Avon Rubber has now released their final results for the year ended 2018.

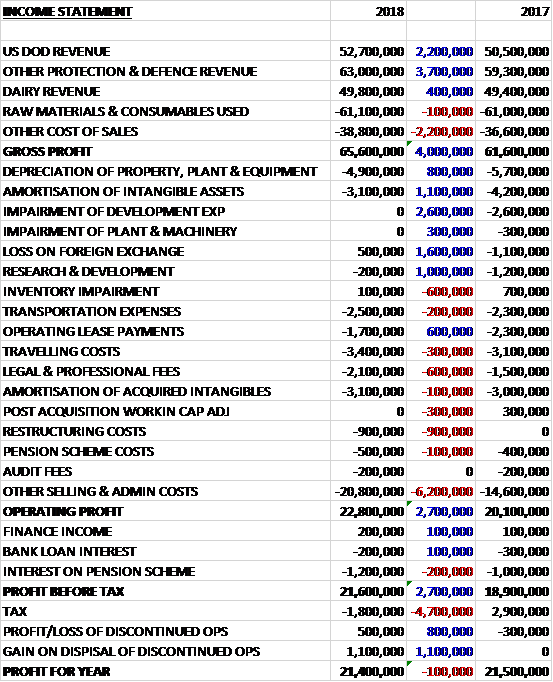

Revenues increased when compared to last year due to a £2.2M increase in US DOD revenue, a £3.7M growth in other protection and defence revenue and a £400K rise in dairy revenues. Cost of sales also increased to give a gross profit 4M higher. Depreciation was down £800K and underlying amortisation fell by £1.1M. There was also a £1.6M positive swing to a forex gain and a £1M decline in R&D expenditure along with a lack of impairments, which accounted for £2.9M last year. There was, however, £900K of restructuring costs and a £6.2M increase in other selling and admin costs to give an operating profit that was £2.7M higher. There was a £4.7M increase in tax charges which meant that the continuing profit for the year was £19.8M, a decrease of £2M year on year.

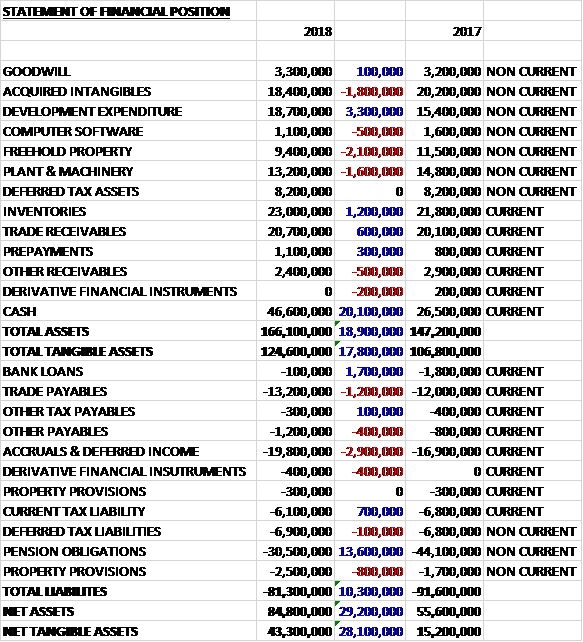

When compared to the end point of last year, total assets increased by £18.9M driven by a £20.1M growth in cash, a £3.3M increase in development expenditure and a £1.2M growth in inventories partially offset by a £2.1M decline in freehold property, a £1.8M decrease in acquired intangibles and a £1.6M fall in plant and machinery. Total liabilities declined during the year as a £2.9M growth in accruals and deferred income and a £1.2M increase in trade payables was more than offset by a £13.6M decrease in pension obligations and a £1.7M decline in bank loans. The end result was a net tangible asset level of £43.3M, a growth of £28.1M year on year.

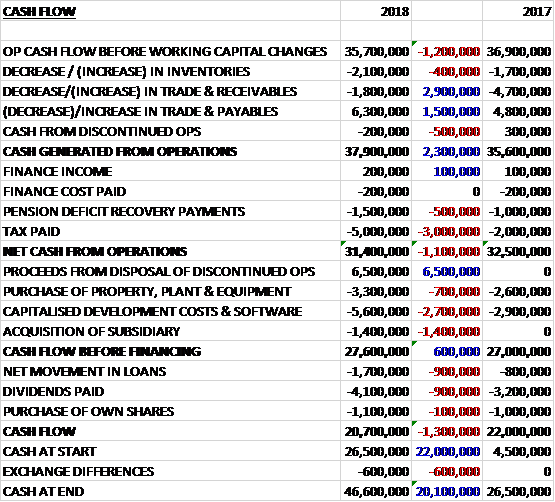

Before movements in working capital, cash profits declined by £1.2M to £35.7M. There was a cash inflow from working capital but pension deficit payments increased by £500K and there was a £3M increase in tax payments to give a net cash from operations of £31.4M, a decline of £1.1M year on year. The group received £6.5M in consideration for the disposal but spent £1.4M on acquisitions, £3.3M on fixed assets and £5.6M on development costs and software which meant that there was a free cash flow of £27.6M. This easily covered the £4.1M of dividend payments along with £1.1M of share purchases and £1.7M of loan repayments which gave a cash flow of £20.7M and a cash level of £46.6M at the year-end.

The operating profit in the Protection division was £19.5M, a growth of £3.3M year on year, although £2M of this increase was due to last year’s impairment costs. Revenues grew by 10% at constant currency with military up 8%, a 28% growth in law enforcement and a 10% decline in fire.

DOD revenue grew by £2.2M reflecting higher M50 mask system volumes and increased volumes of spares and accessories more than offsetting unfavourable currency movements. DOD spares and development costs revenue decreased by £3.6M due to last year including higher development costs relating to the M69 air crew mask. Having received orders for 219,000 M50 mask systems during the year, they entered the new financial year with an order book of 89,000. Revenue from their ROW military business declined by £300K as initial revenue from sales of their powered and supplied air range and the MCM100 underwater rebreather largely offset the non-repeat revenue last year from the 37,000 FM50 general purpose marks delivery.

The increase in law enforcement revenue was driven by strong performances in hoods and mask systems across all regions as they continue to make progress in converting police forces to their products. In North America, they also benefited from increased sales of filters and spares to their expanding customer base. Initial sales of their supplied and powered air ranges also contributed to the growth in the year and their expanded product range provides a foundation for future growth.

The decline in Fire revenue was due to tougher market conditions in North America as customers delayed purchasing on older legacy ranges in advance of the new 2019 compliant products. The NFPA approval of Magnum later in the year will offer greater opportunity for growth in the business as they expect fire services to return to the market to procure the updated and compliant SCBA range.

The Argus thermal imaging camera technology has made a significant cumulative contribution to Fire market sales. During the year they launched the Mi-TIC E L camera which can now be sold into the US market. This model is the most cost effective entry level solution for fire services.

During the period the group signed a five year contract with the UK MOD for the resupply and in-service support of its General Service Respirator. They expect that this will generate further opportunities to deepen their relationship with the MPOD. Likewise the launch of the MCM100 underwater rebreather has provided further opportunities to establish and strengthen relationships with a number of European and ROW militaries and demonstrate their innovation and delivery capabilities.

This year has seen an expanded market demand for their protection products as the needs of the law enforcement community to meet the CNRN threats has increased. This has been reflected in the significant sales momentum in the US for their supplied and powered air products, following NIOSH safety approval in March, and the strong sales performance of hoods and mask systems in Europe, the Middle East and Asia. They have seen good market penetration with US law enforcement municipalities and in the medium term they expect their share of the market to grow.

The operating profit in the Dairy division was £6M, a decline of £300K when compared to last year, entirely due to last year’s post acquisition working capital adjustment. The underlying operating profit was flat (although at constant currency it increased by 6.7%). At constant currency, revenues grew by 4%. Interface grew revenue by 3%, PCI by 2% and Farm Services by 20%. The growth reflects the current stable global dairy market conditions and the improved trading conditions in North America in the second half of the year. The closing order book declined by 31% to £2.5M, however.

The growth in Interface revenue was driven by a stronger performance in North America in the second half of the year and strong growth in Latin America, Europe, the Middle East and Asia Pacific. North American revenues overall declined by 2% reflecting the weaker market conditions in the first half of the year. In Europe, revenue grew by 7%. Latin America grew liner revenues by 12% reflecting market share gains in Brazil, and Asia Pacific liner revenues increased by 8% as a result of stronger market conditions in China.

The sales of their Precision, Control and Intelligence range have continued to perform well across their key markets. Revenue grew by 2% at a constant currency rate as dairy farmers continued to invest in their PCI products to drive farm efficiency. This was driven by growth in Europe of 3.6% and of 10.5% in the Middle East along with market share gains in Latin America driving growth of 17.6%.

Farm Services saw revenue growth of 20% to £5.2M, reflecting the ongoing success of Cluster Exchange which saw a 14% growth in cluster points in the period. North America saw a growth of 21% and Europe 19%. The extension of Farm Services to include Pulsar Exchange and Tax Exchange provides opportunities for growth in future years. At the year-end, Cluster Exchange had grown to 40,000 cluster points on 2,100 farms.

In March the group disposed of Avon Engineered Fabrications, its US based hovercraft skirt and bulk liquid storage tank business. The business made a profit this year of £500K and the group made a £1.1M gain on disposal (net of tax).

In June the group acquired the assets relating to Merrick’s calf nurser product line. The consideration was $1.8M in cash and associated costs of acquisition were $300K. The acquisition involved the purchase of tooling equipment at a value of £1.2M and customer lists, order books and brands at a value of £400K. There was no goodwill generated. The group has been a long standing manufacturer of the rubber component of the calf nurser product and the acquisition enables them to take full control of the distribution.

The restructuring costs this year of £900K represent a charge in respect of the relocation of the West Palm Beach assembly facility. To achieve a greater level of production efficiency, they relocated this facility to their main US manufacturing facility in Cadillac, Michigan. During the year they worked with a local partner to install a production assembly line in Kazakhstan for the production of escape hoods for the oil and gas sector.

The development expenditure in the year has focused on Protection products with significant investment in the UK GSR, MCM100 and next generation hood programmes. They also invested in obtaining NIOSH safety approval for their supplied and powered air range and preparing their upgraded Magnum SCBA for NFPA verification. Development expenditure in the dairy business included the upgraded milk meter equipment and subsequent ICAR approval together with the PCI heavy duty equipment for North America to meet the needs of their larger industrial farm customers.

They continued to work with the DOD on a number of potentially significant new platform programmes including the M69 aircrew mask, the M53A1 mask and powered air system and a follow on M50 mask system contract. They currently expect to enter into multi-year contracts with the DOD for the M69 aircrew mask and the M53A1 mask and powered air system in the new year with production starting in the second half. They are also in discussions to put in place a follow on contract for the M50 mask system following the conclusion of the initial ten year contract in July.

After the year-end the high court handed down a judgement involving the pension schemes. This concluded that pension schemed should be amended to equalise pension benefits for men and women. The board are working with advisers to understand the extent to which the judgement chrystallises any additional liabilities for the group’s pension scheme. They are early in the evaluation process but they estimated that the additional liability could be in the region of £3M which is likely to be recognised in H1 2019.

Going forward the opening order book of £37.8M (23% higher than last year) provides good visibility as they enter the next year and they are well positioned to continue their strong momentum into 2019. Within the protection division, first deliveries of the M69 aircrew masks, the M53A1 mask and powered air system, and the UK General Service Respirator of the UK MOD will be made in 2019. The revenue opportunities from new products and customers is expected to offset the impact of the anticipated reduction in M50 mask system volumes. Alongside this they expect continued sustainable growth from the widening customer and product base in Law Enforcement and following the launch of the upgraded Magnum SCBA they expect a stronger performance in the fire business. There also remains a healthy pipeline of potential further contract opportunities.

Dairy market conditions have remained stable, although there has been some recent market caution around expectations for future feed prices. In this environment, they currently expect that the growth trends experienced by the business will continue into the New Year.

At the current share price the shares are trading on a PE ratio of 19.6 which falls to 16.7 on next year’s consensus forecast. At the year-end the group had a net cash position of £46.5M compared to £24.7M at the end of last year. After a 30% increase in the dividend the shares are yielding 1.3% which increases to 1.6% on next year’s forecast and dividends are expected to grow ahead of earnings in the near term.

On the 14th November the group announced that non-executive director Petrus Vervaat acquired 2,000 shares at a value of £27K.

Overall then this has been a bit of a mixed year for the group, although it seems conditions in the dairy market at least improved in the second half. Profits were down due to higher tax charges. Pre-tax profits increased but this was mainly due to a lack of impairments and underlying profits were fairly flat. Net assets increased, however, and although the operating cash flow declined somewhat, plenty of free cash was generated.

The protection division is ticking along well, boosted by a good showing in the law enforcement market. The fire protection market was subdued but should improve next year with new models coming out. The Dairy market was broadly flat but discounting the effect of detrimental forex movements, underlying profits improved driven by a good showing in the farm services division. The forward order book looks good but the shares are not cheap with a forward PE of 16.7 and yield of 1.6%. Despite this, the quality on offer here temps me to buy back in.

On the 7th January the group announced a sole source supply contract to supply the US DoD with the M69 Joint Service Aircrew Mask for Strategic Aircraft, related accessories and engineering support. The contract has a maximum value of $92.7M over a duration of up to seven years, being a five year base period plus two further one-year option periods. The group expects to receive the first order under this contract shortly with deliveries expected to commence in H2 of this year. This is a significant new multi-year mask system platform for Avon Protection and extends their capabilities into the important aviation sector. They are continuing to pursue a number of other opportunities with the DoD and ROW military customers, both to extend their portfolio further and broaden their customer base.

On the 31st January the group released a trading update. The protection business saw a solid start to the year with a strong performance in the military business underpinning expected revenue growth in the first half of the year. Following the award of the M69 Aircrew Mask contract from the US DoD the first order is expected soon with deliveries commencing in the second half. They are making good progress on a number of other opportunities with ROW military customers and the DoD, including the multi-year M53A1 mask and the powered air system and the M50 sustainment contract.

They continue to see a strong pipeline of law enforcement and fire opportunities but the recent partial US government shut down is impacting the timing of orders from these customers and the group’s ability to obtain export licenses for US manufactured products. As a result they now expect their law enforcement and fire revenues to be more weighted to the second half of the year.

Global dairy market conditions softened in Q1 with falling milk prices impacting farmer confidence. This has impacted trading in all three business lines, and particularly precision, control and intelligence given the longer replacement cycle for these products. They expect upward pressure on feed prices in Q2 to have a further adverse impact on dairy market conditions and they now expect milkrite and Interpuls revenues for the full year to be flat on a constant currency basis with a low single digit decline in the first half.

The continued strong momentum in the protection business is expected to offset the tougher dairy market conditions so the board remain confident of achieving current year expectations.

On the 1st February the group received its first orders under the M69 aircrew mask contract for 7,000 mask systems and related accessories worth $17.8M. Deliveries under these orders will start in the second half of the year and will contribute to the expected military revenues in 2019.

On the 26th March the group announced that they had been awarded a sole source contract to supply the DOD with the M53A1 mask and powered air system and related accessories. The framework contract includes the ST54 self-contained breathing apparatus and has a maximum value of $246M over a duration of up to seven years, being a five year base plus a further two years extension.

The group expects to receive the first order under this contract shortly, with deliveries expected to start in the second half of 2019 and will contribute to the expected military revenues for this year.

On the 28th March the group announced that it had received its first order worth $20.2M under the M53A1 mask and powered air system framework contract with the DOD.