Keller has now released their final results for the year ending 2015.

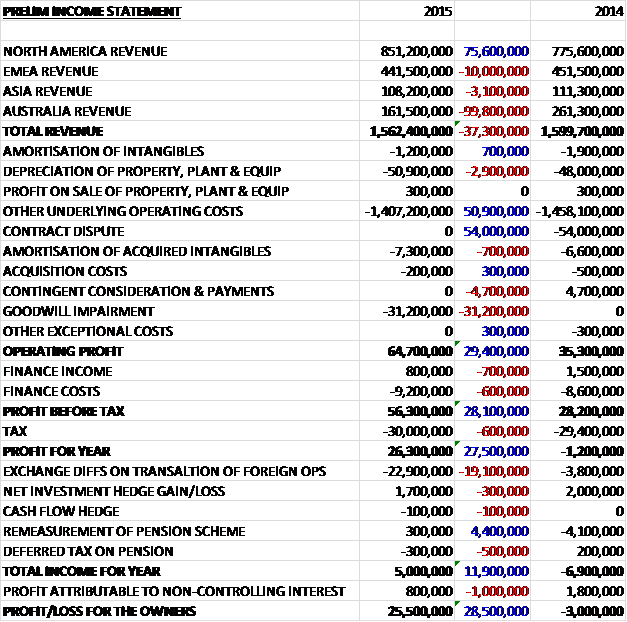

Revenues fell when compared to last year as a £75M growth in North American revenue was more than offset by a £99.8M decline in Australian revenue, mainly as a result of the completion of the Wheatstone contract; a £10M fall in EMEA revenue due to weakness in the Euro and a £3.1M decrease in Asian revenue. Depreciation increased by £2.9M but other underlying operating costs fell by £50.9M. We also see no contract dispute costs which were £54M last year but there was a £31.2M goodwill impairment and no contingent consideration payment which was an income of £4.7M in 2014 so the operating profit was some £29.4M above that of last year. Finance costs and tax were both modestly higher, the former due to lower non-cash income from financial assets, which gave a profit for the year of £25.5M, an improvement of £28.5M year on year.

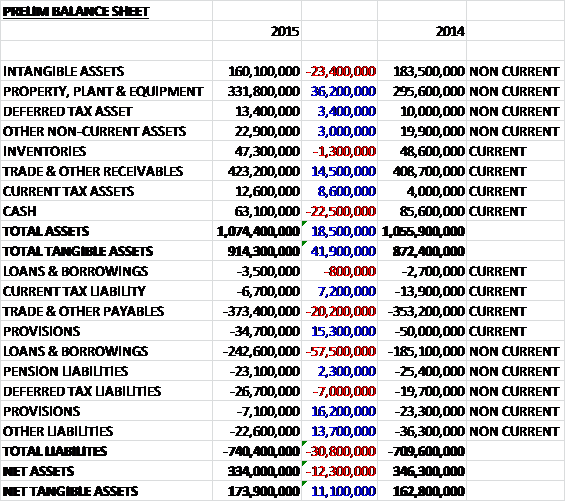

When compared to the end point of last year, total assets increased by £18.5M driven by a £36.2M growth in property, plant & equipment, a £14.5M increase in receivables, an £8.6M growth in current tax assets and a £3.4M increase in deferred tax assets, partially offset by a £23.4M decline in intangible assets and a £22.5M decrease in cash. Total liabilities also increased during the year as a £58.3M growth in borrowings, a £20.2M increase in payables and a £7M growth in deferred tax liabilities were partially offset by a £31.5M fall in provisions, a £13.7M decline in other liabilities and a £7.2M decrease in current tax liabilities. The end result is a net tangible asset level of £173.9M, a growth of £11.1M year on year.

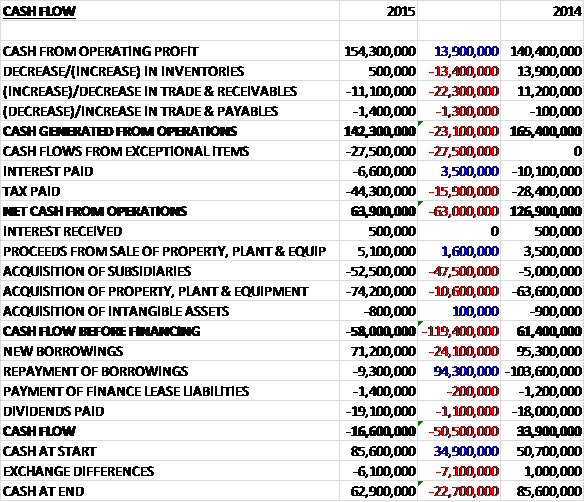

Before movements in working capital, cash profits increased by £13.9M to £154.3M. There was a cash outflow through working capital compared to an inflow last year and there was also a £27.5M payment relating to the contract dispute provided for last year and a £15.9M increase in tax paid to give a net cash from operations of £63.9M, a decline of £63M year on year. The group spent a net £69.1M on property, plant & equipment and £52.5M on acquisitions so that before financing there was a cash outflow of £58M. The group took out a net £61.9M of new borrowings and paid £19.1M in dividends so that there was a cash outflow of £16.6M to give a cash level of £62.9M at the year-end.

In the US, expenditure on construction increased significantly for the fourth consecutive year with good growth in most segments of the market. Private non-residential construction grew by 12% whilst in the residential market housing starts were up 11% year on year with strong growth in both single family and multi-family homes. Growth in public expenditure on construction continued, up 6% on 2014. In Canada construction activity in the resources markets remains very subdued although demand in the commercial and infrastructure segments fared somewhat better.

Conditions in European markets remained mixed with Southern Europe in particular remaining challenging. There are some positive signs in the Central European markets of Germany, Poland and Austria as well as in the UK. Elsewhere there are good opportunities in the Middle East where construction markets have been relatively unaffected by the low oil price. The construction market in South Africa is slowing and whilst there are some good opportunities elsewhere in Africa, a number are in the oil and gas sector so their timing is uncertain. Globally the group’s direct exposure to the oil and gas projects was 6% of revenue.

Construction expenditure in the group’s Asian markets remains varied. In India they are continuing to see signs of increasing business confidence but the Singapore and Malaysian markets are relatively quiet. In Australia, construction expenditure across most segments has been subdued for some time and is showing few signs of improving. An exception is the near-shore marine segment where there remain a number of projects to upgrade or expand ports and harbours.

The operating profit in North America was £76.4M, a growth of £16.5M year on year with an operating margin that increased from 7.7% to 9%. The US business had a very strong second half, building on the good progress made in the first half as construction activity continues to improve across the country. The largest North American business, Hayward Baker, had a good year. The business improved its results despite having fewer major projects.

The US piling companies performed very well, particularly Case and HJ Foundation which had record years on the back of strong regional markets and an excellent performance on a number of large projects. Highlights for Case included major projects working on the installation of catenary poles on rail lines and at a hydroelectric plant at Red Rock Dam in Iowa whilst HJ Foundation benefitted from buoyant conditions in its domestic South Florida market, completing the foundations for a number of projects in Miami.

Bencor, the diaphragm wall company acquired in August, has been integrated into the group and work on its $135M project to repair and upgrade the East Branch Dam in Pensylvania is progressing to plan. Suncoast, the post-tension business which mainly serves the residential construction market recorded a strong performance, taking advantage of the increase in housing starts in the year.

Keller Canada has struggled in very difficult market conditions but managed to record a small profit, helped by reductions in overheads. Despite much reduced revenue, gross margins held up OK and the business performed the only major piling project in the year in the Alberta oil sands. On a more positive note, the business has just been awarded a C$34M technically demanding project in Toronto in connection with the expansion of the city’s metro system.

The operating profit in EMEA was £21.3M, an increase of £8.4M when compared to last year with operating margins that increased from 2.9% to 4.8% reflecting the benefit of continuing business improvement initiatives and a good performance on their major contract in the Caspian region along with an excellent performance in the Central European business and a strong result from Franki Africa.

Despite the mixed market conditions in Europe, the business improved their results through a focus on cost control, risk management and careful contract selection. The business in Central Europe underpinned this improvement. The Polish business benefited from the infrastructure investment in the country and was recently awarded a €17M ground improvement contract in connection with the upgrade of the S7 motorway in the north of the country. Germany reported an excellent result and the group’s Austrian business performed well in a competitive market, making good progress on the €31M St. Kanzian contract, the major grouting project on the Koralm railway line between Graz and Klagenfurt.

The UK business also had a better year in 2015, working on a wide variety of commercial and infrastructure projects and much effort is being devoted to ensure the group secures significant work on the major infrastructure projects scheduled for the next few years in the country. Conditions in the larger markets in Southern Europe remain very challenging. The French market remains subdued whilst volumes in Spain are at very low levels.

Competition in the Middle East remains tough but the group increased profit in the region. This performance was aided by a good result in Saudi Arabia and a number of contract wins in Qatar. Franki Africa had a good year, significantly increasing both revenue and profit on the back of a strong performance in South Africa and the successful completion of Ada Phase 2, a major jetty project off the coast of Ghana.

The operating profit in Asia was £4.5M, a decline of £3.8M year on year with an operating margin that declined from 7.5% to 4.2%. After a disappointing first half, both revenue and profit picked up significantly in Asia in the second half of the year following a break-even performance in H1.

Despite a much improved second half, the ASEAN business as a whole had a disappointing year with revenue broadly flat and profit much reduced. In Singapore the market was quiet with no growth in commercial construction and a virtual stop in projects for the oil and gas industry. In addition, they suffered from significant delays on their major vibro-compaction contract at Changi airport for reasons beyond their control.

The Malaysian construction market slowed significantly in the year as a result of the fall in the oil price. This slowdown, combined with a delay on one of the larger projects meant that the traditional Malaysian business had a disappointing year. Ansah, the small driven piling business acquired in 2014, however, far exceeded board expectations, winning some substantial work on the RAPID petrochemical complex being constructed by Petronas in the SE of the county. In total their work on RAPID will total nearly $50M.

Towards the end of the year the group won their first major ground improvement project in Indonesia. This is a $25M contract to provide vibro-compaction works at Pluit City, a newly created group of islands near Jakarta. The Indian business performed well in the year, aided by an improving construction market. The business has entered the near-shore marine construction market, using some of the existing expertise in Australia.

The operating profit in Australia was £7.2M, a decrease of 8.5M when compared to 2014 with margins declining from 6% to 4.5%. This reflects a very difficult market for the traditional foundation business and having no replacement contract of near equivalent sixe for Wheatstone. In response to the difficult market, the group is merging its three piling businesses into one. This is proceeding to plan and has apparently been well received by customers. As a result of this, and other cost cutting measures, they have reduced their Australian overheads by A$7M on an annualised basis.

In contrast to the construction market as a whole, the near-shore marine segment has remained robust and the business focusing on this segment performed well. Waterway had an excellent year and Austral, which was acquired in July, has had an encouraging start as part of the group. In the last two months, the Australian business has won two large projects – they construction of Mayfield No7 wharf for A$43M in Newcastle, NSW and the foundations for the next phase of a major commercial development in Sydney for A$37M. As a result of these, along with the acquisition of Austral, the Australian order book is now 20% higher than this time last year.

With effect from the start of 2016, the Asia and Australia divisions were merged to create a new Asia-Pacific division under one leadership team headquartered in Singapore and going forward they will report their results in three divisions, which is a bit of a shame in my opinion.

There were a number of exceptional items that are recorded on the income statement. This year the most important one is the £31.2M goodwill impairment relating to Keller Canada whose results have been below those expected at the time of the acquisition, mainly due to a severe slowdown in investment in the Canadian oil sands following the reduction in the price of oil. There remains £27.6M of goodwill in the Canadian business.

Last year there was a £54M charge for a contract dispute relating to a project that the UK subsidiary completed in 2008. The dispute was subject to litigation proceedings involving a number of parties but these were settled in February 2015. The exceptional charge represents management’s best estimate of the net cost to the group before taking account of future recoveries under insurance. During this year, they paid a net £27.5M in cash relating to the dispute and the remainder of the costs are expected to be mostly incurred in 2016.

The group have continued to invest in new facilities and equipment in Renchen, Germany and have added a new manufacturing hall to enable them to raise output and build the vibro and grouting machines of the future. In all, they have made capital investments well above depreciation during the year.

The group made three acquisitions during the year. In July they acquired Austral Construction, a business based in Melbourne, Australia for a total consideration of £26.5M consisting £19.9M in initial cash and £6.6M of contingent consideration which generated goodwill of £6.7M. In August they acquired Bencor, a business based in Dallas, USA. The group paid £29M in cash and the transaction generated goodwill of £3.2M. Also in August the group acquired Ellington Cross, a business based in Charleston in the US for a cash consideration of £1.9M with goodwill of £200K generated. In the period to December the three business generated £500K of net profit to the group.

Last year, Justin Atkinson retired as CEO and he was replaced by Alain Michaelis in May 2015. Following this, chairman Roy Franklin has decided to retire in 2016 having been with the group since 2007 and Chairman since 2009.

At the end of January the group order book of work to be undertaken over the coming year was 15% higher with increases in all divisions. Whilst conditions in their market are varied, the ongoing strength in the US, the largest market, continuing improvements in operating performance and the strong order book mean that the board are confident of another year of progress in 2016 and results are expected to be in line with expectations.

The year-end net debt was £183M compared to £102.2M at the end of last year. This increase reflects the £52.5M spent on acquisitions and a £27.5M cash outflow relating to the troublesome contract provided for last year along with a growth in capex. At the current share price the shares are trading on a PE ratio of 10.4 which falls to 8.6 on next year’s forecast. After a 7.5% increase in the total dividend, the shares are yielding 3.3% which increased to 3.5% on next year’s consensus forecast.

Overall then this has been a solid year for the group in some rather tough markets. Excluding the contract dispute and goodwill impairment, profit increased year on year and net tangible assets also grew. The operating cash flow did decline, but this was mainly due to a reversal of the favourable working capital movements last year along with the payments relating to the disputed contract and cash profits grew. Due to the above issues, there was no free cash flow generated.

North America saw a strong performance, particularly in H2 as the construction market in the US showed good growth, although this was somewhat offset by a difficult environment in Canada driven by the fall in the oil price. The EMEA business also performed well due to a lucrative Caspian contract and a strong performance in Germany and Poland, partially offset by weakness in Spain and France. The Asian business found going difficult, although trading did improve in the second half of the year. Both Singapore and Malaysia were affected by the declining oil price and delays in some large contacts. Conditions in Australia were difficult and profit here fell due to a subdued market and the end of the Wheatstone contract.

Of the acquisitions, the Australian Construction company purchase looks a little mis-timed and expensive, although the US business look better – the acquisitions did not really contribute much to the results this year. In conclusion then, the order book is up and the all-important US construction market shows no signs of weakness, although other areas are more problematic. With a forward PE of 8.6 and dividend yield of 3.5% these shares look cheap to me unless there is a prolonged slowdown in the States and I have decided to buy in here.

On the 29th April the group appointed Peter Hill as non-executive Chairman to succeed Roy Franklin who retires in July. Peter is currently Chairman of Volution Group and non-executive director at Essentra and the Royal Air Force. Previously he has been CEO of Laird.

On the 13th May the group announced that it had acquired the freehold of a processing and warehousing facility near Bristol for £62M from GJ ltd, pursuant to a settlement agreement in connection with the previously announced contract dispute arising on a project completed in 2008. Keller’s final liability from this dispute is in part dependent on the value of the property after some remedial works and in order to maximise this value, the board have decided to acquire it now with a view to marketing it to third parties imminently and the intention of completing a sale before the end of the year.

The facility is fully operational, has a tenant on a long term lease and the acquisition price represents an annual rental yield of 6.8%. The group expects to recoup most, if not all, of the purchase price on sale and management is confident that the existing provision in respect of this settlement will prove more than adequate. The purchase has been largely financed by a new bank facility raised for this purpose and will have no impact on trading.

On the 24th January the group released a trading update for the year to date. There has been no significant change in market trends since the last report. For the group as a whole, both revenue and profit in the first four months of the year are slightly above last year. They have seen good performances from their North American and EMEA divisions but this has been offset by a disappointing performance in Asia Pacific. Tendering activity and contract awards are generally healthy. At the end of April, the order book of work undertaken over the next year was 15% higher year on year. Looking ahead, the group remains on course to meet the board’s expectations for the full year.

In North America, the total US construction market continues to grow steadily, with both private and public expenditure on construction in Q1 up on the comparable period of 2015. The group’s US business has had a good start to the year and bidding activity across the country remains robust. The Canadian business continues to operate in a difficult market but results will improve due to the seasonally better second half as the business starts to work on a number of large jobs.

In Europe, conditions in the larger construction markets remain stable whilst in the Middle East, despite construction activity levels remaining healthy, the group have seen some projects delayed as a result of the low oil price. The main European businesses in the UK, Germany, Poland and Austria have all had a good start to the year but elsewhere trading has been mixed, despite good progress being made on the large contract in the Caspian region.

The Asian Pacific markets of Australia, Singapore and Malaysia have been very challenging with volumes well down on the levels of recent years. Whilst trading in India has been solid, elsewhere the group has suffered from reduced revenue. This reflects both the depressed market conditions and delays in the start dates of certain large projects. As a result the board expect the Asia Pacific region to record a loss in the first half of the year. They continue to reduce their cost base, however, and with an order book well ahead of last year, the second half will see a significant increase in revenue and a return to profitability.

Apart from the £62M property acquisition, there has been no material change in the financial position of the group.

Overall then, the poor performance in Asia is disappointing but the improved order book means the second half should improve. I will continue to hold.

On the 25th May the group announced that non-executive director Peter Hill had purchased 10,000 shares at a value of £93,404. This represents his first share purchase.