BP probably does not need much introduction, but in case anyone doesn’t know, they are an Oil and Gas company whose business model involves exploring for hydrocarbons, bringing them to the surface, moving them using pipelines, ships, trucks and trains, capturing value across the supply chain; refine, process and blend the hydrocarbons to make fuels, lubricants and petrochemicals and supply customers with fuel for transportation, energy for heat and light, lubricants to keep engines moving and petrochemicals to make a variety of everyday items such as paints, plastics and textiles.

BP’s activities are separated into Upstream, Downstream and Other business. Upstream activities include oil and gas exploration, field development and production; midstream transportation, storage and processing; and the marketing and trading of Natural Gas. Downstream activities include the refining, manufacturing, marketing and supply of crude oil, petroleum products, and related services. The other business includes investments in renewable energies, shipping and corporate activities.

Fuels sold include gasoline, diesel, aviation fuel and LPG.

They are active across the globe, but some of the main regions are Alaska, where 13 oilfields and 4 pipelines are operated, along with significant interests in 6 other producing fields; the Gulf of Mexico, where oil and gas are produced from four operated hubs, and three non-operated hubs; Trinidad and Tobago, where 13 offshore platforms are operated, along with one onshore processing facility; the North Sea region, where 30 oil and gas fields are operated, along with two major terminals and an extensive network of pipelines; Azerbaijan where projects include the Azeri-Chirag-Gunashli oil field, the Shah Deniz gas field, three major terminals and a number of long distance pipelines; and Angola where the group holds a position in 9 deepwater licences and the Angola LNG project.

BP have now released their results for the year ending 2012.

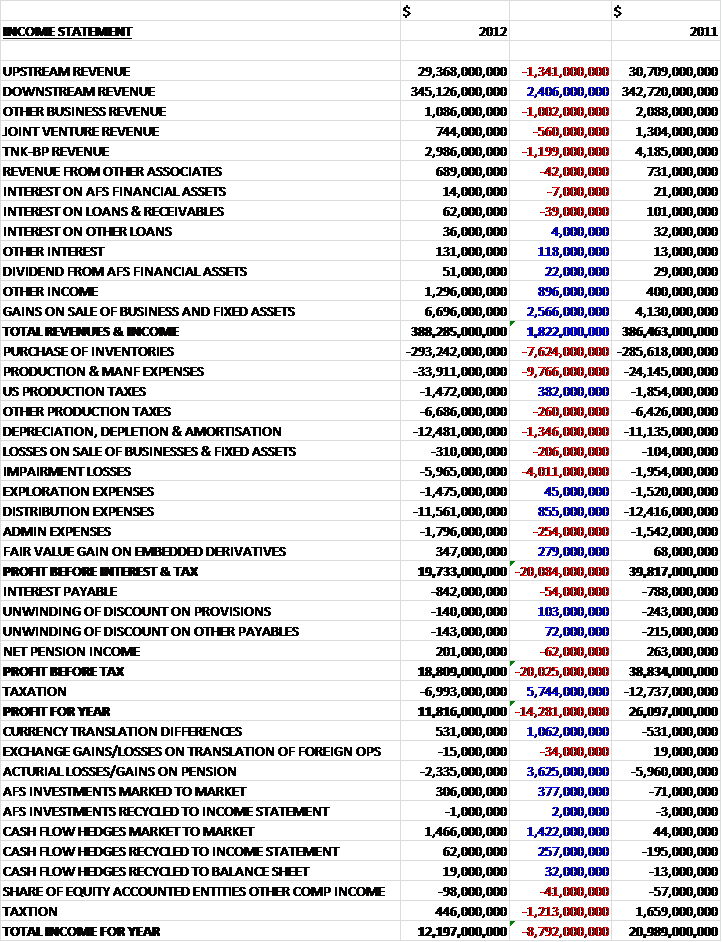

As BP spent the last year divesting assets, it comes as no surprise that revenues are down across nearly all business sectors. Interestingly, however, revenues in the downstream business have increased by $2.4B over the year. The fall in the TNK-BP revenue is because that business was classed as an asset for sale towards the end of the year so the revenue received has been recorded elsewhere ( I think under “other income”). Apart from other income, the only other major gain was in the sale of business and other assets – BP made $6.7B in profit from this over the year.

Taking out the asset sales, the group suffered a revenue fall during the year. Compounding this was an increase in costs. Inventory costs were up by $7.6B but more alarmingly production and manufacturing expenses increased by nearly $9.8B. Also included here are nearly $6B of impairment losses and a $254M increase in admin expenses. Not all expenses rose, however, as both exploration and distribution costs were down. The profit before tax halved as a result of the above and after (a much reduced) tax bill is taken into account, the profit for the year was $11.8B, compared to $26.1B last year.

Non-operational costs for the year included a charge of $370M relating to onerous gas marketing and trading contracts; $308M relating to exploration expenses associated with the US natural gas assets and $244M relating to their exit from the solar business.

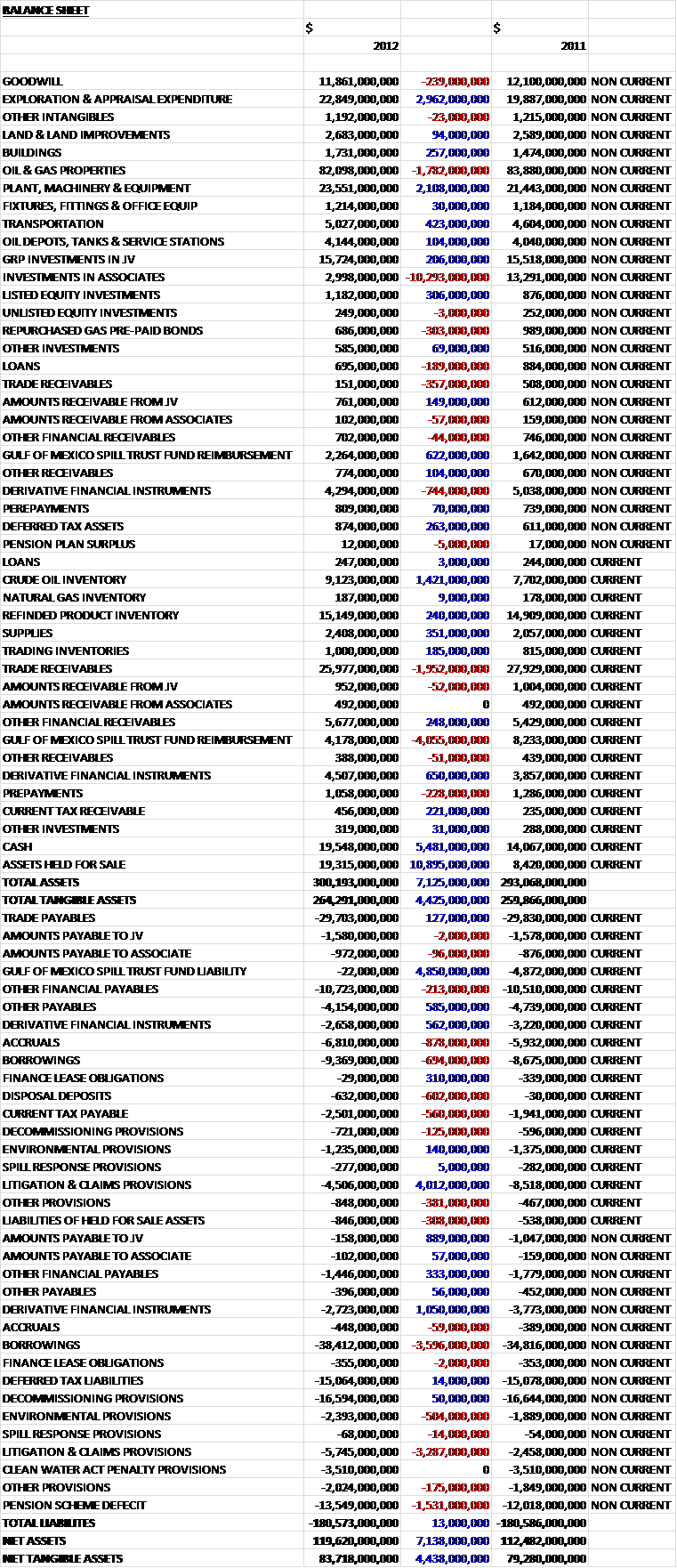

Overall assets actually increased by over $7B during the year. The largest movers were nearly $3B more of capitalised exploration expenses; a $2.1B increase in plant and equipment; a $1.4B increase in the value of crude inventories and a pleasing $5.5B increase in cash. These were mitigated somewhat by a $1.8B reduction in oil and gas properties, nearly $2B less in trade payables and a net $3.4B reduction in the Gulf of Mexico Trust Fund reimbursement, which relates to future expenditure already provided for that will be paid from the fund, so is a non-cash related asset.

Looking at liabilities, we can see that these remained flat year on year. The big fallers were a $4.9B reduction in the Gulf of Mexico Trust fund liabilities as most of this money now seems to be paid in. Whether it will be enough to cover the amount needed is another matter. The other major decreases were a net $700M decrease in litigation and claims provisions which I find somewhat surprising and a $900M decrease in payables to Joint Ventures. The main increases in liabilities were a $878M hike in Accruals, a hefty $4.3B increase in borrowing and a concerning $1.5B increase in the pension deficit, which now stands at $13.6B, as if BP didn’t have enough problems! In fact, as the group from next year will be adopting a revised version of IAS 19 Employee Benefits, they will (quite fairly it seems to me) have to adopt the same expected rate of return on plan assets as they use to discount liabilities which will affect (non-cash) earnings by about $1B. The deferred tax payable was increased because the restriction of tax relief for decommissioning expenditure in the North Sea fell from 62% to 50%. This was mitigated somewhat by the reduction in UK corporation tax. The provisions relate to settlements of criminal charges, penalties for liabilities under the clean water act and legal fees. All the above has given rise to a $4.4B increase in net tangible assets to $83.7B.

We can see that operating cash flows were way down when compared to last year but the decrease in receivables when compared to the increase last year means that the net cash from operations was only $1.8B lower at $20.4B. This was more than wiped out by capital expenditure, however, which was $5.2B higher at $23.1B. A further $1.5B was invested into associates but the group did benefit from a massive $11.4B injection of cash from the disposals. There was also a net £3.9B of new loans which meant the group could pay $5.4B in dividends and have $5.4B left over. It is clear, however, that were it not for the business disposals that there would be a heavy cash outflow here.

The operational cash flow is expected to improve in 2013 due to reduced trust fund payments and higher margin projects coming online.

During the year, BP did not make any major business acquisitions, the most significant being the acquisition of Shell and Cosan Industria’s interests in aviation fuel assets at seven Brazilian airports. There were a number of assets held for sale, however, as the group seeks to streamline its operations and free up some more cash. Among those are a number of central North Sea oil and gas fields, namely BP’s interests in the Maclure, Harding, Devenick, Brae and Braemar fields. The sale has been agreed for $1.1B. BP has also reached an agreement to sell its Carson refinery in California to Tesoro Corp for $2.5B. The sale of the Texas City refinery was completed in early 2013 to Marathon Petroleum Corporation. The most significant disposal agreed, however, was the sale of BP’s share in the TNK-BP group to Rosneft for $11.6B in cash and an 18.5% stake in Rosneft which, although is an interesting development, I find a bit disappointing because BP is giving up considerable operational sway in a very major market.

TNK-BP was one of the ten largest non-state owned oil companies in the world with upstream interests in Russia, Brazil, Venezuela and Vietnam, producing about 2M barrels of oil per day and five refineries located in Russia and Ukraine and had recently announced the first gas from the Lan Do field in Vietnam.

Since 2010, the group have now sold about 50% of their upstream installations, 32% of their wells and 50% of pipelines. At the same time, the proven reserve base has only fallen by 10% and it does seem as though they are doing a good job of offloading mature assets whilst keeping hold of those with more potential.

During 2012, the group completed the sale of Marlin, Horn Mountain, Holstein, Ram Powell and Diana Hoover fields in the Gulf of Mexico to Plains Exploration and Production company; the sale of Hugoton and Jayhawk gas production and processing sites in Kansas and the Jonah & Pindale upstream operations in Wyoming to LINN Energy; the sale of their interests in the Canadian Natural Gas Liquids business to Plains Canada and a number of interests in the North Sea. Downstream, the group disposed of their interests in Purified Terephthalic acid production in Malaysia to Reliance Global Holding.

The group suffered an impairment loss of$1.1B in their interests in the Fayetteville and Woodford shale gas assets due to revisions in reserves; a $1B impairment loss relating to the decision to suspend the Liberty project in Alaska; a $706M write down of assets in the Gulf of Mexico and North Sea caused by the decommissioning provision resulting from continued review of the expected decommissioning costs; a $144M write-down of certain gas storage assets in Europe due to changes in the European gas market and other smaller impairment losses relating to other items. Downstream there was a $1.6B impairment on the sale of the Texas City refinery and a $1B loss on the assets during the sale of the Carson refinery. Finally, a $258M impairment loss was recognised due to the decision not to proceed with an investment in a biofuels facility in the US.

The fortunes of BP over the past few years have been dominated by the Gulf of Mexico rig explosion and the subsequent oil spill and the total amount that BP will need to pay on the disaster is still open to considerable uncertainty. Over the past year, the cost to the cash flow has been $6.3B, materially less than in the past two years. In 2010, a trust fund to deal with the subsequent claims was set up and financed to the tune of $20B. The fund does not cover any fines, penalties and administration costs relating to claims. Unfortunately it seems likely that the $20B in the trust fund will not be enough to fully cover all claims that are likely to arise and after the money runs out, BP will pay legitimate claims directly. The current cash balance of the trust fund was $10.471B.

So far the group has made a total of $32.8B of payments resulting from the Gulf of Mexico oil spill. In November, an agreement was reached with the US government to resolve all federal claims. BP pleaded guilty to 11 counts of misconduct relating to the initial loss of 11 lives; one misdemeanour count under the Clean Water act; one misdemeanour count under the Migratory Bird Treaty Act and one felony count of obstruction of congress. As a result, BP will pay $4B in instalments over a period of five years. The court also ordered that BP serve five years of probation. Also in November, BP agreed a settlement with SEC to resolve the SEC Deepwater Horizon related civil claims and has agreed to pay a civil penalty of $525M.

At the same time, the US Environmental Protection agency announced that it had temporarily suspended BP from participating in new federal contracts, which is rather unfortunate. In February 2013, the EPA issued a notice of mandatory debarment for BP at its Houston headquarters that prevents the company entering into new contracts or leases with the US government at those premises, which is another setback, particularly as these debarments typically last 3 to 5 years and the US government seems to want to make an example of BP, particularly as they have not had a great recent history in the US after the 2005 Texas City refinery explosion and the 2006 Alaskan pipeline leaks.

For the charges set out under the clean water act, the amount to be paid depends on a number of factors, one being the volume of oil that was discharged into the Gulf which has to be estimated. BP believes that the US government has over estimated this figure by about 20%. Another factor is how much per barrel of oil that will be charged. BP is currently working on a figure of $1,100 per barrel, which is the maximum charged unless gross negligence or wilful misconduct can be proven. Therefore the provision of $3.510B that covers this charge could be less in the unlikely event of the maximum not being charged, or much more (there is a theoretical maximum of $4,300 per barrel) if gross negligence or wilful misconduct is proven.

There is the likelihood of further legal claims against BP with regard to the Gulf of Mexico spill going forward, particularly a worrying looking claim by several US Gulf states for damages and loss of earnings that could end up being $34B. BP is obviously contesting this robustly but it could have a damaging effect in the future.

As well as the litigation from the Gulf of Mexico spill, BP is also defending a claim from Exxon against Alyeska, in which BP has a stake with regards to the response to the Exxon Valdez oil spill. It is not clear what they are claiming for and BP are defending the case. Another subsidiary, Atlantic Richfield is being sued over injuries due to lead pigment in some paints. So far, no claims have been upheld but there are some ongoing and the amount being claimed is apparently fairly substantial.

BP also has exposure to the sanctions placed on Iran. Two oil fields in the North Sea and related pipelines markets and supplies gas in which Naftiran Intertrade has interests have been shut down, also a Canadian university has been using graduate students, some of whom were nationals of Iran on a research program part funded by BP which has now been terminated by the company (amazing to think that was against regulations). Finally, BP involved an Iranian consultancy firm in 2010 for some auditing services that may have been against EU regulations.

BP is currently involved in a number of long term research projects. One is the International Centre for Advanced Materials (ICAM), a $100M 10 year research partnership aimed at advancing the understanding of advanced materials from self-healing coatings to membranes across a variety of energy and industrial applications. The University of Manchester will be the centre for this research. Another project is the Energy Sustainability Challenge (ESC) which studies the relationships between natural resource usage and energy production and consumption. Another is the Energy Biosciences Institute (EBI) which is a $500M 10 year study with some American universities to perform ground breaking research aimed at the development of next generation biofuels, as well as other bioscience applications to the energy sector. Halfway through the project, the EBI is generating a number of innovations, particularly in the field of cellulosic conversion. There is also the Massachusetts Institute of Technology Energy Initiative (MITEI), to which BP is providing another $25M for continuous energy research over the next five years. MITEI conducts research aimed at tackling energy challenges such as increasing energy supply, improving efficiency and addressing environment impacts of energy consumption. Finally, BP is in involved with the Energy Technologies Institute (ETI) which was set up to accelerate lower carbon technology development . By the end of the year, the ETI had commissioned $281M of work covering 41 projects.

The vast majority of the profit is made in the Upstream Business ($22.4B) with Downstream only making $2.4B and the Other Businesses making a $2.8B loss.

As far as the exploration side of business is concerned, during the year the group started activities in Brazil, Offshore Nova Scotia, Egypt, Gulf of Mexico, Namibia, Uruguay and the US. The principle areas of production were Angola, Azerbaijan, Argentina, Egypt, Trinidad, UAE, UK and the US. During the year, underlying production was broadly flat as major project start-ups and improved operating performance in Angola was offset by natural field decline.

In Europe, BP is active in the North and Norwegian Sea. In the North Sea, the Rhum gas field remained shut due to continuing sanctions on Iran, as the field is part owned by an Iranian company. In Norway, gas production from the Skarv field commenced and is expected to produce for 25 years. Daily crude production is 85,000 barrels with gas production of 670 M Cubic Feet. Production started at the Valhall field in January 2013 with daily production of around 65,000 barrels expected by the second half of 213. In the Gulf of Mexico, despite the problems there, 2 new rigs were started up with an eighth rig expected to start up in 2013. BP was assigned 51 exploration blocks and the Galapagos development was started during the year. In Alaska, BP operates 13 Oilfields and four pipelines, it also owns significant interests in six other producing fields. BP is working with ExxonMobil and ConocoPhillips to commercialise extensive natural gas resources on the North Slope of Alaska. Work on the Liberty Field was suspended during the year because the cost required to bring the rig up to scratch would be too significant, which resulted in an impairment of $1B. In the rest of the US, the group is involved in production of Natural Gas and condensate across nine states. Impairment losses of nearly $1.5B were recognised in the Woodford and Fayetteville shale reserves reflecting new market values in the prevailing low cost environment. The group has signed an agreement to lease 300 square km in Northeast Ohio for future oil and gas production.

In Canada, BP is focussed on oil sands development and holds interest in three oil sands leases; significant exploration interests in the Beaufort Sea and the new leases covering 14,000km2 off Nova Scotia. In South America, BP is active in Brazil, Argentina, Bolivia, Chile, Uruguay and Trinidad. In Brazil, the group has interests in 14 exploration and production blocks and in March approval was gained for its farm in to four deepwater concessions in which it has a 40% interest. The Bolivian government announced that it intends to nationalise interests in the Caipipendi Operations contract, in which BP has a 60% interest and production was impacted by a strike in the Cerro Dragon field – such are the risks of operating in South America at the moment. In Uruguay, contracts have been signed for 3 offshore exploration blocks covering 26,000 km2. Exploration and Production licences almost doubled during the year in Trinidad and the group now owns licences covering 1.8M acres offshore on the east coast.

In Africa, BP’s upsteam activities are in Angola, Algeria, Libya, Egypt and Namibia. They are present in nine deepwater licenses in Angola and own a small interest in the LNG project. The Clochas and Mavacola fields, which are run by Esso but in which BP has a 27% stake, started production and reached 65,000 barrels a day by the end of the year. The PSVM project also started up with a production of 60,000 barrels a day (but is expected to rise to 150,000 barrels a day eventually). In Algeria, BP owns interests in the Salah and In Amenas gas projects and has a joint venture in the Bourarhet licence which has been extended to September 2014. In January 2013, a terrorist attack occurred at the Amenas site and non-essential staff were pulled out. Limited production started again in February and BP is still committed to production in the country. In Libya, BP has a partnership to explore acreage in the onshore Ghadames and offshore Sirt basin and preparation work restarted in May after the civil unrest there. In Egypt, BP has interest in oil and gas assets and in June, the first gas from the Seth development was announced. In August, the group announced gas discoveries at Taurt North and Seth South, which were the fourth and fifth discoveries announced in the area (BP has 50% ownership). In Namibia, BP is a non-operating partner in five deep water exploration blocks.

In Asia, BP is active in Indonesia, China, Azerbaijan, Oman, Jordan, USE, India and Iraq. In Indonesia, BP has joint interests in a company supplying gas to the country’s largest LNG export facility, the Bontang LNG plant. BP also participates in the Sanga-Sanga CBM PSA, along with the Tanjung 4 and Kapuas 1, 2 and 3. The Kapuas sites will be exited shortly, however. In China, BP has interests in two deepwater exploration blocks in the South China Sea. In Azerbaijan, the group operates two PSAs and holds other exploration licenses and now has an interest in the export pipeline. BP is currently conducting exploration and appraisal programmes in Jordan and Oman. In Abu Dhabi, UAE, they have small interests in both onshore and offshore concessions, with the onshore one expiring in 2014. In India, the group has a 30% interest in nine oil and gas PSAs and a 50% interest in another. In Iraq, the group holds a 38% interest in the Rumaila service contract.

In Australia, BP is one of several partners in the North West Shelf venture, which has been producing LNG, pipeline gas, condensate, LPG and oil since the 80s. BP also has a 17% stake in some of the related oil reserves and infrastructure and stakes in some other smaller fields. In May, the seismic survey in the Ceduna Sub basin uncovered 12,500km2 and BP are now drilling four deepwater wells in this frontier exploration basin. In Eastern Indonesia, BP owns the North Arafura PSA on the coast of the Arafura sea and has interests in the Tangguh LNG plant, the West Papua 1 and 3 PSAs , and the West Aur 1 and 2 deepwater PSAs

In the North Sea, BP operates the Forties Pipeline System that handles capacity from more than 80 fields and has a 36% interest in the Central Area Transmission System that transports Natural Gas. In addition, the group operates the Sullom Voe oil and gas terminal in Shetland. In North America, the group has a 47% interest in the Trans Alaska Pipeline System, transporting crude oil from Prudhoe Bay to the port of Valdez. In Asia, BP has a 30% stake in the Baku-Tblisis-Ceyhan oil pipeline that transports oil to the port of Ceyhan in Turkey. The group has a 26% interest in the South Caucasus Pipeline which transports gas from Azerbaijan to the Turkish border and operates the Western Export Route Pipeline between Azerbaijan and Georgia.

As far as LNG is concerned, BP has a 10% stake in the Abu Dhabi Gas Liquefication company which supplied 5.6MT in 2012; a 14% share in the Angola LNG Project which is expected to produce 5.2MT when it starts up in 2013; is one of several partners in the NWS venture in Australia that has a capacity of 2.7MT and also in Australia, has a 17% interest in the Browse LNG venture. In China BP has a 30% stake in the Guangdong LNG regasification and pipeline project that has a 7MT annual capacity. In Indonesia, the group has a 38% holding in the Sanga-Sanga export terminal and a 37% stake in the Tagguh LNG plant and has a capacity of 7.6MT per annum. In December, government approval was gained to increase capacity at this plant by 3.8MT, with the extra capacity due to be online by 2018. In Trinidad, BP’s net share of the capacity at the Atlantic LNG trains is 6MT per year.

There have only been some minor new crude discoveries in the US and Russia. There have, however, been some large discoveries of Natural Gas in the US, South America and Russia. There were five major start-ups during the year – Galapagos in the Gulf of Mexico; Clochas Mavacola and Block 31 in Angola; Devenick in the North Sea and Skarv in Norway. The Angola LNG plant was also commissioned to start production in 2013.

As at the end of the year, BP has interests in 16 refineries, this will be reduced to 14 during 2013, following the sales of the Texas City and Carson refineries in the US. At the Toledo refinery, a higher efficiency naphtha reformer was completed.

The group also operate nearly 21,000 retail outlets for fuels. These are located in the US, Europe, Australia and Southern Africa but the numbers are reducing, predominantly in the US. Air BP, is the aviation fuel arm and they sell in excess of 460,000 barrels a day. The group are in the process of exiting their LPG marketing business. The lubricant business is active in the automotive sector, under the brand of Castrol, the marine sector, where it is the largest supplier of marine lubricants in the world, the industrial sector, the aviation sector and the energy sector. The petrochemicals business has four main products – Purified Terephthalic Acid (PTA), Paraxylene (PX), Acetic Acid and Olefins. PTA is a raw material used in the manufacture of polyesters used in fibres, textiles and film and it uses PX as a feedstock. Acetic Acid is used in paints, adhesives and solvents, as well as in the production of PTA. The Olefin business if based in China. The PTA project in Zhuhai, China was progressed during the year with the below ground preparation work complete, Also, BP signed a memorandum of understanding with some local groups to explore the development of an integrated 1,4-butanediol (BDO)and Acetic Acid plant in Chongqing. The resultant plant would produce 200,000 tonnes of BDO and 600,000 tonnes of Acetic Acid a year. Progress is also being made with the joint venture with Indian Oil Corp to invest in a 1MT per annum Acetic Acid plant in Gujarat, India. The refinery integration study has been completed. Another revenue stream was realised in 2012 by licensing BP’s PX and PTA technology to third parties, with two being sold for use in India.

The replacement cost loss for Other Business was nearly $2B, compared to a loss of $1.7B last year. The result was impacted by the loss of the Aluminium business, adverse foreign exchange effects and higher costs. The Wind business brought three new wind farms into operation and now has 16 operating farms across the US. Biofuels production continued to increase with a joint venture based in Hull being commissioned that has a capacity of 420ML a year of Ethanol. The group is expanding ethanol production at its existing three sugar cane ethanol mills in Brazil and is looking to produce fuel that is competitive in an $80 Crude oil environment without subsidies. The group can also use waste products at these plants – sugar in Brazil and animal feed in Hull.

At the end of the year, BP had 52 vessels (37 medium size crude and product tankers, 3 VLCC, one North Sea shuttle tanker, eight LNG carriers, 3 LPG carriers). The group have ordered 13 new tankers to be built in South Korea, with the first one to be delivered in 2014. There are also over 100 time chartered vessels and various spot charters.

The main areas of progressed resources were Angola, Azerbaijan, Iraq, Norway, Russia, Trinidad and the US.

New exploration opportunities have been opened up in Brazil, Canada, Egypt, Namibia, Uruguay and in the US, which is a promising Shale basin in Ohio. As mentioned, production has started in two Angolan projects and a programme of exploration is continuing in the country. In Azerbaijan, two pipelines have been selected for the export of oil from the country and the West Chirag drilling platform and are on course to start in late 2013. In the North Sea there were high levels of activity where some projects were started and others sold as the group focus on high margin projects. The Gulf of Mexico continues to be considered an important part of BP’s strategy as 80% of reserves remain in the ground. It has been decided that the challenges involved in developing the Alaska Liberty Field are too high and development plans there have been suspended, as mentioned previously.

Downstream, refining and lubricants seem to be performing well, despite weak demand for the latter but margins were reduced in Petrochemicals as the group maintained their production quantities at the expense of profits . The underlying replacement cost of Fuels was just under $5B, up from $3.6B in 2011. Lubricants were up by a lesser degree, $1.3B, compared to $1.25B. Petrochemicals fared badly, however, as they were just $166M, compared to $1.1B the year before.

Crude prices in 2012 on average remained pretty much unchanged when compared to the year before with global consumption being fairly weak as demand in developing nations took the slack from lower demand in industrialised countries. The weakness in the global economy continued to create a challenging environment for downstream operations but margins did improve due to refinery closures in the US and Europe. Lower demand was caused by low economic growth, blending of biofuel products and increased car fleet efficiencies. The lubricant market was weak due to low growth and the reduction of incomes. Margins were held up by lower raw material costs, though. Demand for petroleum products reduced and new capacity came online in Asia, which caused margins in PTA and Paraxylene to be very low. Conditions in 2013 are expected to continue to be difficult, with more Chinese capacity due online.

Going forward, the group are looking to make between $24-$27B of capital investment a year until the end of the decade with around $2B-$3B of divestments to keep the cash coming and to optimise their portfolio. Production in 2013 is likely to be lower than that of last year, mainly due to the impact of business sales but four major projects are expected to come onstream towards the end of 2013. Refining margins are predicted to decline in 2013 as further capacity comes onstream and demand continues to be weak in many markets. Demand for lubricants is expected to be similar next year and capital expenditure in the downstream sector is likely to be somewhat lower than this year. The break-even point next year is likely to occur in the $80 to $100 per barrel price range.

As BP is still feeling the effects of the Gulf of Mexico spill, there is still a lot of uncertainty. This year profits halved due to less upstream revenue; increased manufacturing and inventory costs, and higher impairments. Net tangible assets were up by $4.4B due to a higher amount of capitalised exploration expenses, more plant and equipment and higher inventories. Although the cash flow was positive, this was entirely due to increased borrowing and business/asset sales. As it stood this year, capital expenditure was not covered by operational cash flow which seems rather unsustainable going forward. It is worth keeping in mind that $6.3B was used to cover the spill so one would hope that this will come down in future. It is also keeping in mind that one of the claims (by a number of US states) has the potential to hit BP for $34B, which will clearly affect the group for many years to come if it is upheld. During the year, net debt reduced by the tune of $1.4B, which is clearly a good sign, the current yield is 4.9%, which is decent but not without risk and the current P/E is a very low 7, with the P/E for next year projected to be slightly higher, at 8.5. Overall, this could be a good investment but the risk is definitely here with the potential for some huge future pay outs. On balance, I will continue to hold.

On 22nd March, BP announced that it intends to carry out a share repurchase program with a total value of up to $8B. This is an amount that is equivalent to their initial investment in TNK-BP (BP received $12.5B in cash from Rosneft for its stake, with the rest of this cash being used to reduce debt). It is intended that this program will finish within 18 months. I am not usually a fan of share buy back schemes and often think there must be better ways to invest the money but with this action, BP are intending to counteract the loss of EPS that will occur with the sale of their TNK-BP business so I guess on this occasion it does have some merit.

On the 3rd June 2013, BP announced that it had completed the sale of the Carson Refinery and SW US retail assets to the Tesoro Corp for $2.4B. Cash proceeds included $1.1B for assets and $1.35B for inventory and other working capital. This sale apparently signals the completion of the US fuels portfolio divestment. The refinery is located near LA and has a capacity of 266,000 barrels per day, so is a large outfit. The sale also included the pipelines, logistics terminals and Arco branded retail marketing network in Southern California, Arizona and Nevada. This sale was already in the pipeline so it is good to get it completed.