Creston has now released its final result for the year ended 2016.

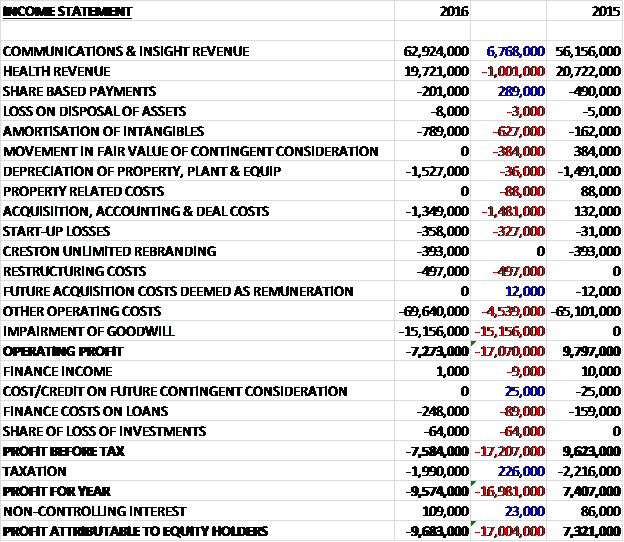

Revenues increased when compared to last year (although like for like revenue was broadly flat) as a £1M decline in Health revenue was more than offset by a £6.8M growth in communications and insight revenue. Share based payments declined by £289K but intangible amortisation grew by £627K, there was no £384K positive movement in the fair value of contingent consideration, acquisition costs were up £1.5M, start-up losses grew by £327K, there was £497K of restructuring costs and other operating costs increased by £4.5M. We then see a £15.2M impairment of goodwill to give an operating loss of £7.3M, a detrimental movement of £17.1M. Finance costs increased somewhat but this was offset by a decline in tax. The end result was a loss of £9.7M, a detrimental movement of £17M year on year.

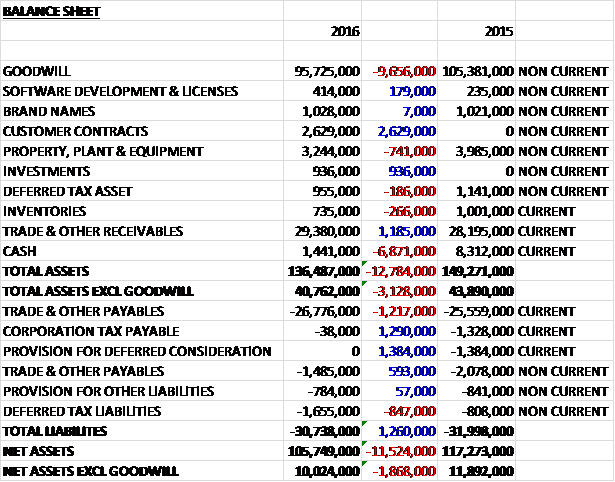

When compared to the end point of last year, total assets declined by £12.8M to £136.5M driven by a £9.7M decline in goodwill and a £6.9M fall in cash, partially offset by a £2.6M increase in the value of customer contracts, a £1.2M growth in receivables and a £936K increase in investments. Total liabilities also declined during the year as a £1.4M fall in the provision for deferred consideration and a £1.3M decline in corporation tax payable was partially offset by an £847K growth in deferred tax liabilities. The end result is that, excluding goodwill, the group had a net tangible asset level of £10M, a decline of £1.9M year on year.

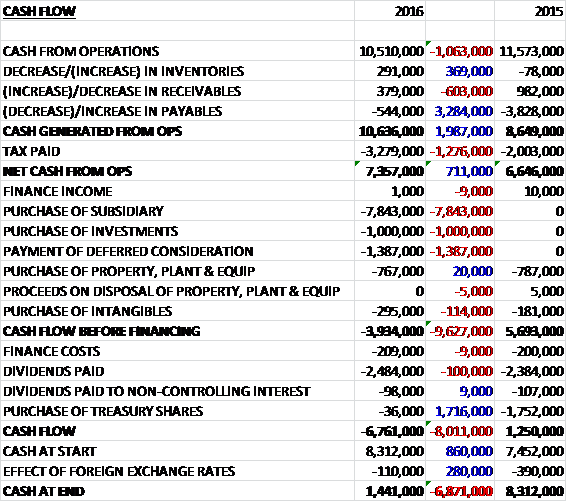

Before movements in working capital, cash profits declined by £1.1M to £10.5M. Working capital was broadly neutral compared to a cash outflow last year and after tax payments increased by £1.3M, the net cash from operations came in at £7.4M, a growth of £711K year on year. The group spent all of this on acquisitions, along with £1M on investments, £1.4M on deferred consideration, £767K on property, plant and equipment, and £295K on intangibles to give a cash outflow of £3.9M before financing. The group also spent £209K on finance costs and £2.5M on dividends it could not really afford to give a cash outflow of £6.8M for the year and a cash level of £1.4M at the year-end.

The headline PBIT in the Communications & Insight division was £9M, a growth of £883K year on year on revenues that increased by 12% overall and 2% on a like for like basis. This growth was driven by the acquisition of How Splendid, the good new business performance and the broadening of services to key clients with two of the top five customers experiencing double digit revenue growth. The top twenty client list saw three new entrants following the acquisition – SSE, Boots and the recent Costa win.

This positive underlying revenue trend has been affected by client budget reductions and volatility due to weaker trading for certain clients, especially in the retail and consumer tech sectors, and a more cautious economic outlook for others. The insight companies have particularly been affected by these factors as well as the changing market research industry, and this has led to the closure of the group’s Fieldwork operation and a more difficult trading performance.

The growth in profit was offset by the weakening Euro to the tune of £400K, and an increase in operating costs to services an expected higher level of revenue earlier in the year. Actions have been taken to ensure operating costs are aligned with the revised levels of future revenues and to maintain margin.

Significant new business wins during the period include work for new and existing clients; CRM and data strategy advisor to BA, the CRM strategy for the Vodafone Customer Value Marketing account, global lead digital strategic agency for Sony Mobile, the local marketing of Bosch Home and Garden and the CRM and digital strategy for Weetabix. After the year-end, wins include Sony PlayStation Europe and additional work with L’Oreal.

In December the group announced the creation of new brand partnership specialist, Affinity, which helps clients negotiate long-term partnerships with sporting and live entertainment events. Since launch the business has won clients including Rolls Royce and Ocean Masters World Championship. The group also launched Navigate, which is involved in marketing technology. In the context of an ever-changing landscape of data platforms, the business has been set up to advise brands on the optimal technology to automate data-driven consumer marketing experiences. It now works with group clients such as Danone, Nissan and Sony. Other investments in existing agencies during the year includes the launch of Real Data and Reflected Life, data analytic and digital marketing tools respectively.

The headline PBIT in the Health business was £4M, a decline of £355K when compared to last year. On a like for like constant currency basis, given the strengthening of the US dollar, the decline increased. Revenue was lower predominantly due to a weaker performance in the UK Health business, and more specifically in the health advertising agency. As a consequence of this and the growing change in market opportunities, the group combined DJM and PAN to launch DJM PAN Unlimited. Cost initiatives have been enacted which have included disbanding the health regional restructure which will realise £500K in annual savings.

Significant new business wins during the period include work for Astellas, Astra Zeneca, CDC, Gilead, National Meningitis Association, Novartis and Sanofi with post period wins including AbbVie, Janssen and Orthimo.

During the year the division created Search Unlimited, a digital marketing search engine optimisation agency. With founding clients Astra Zeneca, Abbvie and Novartis, this SEO specialist works to support clients in building their online profile.

In the US, in April 2015 the group announced a partnership with Propeller Communications and also began a partnership with global consumer trends and insight consultancy Future Foundation. The international growth has been further supported by the existing partnership with Serviceplan in Europe and in January 2016 they entered a new partnership with Ariadna to grow their South American services.

On the 22nd April the group acquired a 51% share in How Splendid Ltd for a total cash consideration of £8.9M, generating goodwill of £5.1M. There is the potential of a further additional consideration payment of up to £7M in June 2017 relating to the 51% shareholding based on profitability up to that date. This payment would be considered deemed remuneration so is off the balance sheet. Currently there is zero deferred consideration due to project delays impacting 2016 performance but this will be re-assessed in future reporting periods, although no further consideration for the 51% of the business is expected.

The fair value of the non-controlling interest is deemed to be nil on acquisition due to restrictions on the 49% shareholding which links the ownership of those shares to continuing employment for two years from the acquisition date. As such a share based payment charge will be recognised to value this liquidity foregone to build up a balance in equity with this converting to non-controlling interest provided the sellers are still in employment at the two-year anniversary date.

For the remaining share capital, there are no put options but the group will have the option to acquire a further 24% from April 2017 for a maximum value of up to £8.6M and the remaining 25% from April 2019 for a maximum value of up to £11.9M. This consideration, payable on cash will depend on the average profit for the year in which the call option is exercised along with the two years prior. During the year the business contributed profit of £1.5M.

In June 2015 the group made an investment in 18 Feet and Rising, a London-based advertising agency for a consideration of £1M. The group acquired a 27% shareholding and in the period since the acquisition, a loss of £64K was recognised from the business.

As usual there are a load of non-underlying costs. Acquisition, accounting and deal related costs amounted to £1.3M comprising acquisition costs of £200K for Splendid United and 18 Feet; £700K of amortisation costs relating to the Splendid acquisition; and share-based payments of £300K in relation to Splendid for valuation of liquidity foregone for the non-controlling interest. In relation to the acquisition of DJM and Cooney Waters, £100K has been recognised as acquisition payments to employees deemed as remuneration.

Start-up related net losses of £400K have also been flagged up. This represents the net losses of five start-ups, being Reflected Life, Real Data, Affinity, Navigate and Search. Restructuring and closure related costs of £500K have been incurred in relation to the reorganisation of UK Health regional board, the combination of DJM and PAN to form DJM PAN and the closure of FieldworkUK.com.

A goodwill impairment charge of £10.7M was recognised against ICM Unlimited. This included £2M as a result of the closure of FieldworkUK.com with the rest due to a more conservative estimate of future operating profit growth rates following a poor performance in 2016. There is still £8.7M of goodwill against the business. The group also recognised a goodwill impairment charge of £4.5M against DJM PAN Unlimited due to a more conservative estimate of future operating profit growth following the business combination.

Richard Huntingford stepped down from the board as non-executive chairman and Nigel Lingwood is activing as Chairman on an interim basis. In February, Iain Ferguson joined the board as a non-executive director representing the company’s largest shareholder, DBAY Advisors.

The board remains confident that the group is well placed to deliver long term growth to shareholders on the basis of its strengthened offer, blue chip client relationships and positive cash position at the year-end.

At the current share price the shares are trading on a PE9.7 which falls to 7.6 on next year’s consensus forecast. After a 5% increase in the total dividend, the shares are yielding 4.8% which remains flat on next year’s forecast. At the year-end the group had a net cash position of £1.4M compared to £6.9M at the end of the prior year.

Overall then this has been a bit of a mixed year for the group. Excluding impairments, profits declined due to various acquisition costs, start-up costs and restructuring expenses, apart from these they were modestly up. Net assets declined and although the operating cash flow improved, this was due to a smaller fall in payables than last year and cash profits fell with no free cash being generated after acquisitions.

The communications & Insight division saw profits increase due to the How Splendid acquisition but the Health business saw a reduction in profits driven by difficult conditions for the UK Health advertising agency. The How Splendid acquisition looks a bit complex and expensive but it seems that a poor performance means that no further contingent consideration is expected on the bit they already own, although the future call options look potentially costly.

Offsetting the issues is a seemingly cheap valuation with a forward PE of 7.6 and yield of 4.8% probably pricing in a fair amount of pain. Overall though this does not strike me as a great investment at the moment, especially after the recent Brexit vote.

On the 6th September the group released an update covering the first four months of the year. They are trading broadly in line with expectations. The recent Brexit vote continues to cause some variability and uncertainty in budgets amongst the group’s UK clients but the subsequent movements in existing clients’ marketing budgets have largely been offset by the benefit of new business gains and during the period there has been marginal growth in revenue.

Headline pre-tax profit is well ahead of the same period last year, reflecting the benefit from the ongoing implementation of operational efficiencies started in the prior year, and some benefit from the weakening in Sterling. Overall this looks tentatively OK and I feel these look rather good value now so have taken a small position.

On the 17th November the group announced they had reached an agreement with largest shareholder DBAY regarding the terms of a cash offer for the group. Each shareholder will receive 126.42p per share, representing a 35% premium to the closing price of the shares the day before. This looks rather opportunistic to me and I would not be that happy if I was a long term shareholder but this represents a decent return for my recent purchase!