API is a manufacturer of speciality foils and packaging materials serving markets in Europe, North America and Oceania from production operations in the UK and the US. The main markets for the products are consumer goods and printed media. The laminates business includes metallised film laminates, holographic laminates, aluminium foil laminates and Fresnel lens laminates and markets include tobacco, wines, confectionary, health, beauty and personal care. The foils products include metallic hot stamping foils, pigment foils, holographic foils, coding foils and holographic lamination film and markets include wines, confectionary, greetings cards, magazines, footwear and office products. The products under the Holographics sector include custom holographics, holographic overlays, tamper evident seals and scratch off foils. Markets include premium branded goods, dutiable goods, pharmaceutical goods, tickets and vouchers. API has now released their final results for the year ending 2014.

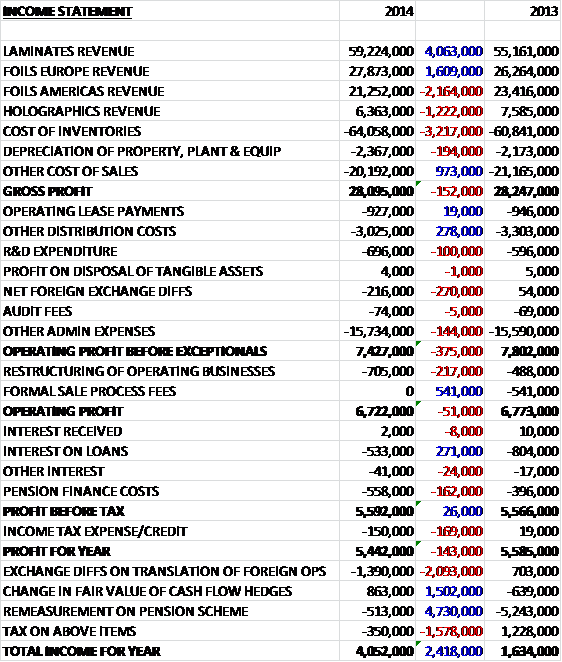

Revenues increased in the Laminates and European Foils business but fell in the Americas Foils and Holographics business. Cost of inventories also increased to give a gross profit some £152K lower than in 2013. A fall in distribution costs was counteracted by an increase in Admin expenses so that before exceptional items, operating profit was £375K lower than last year. The lack of a sale process fee that occurred last year meant that actual operating profit was just £51K lower at £6.7M. The group spent over £1M on loan interest and pension costs but the interest was £271K lower than in 2013, counteracted by a nominal tax charge (compared to a small rebate last year) due to historic losses. There remains £2.1M of tax losses in the UK and $4.1M in the US. This meant that the profit for the year, at £5.4M, was £143K lower than in 2013.

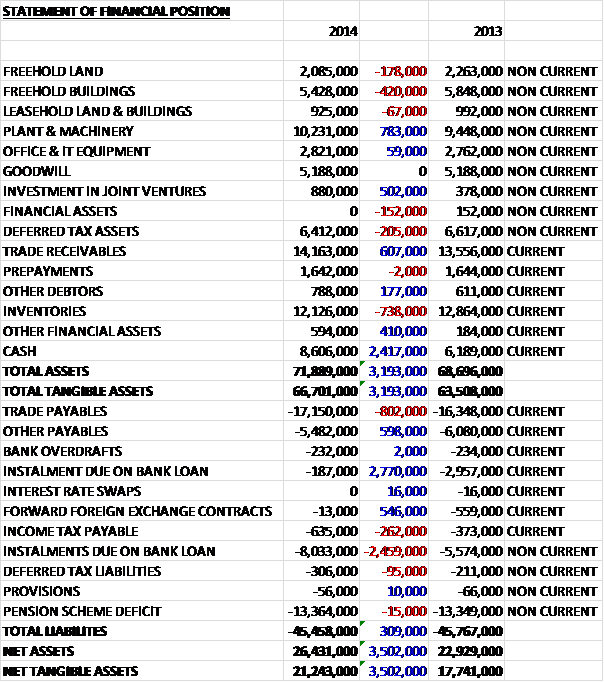

When compared to the end point of last year, total assets increased by £3.2M driven by a £2.4M increase in cash levels, a £600K hike in trade receivables and a £783K growth in plant and machinery, somewhat offset by a £738K reduction in inventories and a £420K fall in the value of freehold land. Liabilities remained fairly flat as an £802K increase in trade payables was offset by a £598K fall in other payables and a £546K decline in forward foreign exchange contracts. Overall, net tangible assets increased by £3.5M to £21.2M.

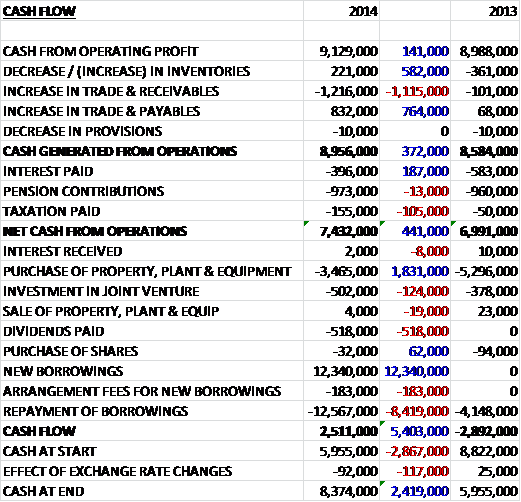

Before movements in working capital, cash profits were £141K higher at £9.1M. An increase in receivables was broadly counteracted by other working capital movements so that cash generated from operations increased by £372K to just under £9M. The group spent almost £1M of this cash on the pension scheme and just under £400K on interest to give a net cash from operations of £7.4M. Nearly half of this, £3.5M was spent on the tangible asset purchases including two new foil metallisers and a new IT system, and half a million pounds was spent on joint ventures, relating to API Optixin the Czech rep. There was also half a million spent on dividends to result in a cash inflow of £2.5M which is a pretty decent result.

Laminates made a profit of £6.7M, a £200K increase on last year. During the first half of the year the laminates business experienced lower demand due to a net adverse churn of customer packaging specifications moving between laminate and non-laminate constructions and a reduced volume on one of its key supply positions. In the second half this was more than compensated by the commencement of bulk shipments against the major new supply contract produced on the newly installed laminator and revenues were 25% higher than the comparative period last year. Operating costs in the business increased due to higher spend on plant maintenance and sales & marketing.

Foils Europe made a profit of £2.1M compared to £2M in 2013 despite some disruption caused by the reorganisation of the UK operations (along with a £200K one-off cost). The Polish distributer managed to double sales during the year, further progress was made in Italy and there was an increased contribution from Germany. These gains were offset by lower revenues in the UK and Australia, which was hit by a factory closure at a key client in the label sector. The board has now approved capital investment for expanding the Livingston manufacturing plant as it is now fully loaded following the repatriation of volume from the failed Chinese joint venture.

Foils Americas made a profit of £1.7M, a decline of £200K compared to last year. The decline was due to a sharp fall in orders in Q4 in the metallic pigments sector due to reduced conversion activity at one key customer. Sales of decorative foils were also lower than last year due to a slow-down in the US during the harsh winter period. These declines were mitigated by a more favourable sales mix to higher margin products, lower raw material costs and a partial reversal of last year’s reduction in inventory.

Losses at Holographics widened from £275K in 2013 to £724K this year as a long standing supply arrangement ended after a customer took production in house and the timing of shipments on another contract impacted year on year comparatives. Despite these increasing losses for the year, most of the damage was done in the first half and cost cutting initiatives enabled Q4 to break even. Going forward, the target remains to increase API’s presence in the security and authentication market but progress has been slower than expected and undermined by the loss of one particular supply position but investment has been made in the division, including in the Czech joint venture.

There are currently two customers in the Laminates segment who represented over 10% of total revenue with one accounting for as much as £22.8M. It seems to be a real potential issue for the group that they are a number of key clients and they are very reliant on a few supply contracts as can be seen in some of the lower sales in some sectors this year.

Going forward, the board expects the stronger second half trading to continue into next year but it is unclear as to how long Foils America will be affected by reduced demand from metallic pigment customers. The board believe that any impact on the results should be compensated by the elimination of trading losses at Holographics and the benefit from last year’s restructuring at Foils Europe, however. Foils Europe continues to experience steady overall demand whereas recent activity in the decorative foils market in North America appears somewhat slower than usual. At the laminates business there is a good pipeline of new business projects which it is hoped, will improve performance going forward.

The group is currently in a position of £154K of net funds compared to £2.6M net debt last year. At the current share price the P/E ratio is a very cheap 7.1 rising to 7.6 on lower earnings forecasts next year. At the current share price the dividend yield stands at 4% rising to 4.3% next year which seems pretty decent. The business is cash generative, net assets are increasing and there is a good dividend yield but the loss making Holographics division and the slow-down at the Americas foils business makes me reluctant to dip in here until it is more clear as to whether demand will improve in the near future.

On the 3rd September the group released a statement that indicated the duration and severity of the down-turn at the Foils Americas business was greater than expected and the unit is likely to post a small loss for the year. The losses at the Holographics division seem to have reduced and the unit is now break even but this is not enough to compensate for the losses at the Americas Foils business and results this year likely to be behind those of last. This is clearly not good and I am staying out of the shares. I will only update this blog now if things change with regards to trading.

Well, after deciding these shares were not for me, as of the 22nd January we now have some major news. Cedar, a subsidiary of Steel Partners has announced that it will make an offer for the company of 60p per share. This morning the shares were trading at 47p so this is quite a premium. The group is already the largest shareholder in API, holding 32.3% of the total share capital. In addition to this, Cedar has received letters of intent to accept the offer for further shares that brings their holding up to 62% and if they receive enough to make this up to 75% then they will procure a cancellation of the admission of the API shares to trading on AIM. I have to say this seems to be a good opportunity for existing shareholders to exit a company that seems to be going nowhere for a decent premium on the last closing price. The board of API suggest that investors do nothing and see what happens.

On the 9th February it was announced that the acceptance condition of the offer has been satisfied and that all other conditions of the offer have either been satisfied or waived such that the offer has become unconditional. It seems this is pretty much all over.