Arbuthnot has now released its interim results for the year ending 2016.

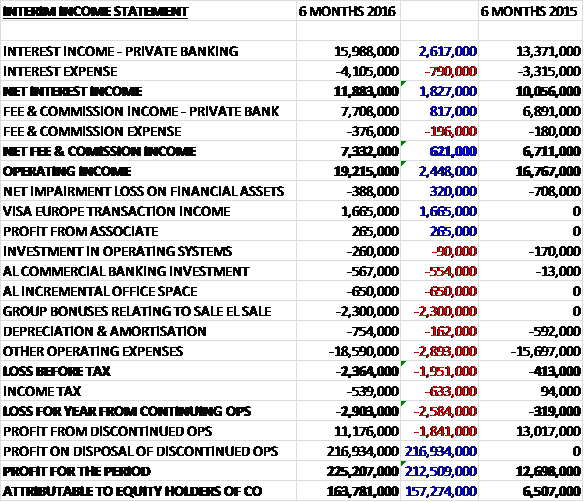

Net interest income was up £1.8M and net fee & commission income increased by £621K to give an overall operating income that grew by £2.4M. The group gained £1.7M from the Visa Europe transaction and received £265K from Secure Trust in the period that it was an associate following the sale of shares. There was a £554K increase in commercial banking investment, a £650K cost associated with increased office space and a £2.3M charge relating to staff bonuses following the sale (this could possibly be included in discontinued ops?). We also see a £162K growth in depreciation and amortisation along with a £2.9M increase in other operating expense to give a £2M detrimental movement before tax. After tax costs increased the loss for the year from continuing operations was £2.9M, an increase of £2.6M year on year although due to the disposals, the actual profit was £157.3M.

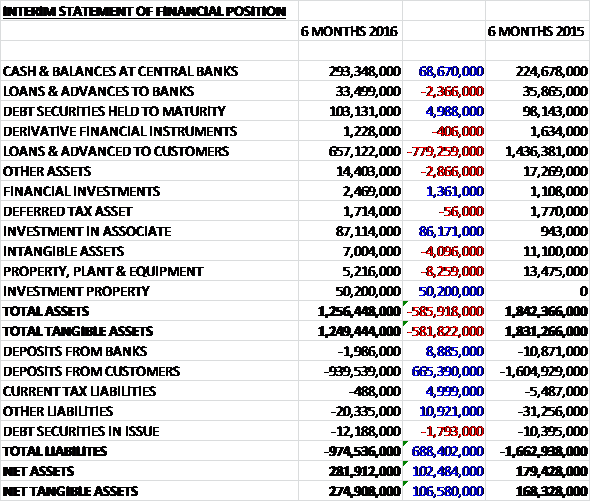

When compared to the midway point of last year, total assets declined by £585.9M to £1.256BN driven by a £779.3M fall in loans & advances to customers, an £8.3M decrease in property, plant & equipment and a £4.1M decline in intangible assets, partially offset by an £86.2M increase in investments in associates relating to the shares in Secure Trust; a £68.7M growth in cash and a £50.2M investment property. Total liabilities also declined during the year due to a £665.4M fall in deposits from customers, a £10.9M decline in other liabilities, an £8.9M decrease in deposits from banks and a £5M fall in current tax liabilities. The end result was a net tangible asset level of £274.9M, a growth of £106.6M year on year.

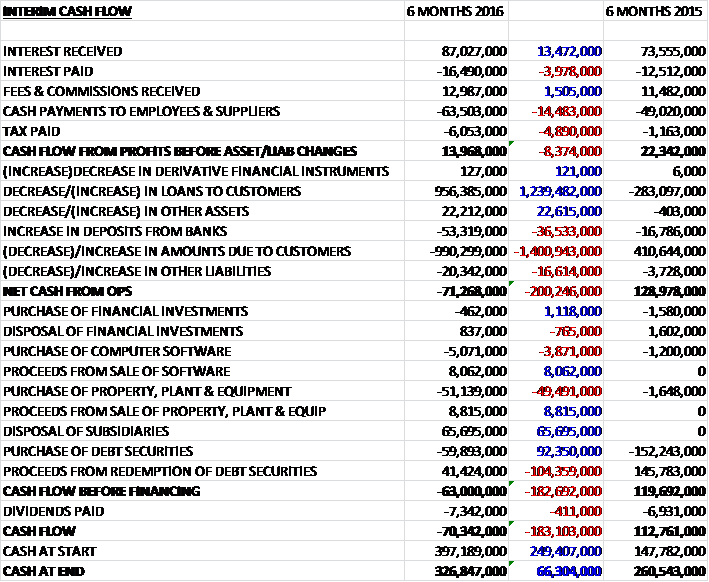

Cash profits declined by £8.4M to £14M and there was a large cash outflow from working capital due to a big fall in amounts due to customers so that there was a net cash outflow of £71.3M from operations (there was a total outflow of £43.7M from discontinued operations). The group spent £5.1M on computer software but managed to get £8.1M from the sale of software. They also spent £51.1M on property, plant and equipment and a net £18M or so on debt securities before a £65.7M gain from disposals and a £8.8M in proceeds from sales of property, plant & equipment meant that the cash outflow for the period came in at £70.3M to give a cash level of £326.8M at the period-end.

In December the group agreed to the conditional sale of its non-standard consumer lending business, Everyday Loans., to Non Standard Finance for £106.9M in cash and £16.3M in Non Standard Finance shares. The disposal completed in April and on completion, Non Standard Finance repaid intercompany debt of £108.1M to Secure Trust and after selling costs of £6.2M this resulted in a gain recognised on disposal of £113.3M.

In June the group sold 6M shares in Secure Trust Bank which reduced its shareholding from 51.92% to 18.93%. From this date they accounted for the remaining holding in STB as an associate and they retained board representation. As a result of this transaction the group recognised a gain of £100M.

The group will continue to invest in its remaining subsidiary to accelerate the growth in the Private and Commercial banking business. Given the current market conditions, they will also explore other opportunities to enhance and diversify its income streams. Meanwhile, Secure Trust will now explore the opportunity of achieving a listing on the main market and will be able to expand its horizon for growth opportunities that enhanced access to capital markets will allow and the group are looking to maintain a significant investment in the bank.

Due to the sale of shares, however, the profit from the Secure Trust Bank has had to be recorded as discontinued operations. Given that the group retains 18.9% of the shares and that Secure Trust is considered an associate, this does under-represent the profit from continued operations. On a pro forma basis, the continuing income from the associate for the first half of 2016 would have been £2.5M, an increase of £900K. (The reported earnings from the associate for the period after the disposal was £300K) so it could be argued that continuing profits are understated by £2.2M during the period.

Arbuthnot Latham reported a pre-tax profit of £4.5M, an increase of £800K year on year which includes the impact of the investment programme that commenced during 2015 with the building out of the commercial banking business and the banking infrastructure upgrade project which offset a 13% increase in revenues. Customer assets continued to grow, increasing by 14% to £657M while deposits increased by 23% as the bank continued to attract new clients. Assets under management increased by £96M to £797M.

The investment in the commercial banking activities totalled £600K in the period. Three sector teams have already been established in London while further teams are due to establish a presence in Manchester and Exeter to cover those regions. In June the business completed the purchase of a property in the West End for £50.2M. This is expected to initially be held as an investment property receiving about £1.8M rental income per year but in due course the bank will explore plans to establish a West End client office in the building.

Given the result of the EU Referendum, the UK economy faces short-term economic volatility. The board believe that the group is well positioned to prosper, however. It has divested its high margin lending business which is the more likely to experience increased impairments during a downturn and realised a significant proportion of the investment in Secure Trust. It is therefore highly capitalised and well place to take advantage of any opportunities that might arise.

After the interim dividend was increased by 1p and a special dividend of 25p was declared, the shares now have a yield of 3.8% although this is expected to fall back to 2.1% next year without the benefit of the special dividend.

Overall then this has been a transformational period for the group. The profit from continuing operations did decline but if we add back in the pro-rata £2.2M profit from the associate that is included in the discontinued operations and discount the £2.3M bonuses given out following the sale of Everyday Loans (the profit of which was included in discontinued operations), the performance of the group improved year on year. Net assets also grew but the operating cash outflow worsened.

The two large transactions are clearly the defining moments of this period with the Everyday Loan sale netting £113.3M in profit and the Secure trust share sale gaining £100M. In addition, customer assets and deposits both increased. Unfortunately looming over these results is the Brexit vote and while Arbuthnot do seem better placed than other banks, their performance could still be affected and with a forward dividend yield of 2.1%, I am not sure the risks are fully priced in. I am waiting on the side lines for a bit more clarity.

On the 13th October the group released a trading update covering Q3. The overall lending pipeline has shown good growth, although the period of time between approval and drawdown of loans has marginally increased. The commercial bank continues to develop at a good rate. The disruption in the larger UK banks has led to a number of direct approaches from experienced bankers who are interested in joining the group. They have therefore accelerated their expansion plans and are taking on new premises in Manchester to cover the NW region.

The recent reduction in the base rate will result in a short term fall in net interest margin but the longer term impact of this may be reduced depending on where rates in the deposit market stabilise. The significant transactions carried out in the first half of the year which resulted in a profit of over £225M have now been included in the capital base of the group so the board are now proposing to pay a further special dividend of £3 per share, which equates to about £45M.

Overall the group is confident that it can continue to exploit the opportunities that currently exist in the financial services industry. This seems like a pretty steady update, although the lower base rate is a bit of a concern. I will keep watch on this share for now.

On the 19th December the group completed the purchase of a private baking loan portfolio which is mainly secured against residential property. The loans are being purchased from Duncan Lawrie Ltd and has customer balances of around £44.9M spread over 83 customer accounts. The average loan to value of the property was 43% and the client yield was 5.21% in October.

On the 20th December the group announced that it had reached an agreement to acquire Renaissance Asset Finance from its founders. The business is a provider of finance for a range of specialist assets which includes vintage and expensive cars and SME business assets. By the end of November customer assets were £68M and the net assets of the business were £1.6M.

Consideration will be paid in four staged amounts, all of which will be in cash with the first amount being paid on completion being equal to the net assets. The remaining amounts will be made annually based on the profitability of the business in each of the following three years. The maximum amount payable for the performance based payments is limited to no more than £6.5M. Both consideration and the refinancing of RAF’s funding liabilities (about £66M) will be satisfied from cash resources. Last year the business made a pre-tax profit of £2.4M but this included a one-off amount of £1.75M.

On the 23rd January the group announced that finance director James Cobb purchased 1,000 shares at a value of £15K. Not a huge purchase but nice to see nonetheless.

On the 21st February the group released a trading update for the year. They continued their development as expected in Q4 and therefore will report profits for the year in line with market expectations. As previously announced they completed the purchase of the Duncan Lawrie loan portfolio which has now been transferred.

In December they also announced that they had reached an agreement to acquire Renaissance Asset Finance which was subject to the approval of the change of control by the Regulation Authorities. One of these approvals has now been received but the completion still remains conditional on the final receipt which is expected to complete before the end of Q1 2017.