Creston has now released its interim results for the year ending 2016.

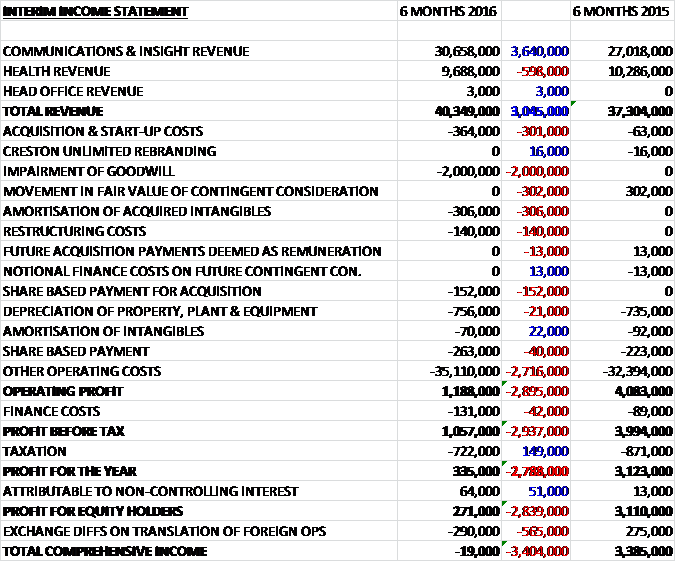

Revenues increased when compared to the first half of last year as a £598K decline in health revenue was more than offset by a £3.6M growth in communications and insight revenue. “Underlying” operating costs increased by some £2.7M and we also see various other costs including acquisition costs, amortisation of acquired intangibles and the lack of a reduction in contingent consideration that occurred in the first half of last year. The largest cost though is a £2M impairment of goodwill so that the operating profit came in £2.9M lower. A small increase in finance costs was offset by a fall in taxation and the profit for the period attributed to shareholders was £271K, a decline of £2.8M year on year.

When compared to the end point of last year, total assets increased by £1.9M driven by a £3M growth in intangible assets, a £2.8M increase in receivables, a £2.7M growth in goodwill and a £1M investment in an associate, partially offset by a £7.4M fall in cash. Total liabilities also increased during the period as a £3.4M growth in the bank overdraft, a £1.1M increase in payables and a £758K growth in the deferred tax liability was partially offset by a £1.4M fall in deferred consideration. The end result is a net tangible asset level of £3.5M, a decline of £7.2M over the past six months.

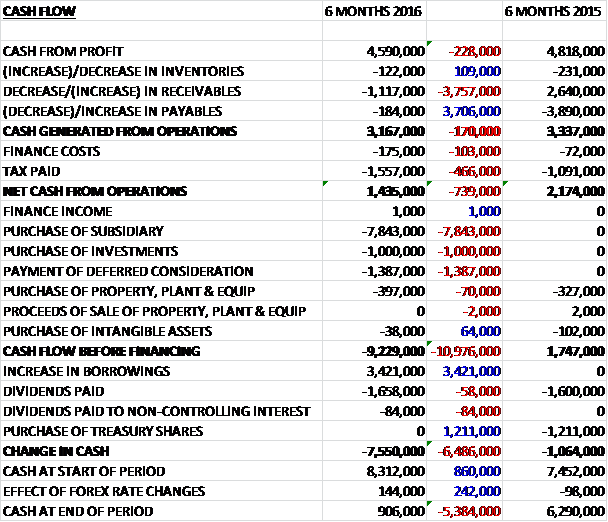

Before movements in working capital, cash profits fell by £228K to £4.6M. A cash outflow from working capital, in particular an increase in receivables, along with higher tax and interest paid meant that the net cash from operations was just £1.4M, a decline of £739K year on year. The group then spent £397K on property, plant and equipment along with £38K on intangible assets but they also spent £7.8M on an acquisition, £1M on an investment and £1.4M in deferred consideration so the cash outflow before financing came in at £9.2M. A £3.4M increase in borrowings helped a bit but there was still a £7.6M cash outflow during the period to give a cash level of just £906K at the end of the first half.

The Unlimited strategy continues to increase inter-agency and partner cross-referrals and results in a growing number of invitations to pitch for multi-discipline and international accounts. In terms of new business the group has added a mix of new clients and brands such as Logitech and Costa, and assignments from existing clients such as Canon, Danone and Diageo with many of the wins involving two or more of the businesses under the new Unlimited proposition. The new business wins are continuing into the second half of the year including their win of the Vodafone Customer Value marketing account, their appointments as both Sony Mobile and McLaren’s global lead digital strategy agency and most recently the appointment as British Airways’ CRM and data strategy adviser.

Following the lacklustre first half, the board are budgeting for improved growth in the second half. The factors behind the slow growth in the first half were weaker trading by a small number of their larger retail and consumer tech clients causing budget cuts; an adverse financial impact of about £400K attributed to the weakening Euro on the Euro-based revenue contracts which have grown during the period; and a slower performance in the UK health advertising offer, predominantly due to the healthcare industry’s growing need for integrated channel neutral and more patient centric campaigns. As a consequence of this third factor, the group took the decision to combine the offers of DJM and PAN to create a multi-channel agency.

The “underlying” profit in the Communications and Insight division was £4M, an increase of £800K year on year although it seems that £700K of this growth has come from the How Splendid acquisition with a 4% growth in like for like sales. There have been two major product launches during the period. Reflected Life allows the group to measure, track and understand a consumer’s digital behaviour and experience across multiple devices, providing insight that helps their clients to influence future behaviours. The Real Adventure Unlimited has launched Real Data, a new data offering strengthening their data capabilities by using their insight data and analytical innovations.

Significant new business wins during the period included work for Emmi Caffe Latte, referred by Serviceplan; and Mitsubishi, referred from Asian marketing network, Hakuhodo. There were also further assignments from existing client SSE and post period end wins include projects for Barclaycard and Sky’s on-demand box sets. The partnership with Serviceplan and the close working relationship with Hakuhodo contributed to the 19% increase in revenue derived from international work for clients.

The “underlying” profit in the Health division was £1.6M, a decline of £100K when compared to the first half of last year on a 6% decline in revenues. Following a slower performance in the health advertising offer, and the healthcare industry’s growing need for integrated channel neutral and more patient centric campaigns, the group have combined DJM and PAN to create DJM PAN Unlimited (see what they have done there?!). With almost all clients shared, uniting the two businesses more formally made sense.

The Health business had some significant new client wins and projects for existing clients during the period including Abbvie, AstraZeneca, Bristol Myers Squibb, CDC, Columbia Neurosurgery, Gilead, International AIDS Society, National Meningitis Association, Norgine, Novartis, Pfizer, Seqirus and Takeda. The period also saw the launch of Search Unlimited, a specialise SEO agency for the healthcare sector, offering natural search, paid search and paid social solutions to a number of global pharma companies and consumer healthcare brands.

In April the group acquired 51% of How Splendid, a London-based digital design and development consultancy. The group spent £8.7M in cash and the transaction generated goodwill of £5.1M. There is potential for a further additional consideration payment of up to £7M in June 2017 based on average profit up to March 2017. This payment would be considered deemed remuneration and will be expensed to the income statement as the provision is recognised. Currently there is zero deferred consideration due to first half project variability which will be reassessed going forward. I’m afraid I don’t know what first half project variability means so am a bit confused why no contingent consideration has been recognised.

The fair value of non-controlling interest in Splendid is deemed to be nil on acquisition due to restrictions on the 49% non-controlling interest which links the ownership of those shares to continuing employment for two years from the date of the acquisition. As such a share based payment charge will be recognised to value this liquidity foregone to build up a balance in equity from the date of acquisition to the two year anniversary of the seal. At the anniversary of the deal this will convert to non-controlling interest which is forecast to be £700K. For the remaining share capital there are no put options, but the group will have the option to acquire a further 24% from April 2017 for a maximum value of £8.6M and the remaining 25% from April 2019 for a maximum value of £11.9M. Since the acquisition, Splendid contributed profit of £700K so it seems to be quite profitable but this is a really complex arrangement I think.

In June the group made a strategic investment in 18 Feet and Rising ltd, a London-based advertising agency, for a consideration of £1M representing 27% of the business. During the period the decision was taken to close Fieldwork UK due to declining demand of face to face market research data collection which led to a goodwill impairment of £2M. There have also been a number of new partnerships entered into. In April they signed with their second international partner, Propeller Communications, a digital healthcare communications agency based in the US. Also in April, they signed with Future Foundation, a global consumer trends and insight consultancy and the Design Consultancy to add to the consultancy offer alongside Splendid.

As with most companies there is a plethora of “non-underlying” costs here, some of which are more underlying than others. Acquisition costs of £100K were incurred in relation to the acquisition of Splendid and £40K for the investment in 18 Feet and Rising. As the group clearly relies on acquisitions, I feel these are probably underlying. Start-up business trading losses totalling £200K were incurred associated with Reflected Life, Real Data and Search Unlimited, in their first year of trading. Along with Creston Unlimited rebranding costs of £30K representing costs as a result of the launch of the new agency brand, Creston Unlimited and the rebranding of all group businesses with the “Unlimited” suffix. Sorry, but taking out losses from new brands is wrong in my view and whilst rebranding is more likely to be non-underlying, I see this as general costs of doing business really.

There was also a £200K share based payment charge relating to the valuation of the liquidity foregone of the non-controlling interest shareholders – more acquisition costs then? Restructuring costs of £100K were incurred comprising £50K spent on the closure of Fieldwork UK and £90K spent on combining DJM PAN. Those costs are borderline I think, they are not huge so I will probably include them. Finally there was a £2M goodwill impairment recognised as a result of the closure of Fieldwork UK. OK, Goodwill is a nonsense anyway so this is one cost I am happy to discount.

There have been a couple of board changes in the period. Nigel Lingwood joined as a non-executive director and after nine years, Andrew Dougal will step down from the board as non-executive director in November.

Whilst the slower growth in Q1 has been followed by a stronger performance in Q2 and start to the second half of the year, the board are expecting their full year performance to be slightly behind expectations.

After a 5% increase in the interim dividend, at the current share price the shares yield 3.6% increasing to 3.9% on the full year consensus forecast. At the end of the first half the group was in a net debt position of £2.5M compared to a net cash position of £6.9M at the end of last year.

Overall then this is a bit of a disappointing set of results. Profits were down but when all of the non-underlying items were taken out, they were broadly flat; net assets declined; and operating cash flow fell generating no free cash after the payment of deferred consideration and nowhere near enough to pay for the acquisition. There were some good sounding contract wins but performance was effected by weaker trading from clients, the weakness of the Euro and the fact that the health business does not seem to be aligned with what their clients are actually looking for. Clearly nothing can be done about the first two issues but the last one is apparently being addressed. In all, the Communications and Insight division showed lacklustre organic growth and the health division reported a small decline in profits.

I am a little concerned about the acquisition as I don’t understand the terms – why is there no contingent consideration recognised? It seems to me that there are some potential liabilities off the balance sheet going forward. Trading in Q2 was better than Q1 and it sounds as though trading so far in the second half if going fine but the board still expect full year results to be slightly below expectations. This is a real shame as there was a point where Creston was one of my conviction buys but it seems as though the turnaround strategy has lost momentum somewhat and the 3.9% dividend yield is not quite enough to compensate for this in my view so I am out for now.

On the 26th November the group announced that CFO Kathryn Herrick purchased 5,700 shares at a cost of £6.8K. This is her first share purchase and while welcome, is not a massive vote of confidence.

On the 27th January the group released a trading update for the first nine months of the year. Following revenue growth of 8% in H1, growth in Q3 saw revenues increased by 11% giving rise to a 9% growth year to date. Like for like revenue growth stood at just 2% in the quarter with like for like revenue growth year to date standing at just 1%.

In the first few weeks of 2016, the group has been advised by a number of clients across multiple industries of project delays and cuts. Some of these relate to client specific circumstances and others are due to increasing concerns they have about the trading outlook for their businesses given the current uncertainty of the global economy. This will lead to significantly reduced revenue growth in Q4 compared to board expectations and there is limited opportunity to mitigate the impact on operating profit from the reduced revenues.

As a consequence, the board expects full year revenue to be about 8% ahead at £83M and flat on a like for like basis with headline pre-tax profits slightly below last year at £9.9M. In addition they expect to report exceptional charges likely to include a charge for impairment of the carrying value of goodwill (no real loss there then). They expect to see a broadly neutral cash position at the year-end.

Despite this the group continued to see considerable new business during the period with wins including the Vodafone Customer Value Marketing account, appointments as both Sony Mobile and McLaren’s global lead design strategy agency, an appointment as British Airways’ CRM and data strategy adviser, the local marketing of Bosch Power Tools and Garden UK and the CRM and digital strategy for Weetabix.

This is very disappointing. Despite some impressive contract wins, Creston seems unable to improve like for like sales and profits. I am not rushing to buy in here.

On the 18th February the group announced that Iain Ferguson joins as non-executive director, representing the company’s largest shareholder, DBAY Advisors. It was also announced that Chairman Richard Huntingford has decided to step down next month having been in the role since 2014. So, it seems as though the shareholders are getting restless here.

On the 18th April the group released a trading update covering 2016. The board expects the group’s financial performance to be in line with the previous statement and consensus expectations with net cash ahead of expectations at over £1M. As previously announced, exceptional charges will include a charge for impairment in the carrying value of goodwill. The actions taken since the last update and a more stable outlook for the group’s clients mean they are well placed for future growth. This is not a bad update considering the issues faced the group and I am considering taking a small position here again.