International Greetings has now released their interim results for the year ending 2018.

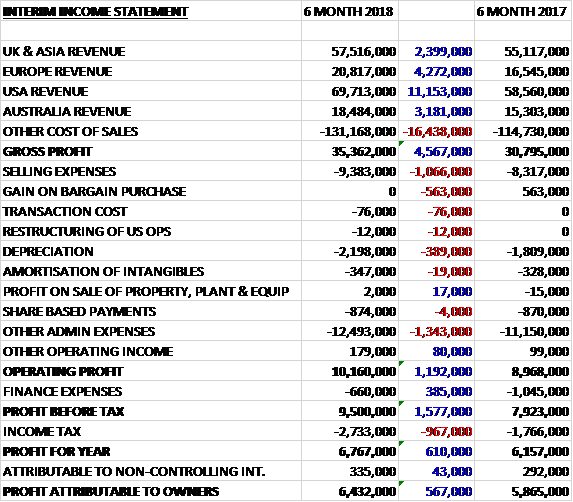

Revenues increased when compared to the first half of last year with an £11.2M increase in US revenue, a £4.3M growth in European revenue, a £3.2M increase in Australian revenue and a £2.4M growth in UK and Asian revenue. Cost of sales also increased to give a gross profit £4.6M higher. Selling expenses were up £1.1M, there was no gain on bargain purchase, which was £563K last time, depreciation was up £389K and other admin expenses grew by £1.3M to give a £1.2M increase in operating profit. Finance expenses reduced by £385K but tax charges grew by £967K which meant that the profit for the period was £6.4M, a growth of £567K year on year.

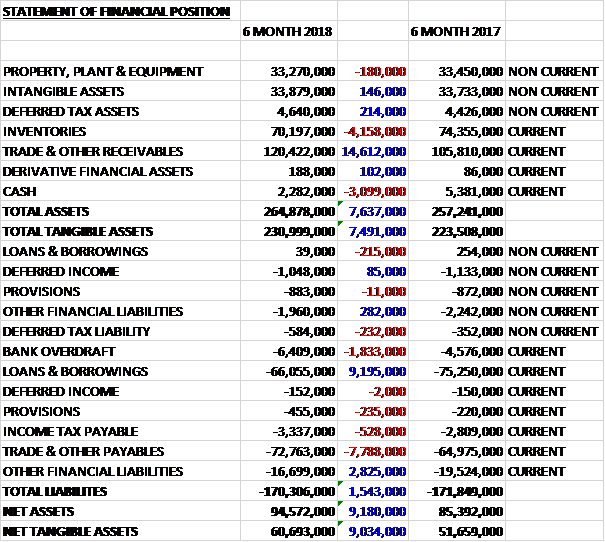

When compared to the end point of last year, total assets increased by £7.6M, driven by a £14.6M growth in receivables, partially offset by a £4.2M decline in inventories and a £3.1M decrease in cash. Total liabilities declined in the period as a £7.8M increase in payables and a £1.8M growth in the overdraft were more than offset by a £9M decline in borrowings and a £3.1M fall in other financial liabilities, mainly relating to finance leases. The end result was a net tangible asset level of £60.7M, a growth of £9M year on year.

Before movements in working capital, cash profits increased by £2.7M to £13.5M. There was a big cash outflow from working capital so after tax payments increased by £976K there was a net cash outflow of £66.8M from operations, an increase of £10.9M year on year. The group spent £462K on intangible assets and £3.4M on property, plant and equipment so before financing there was a £70.6M outflow of cash. The group spent £2.3M on dividends and took out £66.3M of loans to give a cash outflow of £6.7M for the period and a cash level of £4.1M at the period-end.

The profit in UK and Asia was £4M, flat year on year reflecting the initial impact of the integration of the three UK operating businesses. The new manufacturing equipment producing retailer branded bags to be given to consumers is now fully operational having been installed on time and on budget.

The profit in Europe was £1.7M, a growth of £426K when compared to the first half of last year. A second high speed printing press is on track for delivery and on budget for installation early in 2018. A strong order book is in place for the rest of the year.

The profit in the US was £5.1M, an increase of £1.4M when compared to the first half of 2017 which includes organic growth of 27%, some favourable timing differences and the successful integration of Lang. The planned investment to upgrade the IUT systems in the US is proceeding on time and on budget and is due for installation in 2019.

The profit in Australia was £1.2M, a growth of £207K year on year, driven by the robust independents channel.

In September the group agreed to acquire Biscay Greetings with completion taking place in January 2018. The business is a greetings card and paper products business based in Australia. The acquisition will be satisfied by a cash consideration of £5.5M, generating intangible assets and goodwill of £2.4M. The business will also require a working capital injection of £1.8M.

If growth is heavily fuelled by the US business, as is the expectation, the blended tax rate could continue to rise and cash tax is increasingly becoming payable at the prevailing rate in most geographical regions as historical losses are fully utilised, although this will not be evident in the US or the UK until 2019.

Capital expenditure was £800K higher in the period as the group seeks out opportunities to invest in efficiency. They have taken delivery of new machinery in Wales to manufacture retail branded bags as part of a diversification into new adjacent product categories. The equipment was fully operational at the period-end with a strong order book in place. Orders have also been confirmed for second HD high speed printing pressing press in Europe and to implement a new ERP system in the US, both of which are expected to yield attractive paybacks.

As previously announced, Anthony Lawrinson indicated his intention to retire from his role as CFO for family reasons after six years at the group. The board intends to appoint Giles Willits as new CFO from January. Giles, aged 51, was most recently CFO of Entertainment One.

Going forward, the strong trading position at the end of the first half of the year is firmly underpinning management’s expectations for the full year.

At the period-end the group had a net debt position of £70.2M compared to £76.4M at the same point of last year. At the current share price the shares are trading on a PE ratio of 31.8 which falls to 19.3 on the full year consensus forecast. After an increase in the interim dividend the shares are yielding 1.1% which increases to 1.3% on the full year forecast.

On the 29th November the group announced that non-executive director Mark Tentori purchased 7,404 shares at a value of £30K. This is his first share purchase.

On the 16th January the group released an update covering Q3 which covers the Christmas trading period. Trading has continued to be strong. The group expects to deliver record revenues this year with the continued expansion of their global footprint outside the UK. All regions are on track to deliver year on year profit growth which means that EPS is expected to be ahead of current market expectations and delivering strong year on year growth. The board continue to see strong cash conversion across the group and expect average leverage for 2018 to be significantly below an average of two times.

Additionally as a result of the level of the group’s US earnings the board expects to benefit in 2019 and beyond from the recent US tax legislation changes. The US tax rate change is expected to translate into lower tax payments, thereby enhancing cash generation.

Overall then this has been a good period for the group. Profits increased, net assets grew and cash profits increased, although the operating cash outflow widened which is usually the case due to the timing of Christmas after the first half ends. Going forward, all regions are experiencing growth and the important Christmas period has gone well. This is probably factored into the share price, however, with a forward PE of 19.3 and yield of 1.3%. All in all, however, I remain a holder.