Serabi Gold has now released its Q3 results for the year ending 2015.

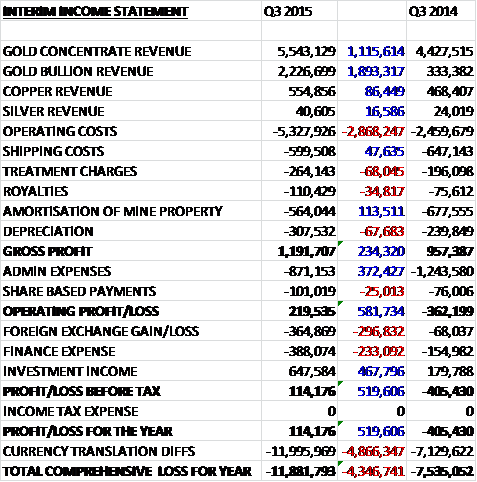

Revenues increased when compared to Q3 last year due to increased sales of all products, particularly a $1.9M growth in gold bullion revenue. Operating expenses also increased, partially due to the group’s decision to revise the basis on which it calculates the value of inventories to give a gross profit some $234K above that of last time. Admin expenses actually fell, mainly as a result of the depreciation of the Brazilian Real, so that the operating profit was $220K, a positive swing of $582K. We then see a greater foreign exchange loss and a higher finance expense relating to interest paid on the Sprott loan partially offset by an increase in investment income due to a reduction in the value of the warranties so that, after no tax was paid, the profit for the quarter came in at $114K, a positive swing of $520K compared to Q3 2014.

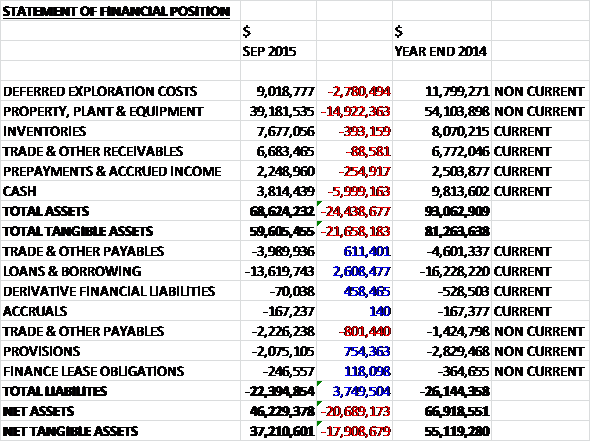

When compared to the end point of last year, total assets declined by $21.7M driven by a $14.9M fall in property, plant and equipment, and a $2.8M decrease in deferred exploration costs, both as a result of the depreciation of the Brazilian Real. Cash also declined during the nine month period, down by $6M. Total liabilities also fell during the period, mainly as a result of a $2.6M decrease in borrowings as the group paid back some of the Sprott loan and a $754K fall in provisions due to the weakness in the Brazilian currency. The end result is a net tangible asset level of $37.2M, a decline of $17.9M over the last nine months.

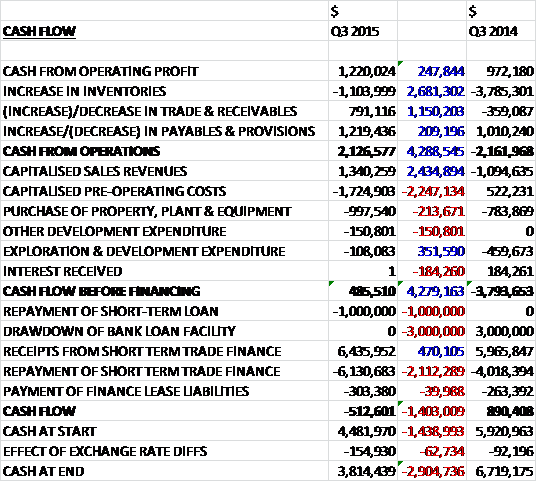

Before movements in working capital, cash profits increased by $248K to $1.2M. An increase in inventories broadly offset an increase in payables but a fall in receivables meant that the cash inflow from operations was $2.1M, a positive movement of $4.3M when compared to Q3 2014, mainly as a result of a lower growth in inventories. There was a net $400K cash outflow from capitalised mining operations so operating cash flow was $1.7M really. The group then spent nearly $1M on property, plant & equipment, $151K on other development expenditure and $108K on exploration and development. After finance lease costs, the free cash inflow was $182K so the company was cash generative. This did not cover the $1M loan repayment, however, so that there was a cash outflow of $513K in the quarter to give a cash level of $3.8M at the period-end.

The operating loss in Brazil was $3.4M compared to a profit of $480K in the same quarter of 2014 and the operating profit in the UK was $3.6M compared to a loss of $842K in Q3 last year.

The Palito mine has now reached a relatively steady operational state with mining activities in a balanced cycle of development and production that is expected to generate approximately 105,000 tonnes of ore at between 8.5g/t to 9g/t of gold during 2015. Production during the first nine months of the year has been 24,704 ounces. Q3 has seen increases in the volume of Sao Chico ore being processed at the Palito plant rising from 4,134 tonnes at the end of Q2 to a total of 10,306 tonnes at the end of September with average feed grades improving from 6.68g/t to 7.12g/t for the nine months and an average of 7.41g/t in the quarter.

Conversely the amount of ore mined from Palito declined by 6% when compared to the Q3 last year which reflected the fact that in this quarter last year, it was the first significant quarter of ore production from stopes. The Palito mine up until the end of Q2 2014 had been in development had with stopes being prepared for production. Q3 therefore saw the benefit of this nine month development period in an exceptionally high level of ore production. By comparison, ore production in Q4 2014 reduced to 25,308 tonnes. Long term planned ore production rates from Palito is expected to average around 90,000 to 100,000 tonnes a year so equates to 22,500 to 25,000 tonnes per quarter so with a figure of 30,454 tonnes this quarter, we can expect this to decline going forward.

During the quarter the group received an average price of $1,122 per ounce of gold compared to $1,199 in the same quarter of last year and $1,162 in Q2 of this year. The all-in sustaining cost of production is $756 per ounce with a cash cost of production of $580 per ounce. During the quarter the group produced 9,078 ounces of gold compared to 8,237 ounces in Q2 and 7,389 ounces in Q1.

The better than forecast mining performance at Palito has resulted in the surface ore stockpiles not being run down as quickly as management forecasted and by the end of September the surface stockpile of Palito ore was measured at approximately 10,600 tonnes with an estimated average grade of 3.63g/t of gold. At the same time in 2014, the stockpile of ore from the Palito mine was estimated at approximately 20,000 tonnes with a grade of 7g/t. During the first half of 2015, the group was able to draw on the higher grade portion of the stockpile to make full use of the processing capability of the Palito gold plant but as the group has, from Q2, achieved increasing rates of ore production from Sao Chico, the level of stockpiled material has started to increase again and also contains 4,000 tonnes of Sao Chico stockpiled ore at an average grade of 3.77g/t.

The gold production generated from this mined ore is to a limited extent being supplemented during the year by surface stockpiles of ROM ore and flotation tailings generated last year. The surface ROM ore stock is carryover or remains of the ore mined in 2013, when the mine started generating ore twelve months before the plant began operating. The 2014 flotation tails are a result of the plant not having the Carbon in Pulp recovery circuit operational until October 2014. Tailings produced from the flotation process were stockpiled during this year, but there has been limited plant capacity to process these stockpiles due to increasing levels of ore beginning to be generated from the Sao Chico mine as well as higher than planned volumes of low grade development ore being processed at Palito.

The group has undertaken further ramp development, and has now reached and is developing on the 19m relative level, but significant focus is now being given to accessing and developing drilled, parallel vein structures on production levels above the 24m RL. These include the Chico da Santa zone which lies to the north of the primary G1, G2 and G3 veins and the Senna zone which is located to the south of the Palito West vein complex and which during 2008 and 2009 produced oxide material in excess of 3g/t. The cross cut to the Chico da Santa zone was completed in October 2015 whilst it is expected that the cross cut to the Senna zone will be completed by the end of November. The opening up of these new sectors will allow the group to establish more ore faces and in time production areas especially on the upper levels in these zones.

In the case of the Senna zone there has never been any previous underground development of the ore zones. Based on the ore grades recovered from the past limited open pit operation, management is hopeful of the potential within the zone. At the Senna zone the group has recorded a drill intersection of 0.55 metres at a grade of 50.99g/t at approximately 300 metres below the surface. Previous exploration activity at Senna highlighted up to four mineralised zones, with structural continuity for three zones of up to 900 metres in strike length and 300 metres vertical depth, of which the most prominent zone was confirmed on surface by trenches for over 600 metres.

Last year the group continued mine development on G3 towards the Palito South area. This development is primarily on the 114m RL, which has been driven some 700 metres further south than any other underground working at Palito. Having intersected numerous high-grade pay shoots, the group is testing the down-dip continuity of these pay shoots for future development of the mine at depth, as well as incorporating into its future mine plans the up-dip extensions of these pay shoots in the upper levels. These are as yet undeveloped and represent an excellent potential source of additional ore.

In light of the higher levels of ore production being achieved at Palito and an expectation of ore volumes at Sao Chico also being higher than initially envisaged, the group has acquired an additional ball mill and is planning further capacity improvements with the Palito gold process plant that will increase the current throughput rates from 400 tonnes per day to at least 500tpd. These improvements, whilst increasing gold production potential, are also intended to create excess plant capacity that will allow the group to catch up lost production caused by unplanned stoppages. These improvements include the installation of an additional flotation cell, an additional leaching tank and new screens within the CIP tanks to improve inter-tank flow rates. These upgrades are expected to be completed by early in Q2 2016 at a cost of about $1.2M which will be funded from operational cash flows.

At Sao Chico, Q4 2014 saw the underground development commence. By the end of Q3 2015, almost 2,000 metres of development had been achieved with three levels now in development and a fourth expected to be reached shortly. During the remainder of 2015 and into 2016, the main vein will continue to be developed and evaluated with the continuation of on-lode development, surface and underground drilling. The development of the main ramp which is being driven at a 12% gradient is continuing, with access to the next level at 156m RL planned to be completed in November 2015.

The immediate priority is to evaluate and define stoping blocks on these first four levels to secure mine production for the next year and a half. Further ramp development will therefore be progressed to pursue the down-dip extension of the current areas that are in development. The rates of lateral development on existing levels will be increased when the company, through a combination of its current surface and underground drilling programmes and on-lode development, has greater confidence in the distribution of the high grade ore mineralisation within the lateral strike extensions.

The high grade mineralisation is dominantly hosted in a consistent alteration zone that can be anything from two to ten metres wide. The alteration zone itself is readily identifiable, however, the high grade gold zones within this alteration zone are much less so, and as a result the mining operations will require on-lode development at regular vertical intervals, with regular channel sampling and in-fill drilling between these levels to best define the high grade mineralisation. This approach will allow the group’s mining personnel to readily identify stoping blocks and optimise mining the high gold grade zones.

The group is continuing to progress the conversion of the exploration license at Sao Chico to a mining license. As the next major step in the conversion procedure, Serabi submitted, in September, the Plano Approvimiento Economico, a form of economic assessment prepared in accordance with Brazilian legislation. All mining operations can continue in parallel under the trial mining license, however and a submission for a further extension of the trial license for one extra year was submitted in September, which will hopefully be completed soon as the current one expires in mid-November. The issuing of the mining license also required the submission of a risk assessment and management plan, safety assessments, environmental and social impact studies, closure and remediation plans which have either been submitted or are in the process of being finalised, in preparation for submission to the relevant government bodies.

The Sao Chico mine, whilst contributing to the group’s gold production during the year, will be primarily in development and is not expected to achieve full production until 2016. A drilling programme is taking place during 2015 which will help the understanding of the ore body and facilitate the mine planning for 2016. Over 6,000 metres of surface drilling has been completed and the programme has been extended beyond its original planned 5,000 metres level to allow the group to undertake closer spaced in-fill drilling. The surface programme is being complemented by drilling being undertaken from within the existing underground developments. The drilling programme which has built on the results and understanding gained from the previous drilling campaigns has continued to report numerous high grade intersections with gold grades in excess of 100g/t and indications that the grade and resource potential continues at depth.

The group is currently forecasting gold production for 2015 of approximately 33,000 ounces with all-in sustaining cost expected to be about $900 per ounce.

As well as the potential that exists to grow resources at Sao Chico, the Palito South, Currutela and Piaui prospects still provide excellent opportunities for identifying additional resources which could both enhance current production levels as well as extend the mine life. With the exception of the current surface drilling programme being undertaken at Sao Chico, no drilling or other exploration activity is currently planned on the group’s properties. Once adequate cash flow is being generated the group will step up its exploration activity and will be looking to add to its resource base and production potential by establishing additional satellite high-grade gold mines in relatively close proximity to Palito which will be the centralised processing facility. Management will continue to evaluate other opportunities within Brazil that it considers could increase the resource base and longer term production potential of the group.

Total volumes processed of both Palito and Sao Chico ore during the first nine months of the year were 96,480 tonnes which was equivalent to 355 tonnes per day. Milling performance at the start of Q1 was affected by power stoppages resulting from an inconsistent electricity supply. The reliability of the power supplied by CELPA has remained subject to fluctuation and interruption which is particularly detrimental to the performance of the gold processing plant. As a consequence, during Q2, the group took the decision to commit to the use of diesel generated power for the operation of the plant. Management expects that the benefits of increased plant availability will significantly outweigh the increased operational costs. The power requirements of mining operations together with the day to day needs of the mine site, camp and other operations continue to be met by power supplied by CELPA except in exceptional circumstances.

During the period the group installed an ILR which will be commissioned in November, this will allow the milled Sao Chico ore to be passed initially through a gravity concentrator with the recovered gravity concentrate containing “free gold” passing through the ILR where in a small closed circuit it is leached with high concentrations of cyanide, dissolving the gold. This gold in solution is then recovered by conventional electro-winning and smelting. This process will enhance gold recovery for the Sao Chico ore and help improve efficiencies in the CIP plant.

The Palito mine achieved commercial production in July 2014. In Q3 2014, the group completed work and commissioned the Carbon in Pulp leaching circuit allowing them to maximise the potential recovery of gold from the ore processed. The first gold pour from the CIP operations took place in October 2014. During the first nine months of this year the group has been undertaking the initial development of its Sao Chico operation and for the remainder of the year plans to steadily increase the production of ore from Sao Chico using the Palito gold processing plant. They began processing ore from Sao Chico during April.

The group started a surface drill programme in March which is ongoing. The drilling campaign is a combination of in-fill and step-out drilling and the results from this, in conjunction with the on-lode development mining that will take place in the remainder of 2015 will help the understanding of the ore body and facilitate mine planning for 2016. The group has not engaged in any exploration activity at the Sucuba or Pizon projects during the past year and has currently not budgeted for any during the next year and a half.

Last year the group entered into an $8M secured loan facility which is required to be paid in full before the end of March 2016 with the Sprott Resource Lending Partnership providing additional working and development capital. The first tranche of $3M of this facility was drawn down in September 2014 with the remaining tranches drawn down in full in December. This loan attracts a hefty interest rate of 10% and to date the group have paid back $3M of this loan. They also have a borrowing facility of $7.5M to provide advance payment on sales of gold and copper concentrate which currently extends only to the end of 2015.

The directors anticipate that the group now has access to sufficient funding for its immediate projected need and they expect to have sufficient cash flow from the current forecasted production to finance the ongoing operational requirements and, at least in part, fund exploration and development activity at the other gold properties. However, the forecasted cash flow projections for the next year include a significant contribution arising from the Sao Chico development where commercial production has yet to be declared. There are obviously risks involved with the start of any new mining operation giving rise to the possibility that additional working capital may be required to fund any delays or additional capital requirements. Should additional working capital be required, the directors consider that further sources of finance could be secured within the required timescale.

Obviously the group’s performance is linked to the price of gold and with the continued strength of the US dollar, it is hard to see the gold price increasing by that much in the near term. Other risks are mainly related to operating within Brazil with the government still looking to introduce a new mining code, and the fact that the group still does not have a proper mining license at Sao Chico.

It is worth noting that there are 100M outstanding warrants which expire in March 2016 but because they are denominated in US dollars and not Sterling, they are not considered an equity item and are included under group liabilities. After the period-end, the Brazilian Real has shown some stability after declining by about 60% against the US dollar over the past year. The majority of the group’s operating costs are made in Reals so any changes affect the cost base along with the value of the assets and liabilities.

Overall then, this has been a fairly steady quarter for the group. Profits increased, and they now seem to be at least breaking even at the current gold price. Net assets did decline, due to the depreciation of the Brazilian Real, but operating cash flow increased and the group even managed to generate some free cash, although this was not enough to cover the loan repayment. Palito has is now producing steadily and the reduction quarter on quarter was due to exceptionally strong production in Q3 last year and will probably settle down a bit lower. At Sao Palito, those very high grade areas of ore seem to be quite difficult to identify but both the amount of ore mined and the grade increased in the quarter, although the mine is not yet in commercial production.

The sale price of $1,122 per ounce seems fairly steady and is above the cost of $756 achieved during the period and the $900 per ounce expected for the year as a whole. Operationally, the ball mill will undergo an upgrade which should increase capacity to mine some of those tailings that seem to be building up. I am a little concerned about the trial mining license, which expires this month and the seeming lack of progress in obtaining a full mining license so would like to see this resolved, and there are obviously operational risks in bringing Sao Chico up to commercial development. Overall though I like the progress being made here and may look to buy some shares when the above issues are clearer.

On the 31st December the group announced that its controlling shareholder, Fratelli Investments, has provided a short term working capital convertible loan facility of $5M for additional working capital facilities. The group is facing strong economic headwinds at a time whilst they have continuing commitments for increasing throughput through the process plant as well as development expenditure to bring the Sao Chico mine into full production. This has restricted the company’s ability to build up cash reserves and to ensure they remain on track, they have had to find external sources of funding.

The loan expires at the end of January 2015 and may be drawn down in three tranches. It has an interest rate of 12% per annum but there is no prepayment penalty or arrangement fee. This is in addition to the secured loan facility arrangement with Sprott which has an outstanding balance of $4M.

The first $2M of the loan is convertible at the election of Fratelli into new Serabi shares at an exercise price of 3.6p (the share price is now 2.8p so this actually seems very fair to me). The remaining amount of the loan if drawn down may be repaid by the company at its option on or before the end of June this year, otherwise Fratelli will have the right to convert it into new shares, also at 3.6p.

Clearly the company is under considerable financial distress which doesn’t really make the shares a good investment at the moment in my book but they are in a fortunate positon in that their controlling shareholder can provide them with short term funding at terms which are not actually that bad. If they had to do a placing to get the cash, things could have been a lot worse.

On the 6th January, the group announced that they had drawn down the initial $2M.

On the 1st February the group released an operational update covering Q4 2015. In the quarter they recorded 7,924 ounces of gold production and although this did not exceed the 9,078 ounces recorded in Q3 or indeed the 8,237 ounces in Q2, December was the best months of the year with 3,200 ounces of gold produced from a milled grade of 9.5g/t of gold. With this trend continuing, there should be a good start to 2016 and production for January is looking to be a further improvement on the December figure. The plant expansion and improvements are planned to be mostly completed by early in Q2 which should mean a further increase in levels of gold production in 2016. As a result, the production guidance for 2016 should be about 37,000 ounces.

The Palito mine has continued to perform consistently with mined grades and tonnages at the forecast level. The operation has now maintained a mined grade of just below 10g/t for much of the past two years. The group have been expanding the mine with some lateral development and two new areas in the mine have now been opened up by cross-cutting to the Senna and Chico da Santa sectors. Veins have been intersected by both sectors with encouraging mineable grades to date. Ore development is ongoing and these two new sectors will provide greater operational flexibility and additional ore sources to the well-established deeper Palito Main Zone and Palito West sectors.

The final quarter also saw the start-up of underground diamond drilling at Palito and the group are now evaluating numerous known but underexplored veins. Currently this evaluation is mostly being undertaken in the upper levels where these veins have been side lined awaiting drilling for the past two years. The board are confident this drilling will provide abundant ore sources in the next two years with the advantage of close proximity to existing infrastructure and not requiring any new ramp development.

At Sao Chico, ore development is now ongoing on a number of levels, most notably at 186mRL and 156mRL, and about to commence on 171mRL and 141mRL. The mine experienced a blip in gold production in October and November which adversely affected Q4 gold production. This was mainly due to power generation problems which delayed all mining activities. The shortfall in the high grade Sao Chico development ore feed was replaced by surface stockpiled ore from Palito which has a lower grade.

By December the problems were resolved and the mine delivered its best month of the year with over 4,000 tonnes mined at grades in excess of 12g/t. This improvement coincided with the commissioning of the Gravity/ILR circuit in the plant in late November where the group are now seeing gold recoveries from gravity concentration exceed 30%, bringing substantial benefits to the efficiency of the rest of the plant.

In the Sao Chico mine itself, the group are continuing to concentrate on the Main Vein. This is a 1.5m to 4m wide alteration zone which is structurally continuous but the gold grades within the zone are not as continuous and are hosted in four steeply plunging “pay shoots”. In these pay shoots the grades are often spectacular, often being in excess of 100g/t. Outside the pay shorts the vein is continuous but with low grade. As a result, as the mine development passes between pay shoots, lower grade ore has to be mined. The central pay shoot is the most established of the four and is some 100m long. The group are focusing the mine development plan for 2016 on this part of the main vein and are now enjoying some consistent higher grade development as a result.

The production improvements in the mine and the plant have met the targets established by the board and have allowed the company to take the decision to declare commercial production effective from the start of 2016.

As reported previously, the plant is being further expanded to allow the processing of significant surface ore stockpiles. The operation has been mill limited since the start of operations and the installation of the third ball mill, along with some improvements in the flotation and cyanidation plant will see their daily throughput increase from the current levels of between 350 and 400 tonnes per day. It is anticipated that they could average over 500 tonnes per day once the improvements are complete but the improvements will also create surplus capacity to catch up any lost production caused by unplanned stoppages.

The surface diamond drilling programme at Sao Chico was stopped shortly before the end of 2015. Whilst the programme was designed initially to explore the Sao Chico main vein to the east and west with step out holes, it soon became clear that more infill drilling was required. The programme and the deployment of the drill rigs was re-prioritised as a result but before completing the programme, three holes targeting the 50mRL level were drilled, some 100 metres below the deepest development level today, returning some very encouraging results.

The total gold production for the year was 32,629 ounces from the treatment of 130,300 tonnes of milled ore at an average grade of 8.43g/t and from cyanidation of 18,355 tonnes of stockpiled flotation tails grading at 2.66g/t. At the year-end the company still had a stockpile of about 36,000 tonnes of flotation tails at an average grade of 2.5g/t, which were recovered from 2014 plant production. They will continue processing this material when possible but until the completion of the plant expansion, currently scheduled for April, available plant capacity for processing these tailings is limited.

During the quarter Palito achieved about 2,000 metres of horizontal development, of which about half was ore development. For the whole of 2016, the mine has completed 6,800 metres of horizontal development and a further 792 metres of raises. At the Sao Chico mine, a total of 728 metres of horizontal development was achieved, 230 metres being ore development and 340 metres completed in the deepening of the ramp and cross cuts to development levels. About 2,800 of horizontal development has now been achieved for the year.

Of the 37,000 ounces of gold forecasted to be produced in 2016, 28,000 should come from the processing of Palito ROM and the Palito stockpiles and with the Sao Chico mine now under development, 9,000 ounces of gold should be produced from there. Overall in Q4, 34,848 tonnes or ore was milled at a grade of 7.55g/t to produce 7,925 ounces of gold. This represents the lowest grade from the year with the largest tonnage of ore to create the third highest quarterly total of gold.

The company announced that it had agreed an extended repayment period for the remainder of the loan with Sprott, the outstanding balance of which amounted to $4M and was due to be repaid by the end of March this year. The company has now agreed that the balance of the loan will be repaid in nine equal monthly instalments starting at the end of April. The interest rate remains at 10% per annum but the company has granted a call option over 2,500 ounces of gold at a strike price of $1,125 per ounce with Sprott having the right to exercise the option at any time up to the end of June 2017. The call option will be settled in cash.

Overall then, this is a pretty decent update. The figures for Q4 were actually rather disappointing with low grades and an associated low amount of gold produced. These issues were due to power generation problems at Sao Chico but they were resolved by December and Q1 2016 looks to be a pretty good period. The Sprott loan has been extended which suggests cash levels are a little tight but it is a positive move to have the repayments spread over a longer period of time.

A tricky one this – if gold prices hold up OK then this could be a pretty good investment at these levels in my opinion and in total contrast to the shambles at Aureus.