.5M. Surface exploration of the Grasvally upper chrome seam outcrop have indicated Cr2O3 values of 46.4% Cr2O3 in situ with a chrome iron ratio of 2.45:1 but further studies suggest that the main seam may be upgraded to 55.5% Cr2O3 with 62% recovery after only one washing pass but tests also suggested that the crown pillar in some of the previously mined areas is shallower than first expected. The company has commenced with exploring the application for a mining right on the property and has spent $250K on the project so far, not including the acquisition rights mentioned above. This is a brownfields site that was originally closed in 1988 but the high quality of chromite means that the project is expected to not only pay for itself but in the long term should also provide significant PGM resources. In a best case scenario, management consider the group to be at least two years away from being able to start construction.

As we have seen there was a $1.3M impairment of the group’s 25% investment in CTRP as the plant is on care and maintenance and no agreement has been reached to restart the operation. This means the carrying value of the investment is now zero. There was also a $1.4M impairment of the group’s Everest North project. This is a joint project with Aquarius Platinum and the viability of the project depends on the operation of their Everest South processing plant which was placed on care and maintenance in 2012 with no apparent plans to restart the operation. The carrying value of this asset is now zero. Finally, there was a further $181K impairment on a prospecting right that expired and was not renewed.

During the year the platinum price has been muted due to excess stocks being held due to the ongoing strike actions. Into 2015, prices have been weak and the situation could continue for some time as improving automotive demand slowly draws down the excess stocks. The palladium market has powered ahead due to improved automotive demand in North America and Asia. It is thought that ongoing strike action could cause the mothballing or closure of some mines which may result in a tighter market that would bode well for platinum prices.

The group is heavily reliant on two customers which together make up over 99% of total sales with has clear risks attached to it. Another thing to be aware of is that repatriation of funds from South Africa is subject to regulatory approval. Another risk is the susceptibility to currency changes with a 15% appreciation of the Aussie dollar against the South African rand giving the group a $964K loss. Clearly one of the main risks, however, is the exposure to commodity prices, in particular Platinum group metals which the group does not hedge against. A 10% fall in PGM prices would result in a $763K loss with a 10% appreciation giving the profit of the same value.

Other risks more specific to the company include the fact that the retreatment of dump material has a finite life and it is essential to for the long term continuation of operations that additional feed material is found and committed to the plants. Also, South Africa has experienced continuing problems with strikes. There was a five month strike in the first half of the year and despite no employees of the group being involved, the effects of the strike were far reaching.

During the year the group received notification that Platmin had removed the summons for hearing due in August 2014. Platmin claims co-ownership of the tailings contained in the Lannex dam. A similar case has previously been brought that resulted in the claim being withdrawn and Platmin paying all costs. The withdrawal this time is expected to be temporary and it is thought Platmin still intends to proceed at a later date.

Going forward the board is confident that as a low-cost producer the business will continue to perform despite adverse economic circumstances with focus in the upcoming year on free cash flow generation and maintaining the consistent production of 53,000 PGM ounces during the year, a similar level to this year. In addition, the board are investigating the possibility of returning capital to shareholders through a dividend policy barring any negative changes in the Platinum or Rhodium price. The management have also stated that they are not looking to tap up shareholders for capital or take on any unwarranted debt in this climate so will probably spin off or enter into a joint venture over the Grasvily project.

As the group suffered a loss this year, the P/E ratio was -7.7 but on next year’s forecast it is a very cheap looking 5.8. The dividend yield for next year being forecast by WH Ireland is about 4.2% which doesn’t sound too bad. This was a mixed set of results for the group. The fall in profits is due to one-off items and now that some of the low quality assets have been impaired, perhaps this will draw a line under them. The knock on effect is the declining net asset base, predominantly due to the fall in the value of property, plant and equipment although the balance sheet is steel relatively strong. Operational cash flow improved but there was no free cash flow after capex was taken into account. It should be pointed out though, that this would not have been the case if it weren’t for the exploration costs that the board are stating is unlikely to repeat. Once the problems are sorted out at Lannex and Mooinooi and the exploration costs come down, I can see performance improving here. Risks remain, however, as the price of platinum seems to be subdued by higher supply and the threat of strikes in South Africa continues to loom. I will keep watch here but this seems a bit risky for me at present.

On the 7th November the group released an update. The Sylvania Dump Operations (SDO) exceeded expectations over the last 18 months, with six consecutive quarters of continuous growth. Increased production levels and technical focus, combined with specific improvement initiatives across all operations, contributed towards this. A project to move from mechanical mining to hydromining at all plants will improve feed stability to plants and to reduce mining costs going forward. This project commenced in August 2014 with completion expected by the end of Q2 2015. The company has signed a new offtake agreement for the concentrate produced by the SDO and improved terms were secured going forward.

The Company also announced that it has received permission to remove and dispose of a bulk samples of Chrome recovered in the course of prospecting operations on the Grasvally and Zoetveld properties. Based on the high chrome to iron ratios found during the initial exploration phase of the project, the Company believes that the test work to be done on the ore removed by the bulk sample will prove that the chromite is of unusually high quality by South African standards. In summary, the combination of the stable production profile, improved offtake and Section 20 permissions results in the Company having an improved outlook for the financial year which sounds pretty good to me.

On the 30th January the group released a statement covering Q2 trading. After a good Q1, the ounce production declined during the second quarter but still exceeded the business plan production for the period. This reduced production was due to the start-up of hydro mining as well as the planned holiday shut down during the Christmas period. Overall, 14,701 ounces were produced and group cash costs were $691/Oz, an increase of 21% on last quarter, largely as a result of converting all operations to hydro mining. The price of the PGMs was pretty much at $893/Oz but revenues only fell by $11% to $13M due to improved concentrate sales terms negotiated during the period. The cash balance stood at $7.8M, a $1M increase on the previous quarter and about double the level this time last year. Despite the short term increase in costs, the change-over to hydro-mining is expected to reduce mining costs by 20% going forward.

During the year the Lannex, Doornbosch and Steelpoort plants all suffered lower PGM feed tonnes and recovery efficiencies which was mostly attributable to the change to hydro mining but also the final scrapings at the current Steelpoort dump. After corrective measures have been put into place, the operating performance at these sites is expected to return to normal levels in Q3. The company continues to wait for the outcome of the application for mining rights at Volspruit but they are commencing with the public participation of the water use license application. At the Grasvally Chrome exploration site, testing and samples removed will be used to further prove the high chrome to iron ratios of the orebody and further exploration will consist of a drilling programme in the north of the property for a near surface resource and additional drilling will be performed to categorize the deeper underground resources. Overall this was a decent update but I still feel there are too many risks at this time.

As we can see, the chart looks a little volatile but the company does seem to be starting to improve from the lows in September, as seen by the gentle incline of the 200 day moving average. Both the share price and the 50 day MA are above this marker which suggest the group may be over the worst.

A look at the longer term chart shows rather a different story. This share has been through some tough times but does seem to have leveled off. I think I would like to see some evidence of a more sustained upturn before buying though.