Solid State has now released their final results for the year ended 2017.

Revenues increased when compared to last year as a £149K decline in distribution revenue was more than offset by a £3.4M growth in manufacturing revenue. Cost of sales also increased, to give a gross profit £568K higher. There was a £162K growth in the amortisation charge but a £174K reduction in share based payments. Other admin expenses were up £500k, however, so the operating profit was broadly flat, increasing by just £35K. Finance costs fell by £70K but tax charges increased by £119K, due to deferred tax credits last year, which meant that the profit from continuing operations was £2.2M, a decline of £224K year on year.

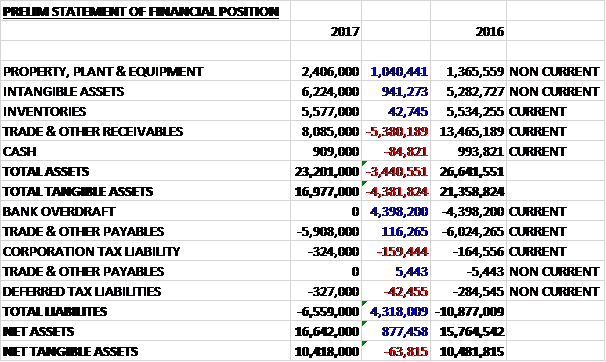

When compared to the end point of last year, total assets declined by £3.4M driven by a £5.4M decrease in receivables, partially offset by a £1M growth in property, plant and equipment, along with a £941K increase in intangible assets. Total liabilities also declined, mainly due to a £4.4M reduction in the bank overdraft. The end result was a net tangible asset level of £10.4M, broadly flat year on year with a fall of just £64K.

Before movements in working capital, cash profits declined by £2.7M to £3.1M. There was a cash inflow from working capital due to a large decline in receivables and after tax payments increased by £211K, the net cash from operations was £9.1M, a growth of £7.4M year in year. The group spent £1.5M on property, plant and equipment, £426K on intangible assets and £2.1M on acquisitions to give a free cash flow of £5.3M. Of this, £1M was spent on dividends so the cash flow for the year was £4.3M and the cash level at the year-end was £909K.

The revenue delays on a number of the antenna projects have been more than offset by the additional batteries revenue from the Creasefiled acquisition. The gross margin did falls somewhat, however, reflecting the changing mix of sales combined with the additional Creasefield sales which are typically lower than the average margins for the manufacturing division.

The profit in the distribution division was £896K, a decline of £70K year on year with billings flat as the business investing in staff to accelerate growth next year. During the year the group recruited experts in the area of sourcing and obsolescence to form the sourcing and obsolescence team which provides a new revenue stream for the division.

The division also invested heavily in its technical field sales team increasing the resource by about 25% to give greater account coverage, improved service and to take advantage of the cross-selling opportunities within the group which adds about £250K per annum in costs. The outlook for next year is strong with the Electronic Component Supply Network reporting that early indications suggest the upper limit of the industry wide growth forecast of 4.3% may be understated. The division is now well positioned to exceed this industry wide forecast and has seen a strong start to Q1 with record order intake in the first two months of the year.

The profit in the manufacturing division was £2.2M, an increase of £27K when compared to last year. The division saw billings increase by £3.3M but the Creasefield acquisition added £4.2M of revenue which mitigated for delays in a number of antenna contracts seen in the communications business. The discontinued SEMS business unit contributed £7.3M of revenue in the prior year which has not recurred as a result of the termination of the business unit, although this is not included in the above figure and like for like revenues declined due to the antenna contract delays.

The computer business unit has geared up with additional sales resource in the second half of the year, responding to increased demand as a result of directed marketing efforts including advanced use of SEO and Google Adwords.

The Creasefield battery business was acquired in May, complementing the existing battery business unit. This has resulted in an extension of market reach, with a customer base extending beyond the oil and gas sector to include Medical, Aerospace, Utilities and Defence sectors. The facility has brought increased capacity, technical resources and long standing supplier relationships. In addition it has brought exposure to new battery chemistries and charging technologies, significantly adding to the capacity and capability of their batteries business unit.

As part of the acquisition integration plan they transferred their battery business unit in Reddich into the Creasefield Crewkerne facility, incurring £200K of one off costs (their strategy involves an acquisition a year so these costs are not one-off!). The acquisition added £200K to profits this year. Margins at Creasefield are typically lower than the other business units of the manufacturing division albeit this is an area of focus for improvement. The year saw a demonstrable recovery of the oil and gas sector, where the group produces power solutions for pipeline inspection gauges, with strong battery bookings from customers in this sector in Q4. Strong orders were received in the latter part of the year as prime contractors rebuilt stock levels.

In the communications business, the antenna manufacturing was relocated to a purpose built facility in Hertfordshire in January 2017, after a capital investment of around £1M. The new facility is able to design, manufacture and test complex systems and is large enough to accommodate antennas with a dish diameter of up to three metres. In addition, environmental testing facilities have been relocated to the site and will be commissioned later this year alongside vibration testing facilities for use across the group. Investment has continued with the addition of technical and commercial staff and the business unit is resourced for growth.

Steatite has won the persistent systems franchise for distribution of the secure wave relay mesh network mobile, providing HD video and voice in the most severe environments. They have also secured contracts to supply radio systems to the MOD both directly and through contractors. An important export order for the mesh radio solution was secured in the Asia Pacific region with strong potential for additional systems. A long standing relationship with the provider of an advanced satellite communications system has secured ongoing business with the MOD for maritime applications both surface and underwater.

On commercial grounds the group made the decision to close the self-funded Steatite Electronic Monitoring Systems business unit in the latter part of the year, allowing the manufacturing division to concentrate on its core activities. Following the termination of the MOJ contract, the board had decided it was appropriate to explore if the group could commercialise the IP they developed as part of the contract. At the end of the year, however, the board took the decision that returns would not be sufficient to warrant continued investment and development in the SEMS market.

Going forward, the group finished the year in a stronger position, having focused investment on the areas that will deliver the future strategic goals of profitable organic and acquisitive growth. Additionally the group has made significant investment in the management, sales and operational teams to position it to deliver the future growth in 2018 in line with expectations. The board believe that the group, with its diversified structure, increasing export sales, new opportunities with battery chemistries, additional antenna capability and higher margin products, is now well placed to deliver organic growth.

Activity levels are encouraging across both divisions. Leading edge indicators which include the open order book (up 16%) give the board confidence in the prospects for the group next year and trading in line with market expectations.

At the current share price the shares are trading on a PE ratio of 17.5 which falls to 14.4 on next year’s consensus forecast. After the final dividend was kept the same, the shares are yielding 2.5% which increases to 2.6% on next year’s forecast. The board has now agreed a new dividend policy whereby they will target a dividend cover between 2.5 and 2.75 adjusted earnings in future periods. At the year-end the group had a net cash position of £900K compared to £3.8M at the end of last year.

Overall then, results have been a bit flat this year. Profits were flat, net tangible assets were stable and although the operating cash flow improved due to a big decline in receivables, cash profits fell. There was a decent amount of free cash generated, but again this was due to the collection of receivables, without which there would not have been any.

The distribution division saw a small decline in profits due to investments targeting future growth with the board expecting growth next year. The manufacturing division saw a modest increase in profits due to the Creasefield acquisition, without which there would have been a like for like decline due to delays in antenna orders. Going forward, the group does seem well placed to grow in the coming year, assuming their markets remain decent. With a forward PE of 14.4 and dividend yield of 2.6% this looks OK value. I’m in two minds over this one!

On the 23rd October the group released a trading update covering the first half of the year. Group revenue increased by 12% to £22.5M reflecting strong organic growth in the distribution division of 20% and a 7% increase in the manufacturing division. Product line margins in both divisions have been maintained but changes in product mix affect overall group gross margin and in this period, the combination of the increased proportion of distribution sales and change in mix of sales in the manufacturing business has resulted in a group gross margin of 28%, down from 31%.

The investment in and restructuring of the communications business unit and Leominster operations is now complete and has positioned the group for future growth. Despite an improvement in revenues relative to last year, the lead time to win and deliver some of the complex antenna programmes is taking longer than expected, resulting in a performance below management expectations. The prospect pipeline remains strong, positioning the business unit for a stronger 2019.

Planned investment to drive long term organic growth and margin enhancement across the group increased overheads from the start of the year. The benefits of these initiatives are starting to be realised and good progress is being made in implementing the margin enhancement strategy through additional added value services and operational efficiencies, the benefits of which should be seen in the next financial year.

As a result of the product mix and increases to overheads through the investment in growth and margin initiatives, the board expects pre-tax profit to be slightly lower than current market expectations for the full year, although the open order book at £18M is higher than the £14.8M at this point of last year.