Bioquell sells biological contamination control services and equipment into the international life sciences, healthcare and defence markets. One important offering is hydrogen peroxide vapour bio-decontamination technology which has been used by the US military programme to eradicate biological warfare agents and reduces hospital acquired infections. In addition the group utilises HEPA and activated carbon air filtration which it uses to breakdown hydrogen peroxide vapour as well as to protect military vehicles and facilities from biological, chemical, radiological and nuclear contamination.

The group has now released its final results for the year ending 2014.

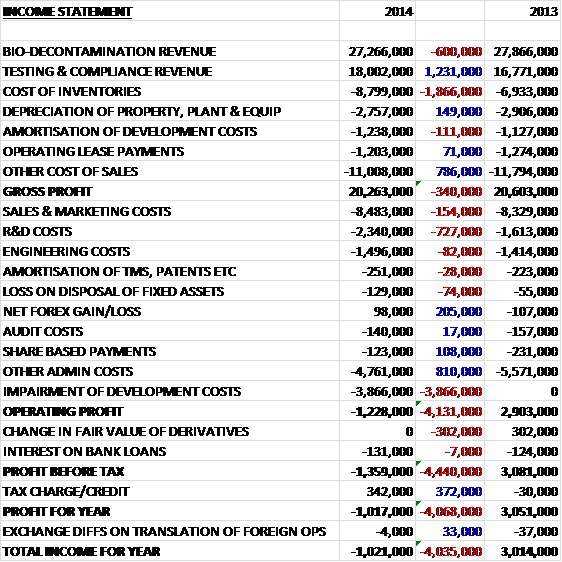

Overall revenues increased when compared to last year as a £600K decline in bio-decontamination revenue, held back by operational difficulties in the US and Asia, was more than offset by a £1.2M increase in testing and compliance revenue. Cost of inventories also increased, however, which meant that gross profit for the year was some £340K lower. Sales and marketing costs grew modestly but R&D costs were up £727K which was mostly offset by a reduction in admin costs and a favourable forex movement before a £3.9M impairment of intangibles, mostly development costs, meant that there was a loss at the operating level, an adverse movement of £4.1M when compared to 2013. After movements in derivative financial instruments were offset by a tax credit, the profit for the loss for the year was £1M, an adverse movement of £4.1M year on year. Even without the impairment charge, the profit would have been lower.

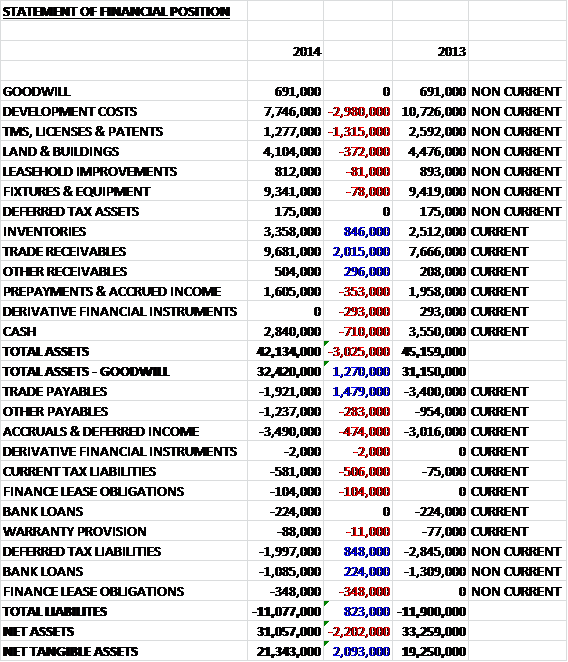

When compared to the end point of last year, total assets fell by £3M driven by a £3M fall in capitalised development costs, a £1.3M fall in other intangible assets and a £710K decline in cash levels, partially offset by a £2M increase in trade receivables and an £846K growth in inventories. Liabilities also fell during the period due to a £1.5M decline in trade payables and an £848K decrease in deferred tax liabilities. The end result is a net tangible asset level of £21.3M, an increase of £2.1M year on year.

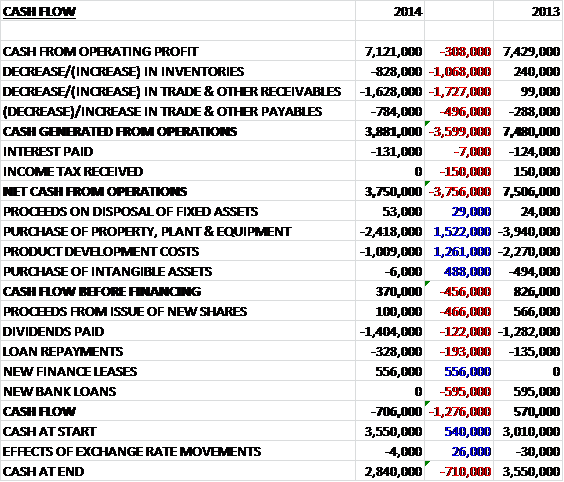

Before movements in working capital, cash profits fell by £308K to £7.1M. When compared to last year there was also a detrimental movement in all constituents of working capital with a particularly large increase in receivables and after the income tax rebate of last time was not repeated, the net cash from operations was £3.8M lower at £3.8M. The group then spent £2.4M on fixed assets and £1M on project development to leave a few cash flow of just £370K. This was not enough to cover the £1.4M of dividends paid out and after some cash received from the new finance leases, the cash outflow for the year was £706K to give a cash level of £2.8M at the year-end.

The Bio division encountered significant headwinds in the Life Sciences market, particularly in Asia and the US, and a number of management changes were made during the year. In the division, healthcare revenues increased by 26% to £4.3M, assisted by the new single patient pod product which is used to isolate beds in open plan multi-bed hospital rooms which are common outside the US and France, as well as increased interest in the hydrogen peroxide vapour technology as a result in part of the decontamination service activities during the Ebola outbreak. Defence revenues more than doubled to £4.1M but life sciences revenues, mainly from equipment sales, reduced by 17% to £18.9M.

The Trac revenues were strong across all services with particularly good results from the environmental and electromagnetic compatibility services helped by high levels of aerospace activity.

The group have taken a number of steps to try and reduce the lumpiness of their defence orders, in large by extending the range of applications for their products. Interest in the CBRN filter products have been aided over the past year by increased sectarian conflicts in the Middle East as well as instability close to the Russian border in Eastern Europe.

Many of the group’s customers are highly conservative and adopt new technologies slowly so it can take some time and substantial marketing investment to see increased revenues linked to the launch of a new product. In order to supply the breadth of products as well as the short response times for services, they require a large facility in the UK which has high fixed costs and associated operational gearing. This facility currently has significant under-utilised capacity which could be used to generate high margin incremental revenues.

The group have made good progress during the year in increasing the number of regulatory approvals for their hydrogen peroxide consumables around the world. They also extended their supply chain to enable them to supply consumables cost effectively to a greater proportion of international customers. They have also taken a number of steps to repackage certain technologies to enable them to migrate from an equipment based offering to increase the provision of specialist decontamination services which should improve recurring revenues and quality of earnings.

In the last couple of years the group have reduced their dependency on HPV by delivering complementary products such as the QUBE for life sciences and the Pod for healthcare. They are also in the process of launching a new HPV product, the BQ-50. This product is designed both for use in hospitals and for the provision of decontamination services by the network of international distributors. This product draws on the technologies and components which were developed for a US military development programme a few years ago, including fast cycles, smaller size, reduced weight and automated cycle calculations. It is anticipated that this product will help the group increase their equipment and service revenues in the healthcare sector in 2015.

During the year the group deployed twenty Pods in conjunction with four suites of HPV equipment in a Saudi Arabian intensive care unit in advance of the annual Hajj pilgrimage at Mecca. This was the first substantial Pod deployment outside the UK and it is anticipated that this reference site will generate further Pod and HPV bio-decontamination revenues from the Middle East. The recent Ebola outbreak has created significant interest in the group’s equipment and services. The HPV technology has been used to decontaminate Ebola patient rooms in three hospitals in the US as well as in hospitals in the UK, France and Holland. The group have been talking to hospitals in Europe and the US about helping them with Ebola emergency preparedness and, via the Pod technology, isolation surge capacity.

The group has been developing BioxyQuell, a peroxy-chemical based wound treatment technology for a number of years. The technology has regulatory approval in the EU and they have been working on the commercialisation of the product in the UK. They have found it difficult to commercialise the technology in the current hospital funding environment, however, and they have taken the decision to suspend the project as it is believed there are better opportunities with other products in the portfolio so the board has taken the decision to impair the value of development costs of this technology.

During the year the group ceased working on the contract to develop COLPRO solutions for a new vehicle for the British Army. Subsequently to the cessation of this contract they essentially halved the size of the engineering team as the end of the contract has cost them £300K a year. Due to the risks associated with such programmes, the board have taken the decision not to carry out large defence-related development contracts in the future. They did manage to secure other COLPRO contracts related to the standard CBRN equipment from customers in the Middle East and Eastern Europe, though. A proportion of these contracts was delivered in 2014 and based on the orders already received, they will continue to generate revenues into 2015.

There does seem to be a decent amount of headroom on borrowings with an unused revolving credit facility of £6M and undrawn overdraft facilities of £1.5M. It is interesting to note that last year, about a quarter of shareholders voted against the remuneration report which is quite strange as the directors don’t seem to be that aggressively paid. The group is somewhat susceptible to foreign currency changes with a 10% strengthening of Sterling against the US dollar reducing profits by £109K and a 10% strengthening against the Euro reducing profits by £73K.

After the year-end the group sold the TraC division for a cash consideration of £44.5M and is expected to give rise to a profit of £35.4M with the majority of cash proceeds being returned to shareholders. The sale of the most profitable part of the business does seem to lack ambition somewhat but the board believe that the remaining Bio division represents an attractive standalone business with interesting prospects.

In the life sciences sector growth is expected due to increased sales of biologics and biosimilars, which require the use of aseptic principles during research as well as the manufacturing process. The imposition of more demanding regulations and compliance requirements in the life sciences and healthcare sectors is also expect to increase demand for the group’s products. Within the healthcare sector hospitals face increasing difficulties treating patients who contract antibiotic resistant bacterial infections. The imminent launch into the healthcare sector of the BQ-50, a new small, fully automated product to rapidly eradicate pathogens from surfaces in hospitals should also help drive revenues in this sector.

During the past year the group reduced the cost base in the Bio business substantially, particularly in relation to their engineering resources, and also made significant changes to the management structure of the American and Asian subsidiaries, the results of which will be seen in the coming financial year. The new year has started well for both divisions and it is believed that the business can deliver significant value to shareholders in 2015.

The substantial phase of significant capital investment in new products and services such as QUBE, Pod, BQ-50 and consumables, is essentially over. Going forward the group expects to see product line extensions and technology updates but with a markedly lower requirement for capital expenditure so it is expected that the Bio division will start to generate cash. Sales in the Life Sciences sector currently remain key to the profitability of the division and steps have been made to address the issues encountered in that market. The lack of single patient rooms in many critical care rooms in hospitals and the increasing prevalence of antibiotic resistant infections creates opportunities in the healthcare market and the defence business is well positioned with a significant order book already covering most of the planned 2015 defence related shipments.

At the current share price the shares trade on a PE ratio of 20.7 which reduces to 20 on next year’s consensus forecast so that doesn’t look great value. The shares currently yield 2.4% which is identical to the figure expected next year. The net cash at the year-end was £1.1M compared to £2M at the end of last year.

Overall then this is an interesting company. Over the past year, though, profits have fallen as have operating cash flows. There is still some free cash, however, but this does not cover the dividends and the net tangible assets improved during the year. The Testing and Compliance division seems to be doing very well but sadly this has been sold, albeit for quite a decent amount. The remaining bio division is doing less well due to headwinds in the life sciences division in the US and Asia – progress in the much smaller healthcare and defence markets seems to be better.

There are some interesting products which may add to future profits with the pod gaining traction and BQ-50 looking promising. The emergence of Ebola and MERS must be a good thing for the group and there is likely to be less cash used in capex going forward. The shares are not that cheap, however, trading on a PE of about 20 and delivering a yield of just 2.4% so I am going to watch proceedings here from the side lines for a while.