Interserve has now released their interim results for the half year 2013.

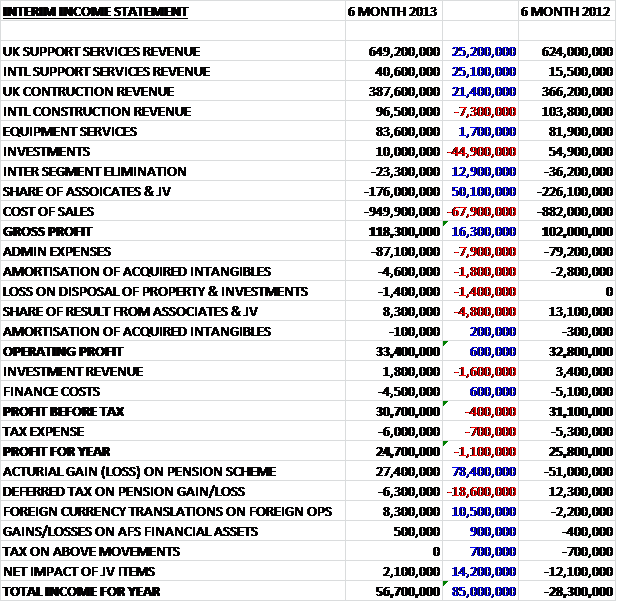

We can see that revenues in most of the business segments have increased, with international support services up by £25.1M to £40.6M. International Construction revenue fell, however, down by £7.3M to £96.5M. Revenue from investments was down substantially as the group sold off most of their PFI interests but there is also a corresponding fall in the share of revenues from joint ventures. The cost of sales were also up substantially to leave the gross profit up £16.3M to £118.3M. We can see there was a fall in the share from associates and joint ventures, presumably due to the lack of PFI income and admin expenses were up £7.9M to £87.1M. There were also one-off costs of £4.6M of amortisation of acquired intangibles and a loss on investment disposals. The resulting operating profit was similar to that of last year, up by just £600K.

A reduction in investment revenue, however, and an increase in the amount of tax paid pushed the profit for the half year £1.1M down to £24.7M. A massive actuarial gain on the pension scheme (that is where most of those sold PFI investments went) means that the total income from the year was considerably higher than last year.

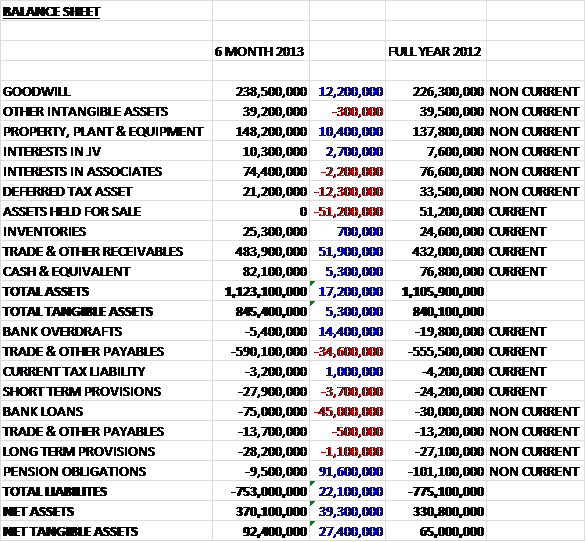

Overall assets grew by £17.2M over the position at the end point of last year. The largest movements were in Assets Held for sale, as the group sold the PFI investments (£51.2M) and a £51.9M increase in trade and other receivables. I am not sure what caused such a hike, presumably partially to do with the acquisitions. We also see a £21.3M reduction in the deferred tax assets counteracted by a £12.2M increase in goodwill, a £10.4M increase in property, plant and equipment, and a £5.3M increase in cash. Stripping out the increase in intangibles gives a small rise of £5.3M in tangible assets.

In contrast, liabilities fell by £22.1M. The major movement here was the £91.6M reduction in pension obligations which are now just £9.5M. This was because most of the PFI investments were sold to the pension scheme. There was also a £14.4M reduction in the bank overdraft but this was swamped by a £45M increase in bank loans. Trade and other payables were the other big increase, up £34.6M on the end of last year. Overall this means that net tangible assets climbed £27.4M to £92.4M so a pretty decent 6 months for the balance sheet, mainly due to the pension deficit fall.

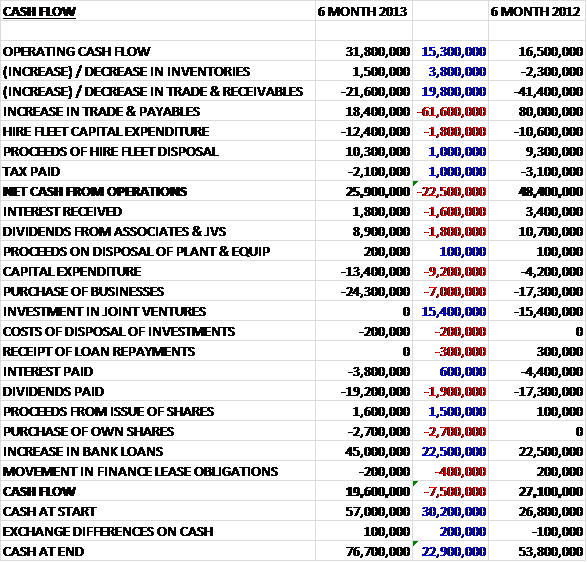

There was a fairly healthy £31.8M of operating cash flow which is reduced to £25.9M by changes in working capital, a net expenditure on the hire fleet and tax paid. This was £22.5M less than in the same period of last year due to the fact that there was an £80M increase in payables during the first half of 2012. Compared to last year there was a lower interest received and a lower dividend from associates and joint ventures. Capital expenditure was much higher than last year, up by £9.2M to £13.4M. The increase of £45M in bank loans paid for the £24.3M of business purchases and the £19.6M of positive cash flow whilst the group also managed to pay out £19.2M in dividends.

The £19.6M cash inflow in the first half of the year was very much flattered by the £45M of new debt, which also paid for the acquisitions. Were it not for these two factors, there would have been a £1.1M of cash outflow, which is not that great actually but it is important to remember that £19.2M was paid out in dividends, £1.9M more than last year.. It is also worth noting that after this was recorded, another acquisition was made in the region of $46M, which would mean that cash flow for the full year is likely to be rather negative.

Geographically, by far the largest amount of revenue received was in the UK. The region was also very important for profit, contributing £34.1M in the 6 month period (compared to £30.5M in the first half of last year). The next largest region, MENA accounted for £12.4M, an increase of £1M. Oceania contributed £4.1M, a reduction on last year and the Far East only contributed £700K, £1M down from H1 2012. The rest of Europe and the Americas actually made a loss.

During the period there were two acquisitions. In January, the group acquired Willbros Middle East Ltd which owned 85% of two oil and gas services businesses, the main one being The Oman Construction Company (TOCO) for a total consideration of £25.7M. The second acquisition was much more minor. In May the group acquired Paragon Management UK Ltd, a specialist interiors and property refurbishment business for a consideration of £3M. TOCO came with £11.8M of net assets (£4.9M intangible) and Paragon £2.6M (£400K intangibles). After the end the period, another acquisition was made. In July the group acquired Topaz Oil and Gas which provided oilfield maintenance, fabrication and construction services to the Middle East. The total consideration is expected to be $46M.

Support Services in the UK grew revenues by 4.4% and profits by 29.1% and showed an improved margin of 4.2%. Organic profit growth was bolstered by new contracts in the nuclear, defence, healthcare and public sectors with some extra coming from the recent acquisitions. Future workload for the division increased to £5.4B. About 2/3 of revenue comes from the public sector with major clients the MOD, Magnox, DEFRA, NHS, Scottish Power, East Thames Group, Sainsbury, Carphone Warehouse and Alliance Boots. A highlight was the £700M seven year contract with NHS Leicestershire to provide estate management, rationalisation and modernisation for three NHS trusts. Another seven year contract was with East Thames to provide a repairs and maintenance service to the group’s 13,500 households.

Internationally, Support Services more than doubled revenues and increased profit by 50%. Future work load more than doubled to £159M at the half year point. The major contributor to this increase was the TOCO acquisition. The principle focus is on the oil and gas industry and there is considered to be growth potential there. TOCO has added strong work-winning contracts valued at about £34M. A highlight was a three year oilfield services contract worth £30M to construct and maintain pipelines in Northern Oman. Madina won a long term mechanical services contract with Shell Pearl in Qatar and Khansaheb secured contracts for the provision of facilities management to Habib bank in Dubai and Estate management at Monte Carlo Beach Club in Abu Dhabi.

UK Construction increased revenues by 5.8% and profits rose 1.4% to £7.4M with a stable future workload of £950M. A significant new revenue stream was achieved with the construction of energy from waste plants with construction taking place in Glasgow and Peterborough. The value to the group of this contract is about £15M. The acquired Paragon group won a £6M contract from HM Courts and Tribunal Service. In Education, new projects were awarded by Middlesbrough College and Portsmouth Charter Economy. In Health, new projects were won with Mid Cheshire Hospitals and Hywel Dda Health Board. A contract was secured with Jaguar Land Rover to build their Engine plant in Wolverhampton. There were also new awards from Viridor, United Utilities, SW Water, SE Water, Affinity Water, Cornwall County Council and the Highways agency.

The Middle East construction business continued to find the market difficult but there were early signs of an upturn in the UAE. Greater demand was also showing in the Americas and Far East. Oceania, however, saw demand weaken from historic highs. Revenue was down 7% and profit fell by 18.6% to £5.7M. Future Workload remained stable at £200M. There appears to be some sign of an upturn in the UAE with previously mothballed developments starting up again and new developments in the commercial and leisure sectors. Slow progress on contract wins in Qatar hampered market activity but there has been recent progress in significant civil engineering contracts for rail and roads. Oman offers a good prospect for growth from the recent acquisitions. Progress in the Indian construction market has been slow and the group has taken the decision to exit that market resulting in a write-off of £5M. Highlights over the half year have included a contract for the construction of Lusail tower in Qatar and the installation of a desalination plant in the same country. In Dubai, contracts were won with the Office of the Crown Prince of Dubai, EMAAR restaurants, Majid Al-Futtaim (retail), Chalhoub Group (retail), the Government of Fujairah (roads) and the Dubai Festival Club (retail). In addition, a contract to construct a GE Emirates Engine maintenance centre in Dubai; fit out work for the Four Seasons Hotel and road and infrastructure work for Meraas was gained.

In Equipment Services, revenues were up 2.1% and profits increased by 25% to £8.5M due to pricing improvements and operational efficiency. There were new expanded capabilities in Philippines, Singapore, Colombia, South Africa, Iraq, US and Mozambique. There was strong demand in Saudi Arabia and Qatar showed signs of an upturn. Demand weakened in Australia, however, as a number of significant natural resources projects were delayed. Market conditions in the UK and the rest of Europe remained difficult. Highlights included framework on the largest coal bunker in South Africa at the Grootegeluk mine; heavy duty shoring equipment was used on the Isa Gate Flyover in Bahrain, framework used on the air traffic control tower in Muscat Airport, Oman, the use of a safety screen on the construction of a new residential tower in Canada Water, London and equipment used in the construction of bridges linking Jubail with Ras Al Kahair in Saudi Arabia.

So, revenues increased across most of the businesses with the exception of International Construction. The support services seem to be entering into some good, long term contracts and the equipment services business seems to be doing well to improve margins. The subdued construction market in the Middle East and Australia are of some concern and it is disappointing to see the group exit India, which I would have thought could have provided some good long term returns even if short term profits were hard to come by. Profit for the year fell by £1.1M due to reduced investment revenues, presumably due to the PFI investments being sold to the pension scheme. That transaction, however, made a serious improvement with the look of the balance sheet, however, as the pension deficit was reduced dramatically. In fact, net tangible assets increased by £27.4M which seems very impressive.

Cash flow was OK. Dividends were nearly covered by the cash generated by the group, with a bit more coming from new borrowings. In fact, borrowings were up substantially to pay for the acquisition spree that Interserve seems to be on. Having said that, at the half year point net debt was a negligible £700K (although that will change once the Topaz acquisition is taken into account). The dividend yield stands at 3.8%, and although the mega returns available a year or so ago are no longer present, this still represents a decent yield. In the medium term, it will be interesting to see how the group adjusts from the move away from PFI contracts to Middle East oil and gas services but at the moment I think the shares are at a fair price.

On 14th August the group announced that it had been awarded a contract extension with the MOD worth £110M. The contract runs until July 2014 with an option to extend for a further 6 months and involves managing military training facilities across the MOD’s training estate. It is an extension of a contract that has been in place since 2003 so has been long term so far and covers more than 120 sites and 8,000 buildings.

On 17th October, Interserve announced that they won a new five year contract to supply service management to the BBC. The contract is worth £150M and involves supplying over 150 UK facilities with critical broadcast engineering and business continuity services. This contract follows the current construction contract the group had with the BBC that was worth £40M. This is clearly a substantial win, obviously the margin is unknown but this is a good boost to Interserve.

On 13th November, the group released an interim trading update. It is noted that they completed the acquisition of Topaz Oil and Gas Services in September but that market conditions remained mixed. Overall, performance was in line with expectations with strong growth in UK Support Services and Equipment Services and a resilient performance in the construction business. This offset lower than expected activity levels in the Middle East oil and gas services business. In the year to date the group won over £1.8B of work from clients including the Ministry of Justice, BBC, Foreign and Commonwealth Office, Defence Infrastructure Organisation, Nottingham University Hospitals NHS trust, Arabtec Corp (Qatar), Majid Al Futtain (UAE), Qatar National Bank and Doha Festival City. This is a decent update but the down turn in the Middle East oil and gas business is a bit of a disappointment.

On 25th November the group announced that it formed a partnership with the University of Sussex to provide a 10 year facilities management contract to the university. The contract is worth £150M so is quite substantial and will commence at the start of 2014. The group will provide various services to the university including cleaning, grounds maintenance, buildings management, portering, mailroom, security, car parking, waste management, health and safety support, project management and energy saving improvements. Some improvements that are being introduced are a reduction in carbon emissions, a new helpdesk staffed 24/7 and investments in skills development. One other nice touch is that six undergraduates will be given the opportunity to work on the contract each year as trainee managers.

On 8th January the group released a trading update. It stated that they have continued to perform well and in line with expectations. Short and sweet!

On 28th February the group announced that they had entered a conditional agreement with a subsidiary of Rentokil Initial to acquire its facilities services business for a cash consideration of £250M. The transaction will be funded partly by a new placing of shares which should raise about £70M and represents nearly 10% of the current share capital, along with new debt. The acquired business has operations in the UK, Spain and Ireland and employs about 25,000 people. The services offered include cleaning, catering, security, mechanical & electrical building maintenance, energy management and statutory compliance. Their client base is also more skewed towards the private sector than the current situation at Interserve and the enlarged group should have a close to 50/50 split between the private and the public sector.

The resultant group will become one of the top three (by revenue) providers of support services in the UK (I assume I also own shares on one of the other top three, Compass). The main reason for the acquisition is the increased market that it opens up for the group, but the board also expect to achieve synergy costs of about £5M by the end of 2015. The underlying operating profit before amortisation for the acquired group was £25.6M and the board expect the acquisition to be earnings enhancing within a year despite the £10M in one-off exception costs associated with the purchase. This bid is large enough to require shareholder approval but given the group currently has negligible net debt, I see this as a decent opportunity for expansion.