Central Asia Metals has now released its final results for the year ended 2016.

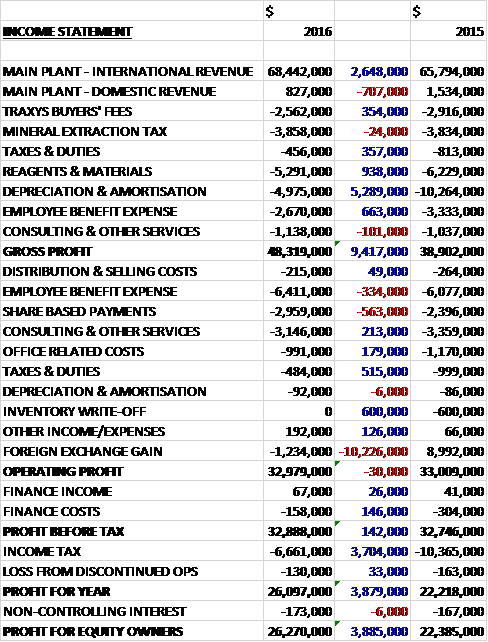

Revenues increased when compared to last year as a $707K decline in domestic revenue was more than offset by a $2.6M growth in international revenue. Buyers fees fell by $354K, taxes and duties were down $357K, reagents and materials declined by $938K and depreciation and amortisation decreased by $5.3M following the extension to the life of the mine at Kounrad,to give a gross profit $9.4M above last year. Share based payments increased by $563K but taxes and duties declined by $515K and there was no inventory write-off which accounted for $600K last year. There was a $10.2M adverse swing to a forex loss, mainly due to last year’s devaluation of the Tenge, however, which meant that the operating profit was flat on last year. We then see a $146K reduction in finance costs and a $3.7M decline in income tax charges, mainly relating to a deferred tax credit this year (something to do with depreciating the Kounrad assets since the date of the acquisition following the increase of the fair value of the assets), so the profit for the year came in at $26.3M, a growth of $3.9M year on year.

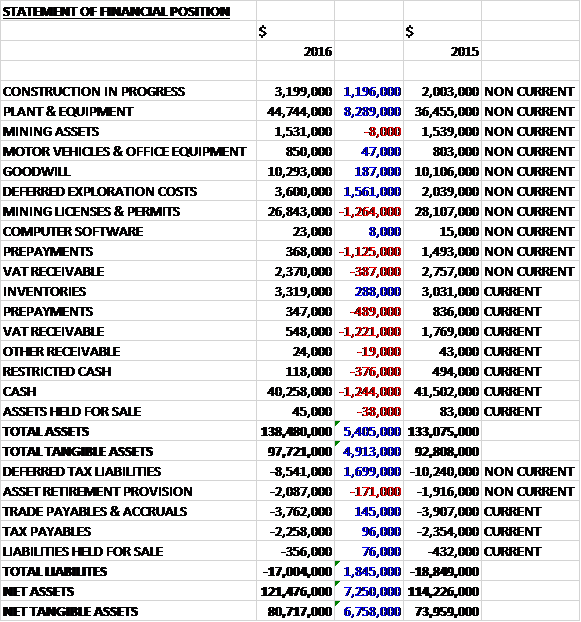

When compared to the end point of last year, total assets increased by $5.4M driven by an $8.3M growth in plant and equipment, a $1.6M increase in deferred exploration costs and a $1.2M growth in construction in progress, partially offset by a $1.2M decline in cash, a $1.2M fall in VAT receivable, a $1.3M decrease in mining licenses and permits and a $1.6M decline in prepayments. Total liabilities declined during the year, mainly as a result of a $1.7M decrease in deferred tax liabilities. The end result was a net tangible asset level of $80.7M, a growth of $6.8M year on year.

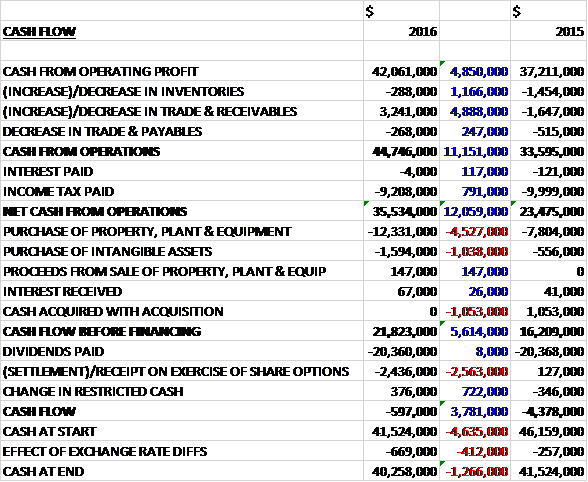

Before movements in working capital, cash profits increased by $4.9M to $42.1M. There was a cash inflow from working capital and after tax payments fell by $791K the net cash from operations came in at $35.5M, a growth of $12.1M year on year. The group spent $12.3M on property, plant and equipment along with $1.6M on intangible assets to give a free cash flow of $21.8M. Most of this ($20.4M) was paid out in dividends but $2.4M was used to settle share options so there was a cash outflow of $597K for the year and a cash level of $40.3M at the year-end.

Last year was another challenging year for the copper price with it reaching seven year lows of $4,311 per tonne in January 2016. The price increased in Q4, ending the year at a price of $5,500 per tonne. The movement seemed to signify renewed positive market sentiment and that outlook has continued into 2017.

The pre-tax profit from the Kounrad operation was $46.1M, a growth of $2.4M year on year. The total production was 14,020 tonnes with the total quantity of copper being sold 13,938. This represents an increase of 1,949 tonnes and 1,898 tonnes respectively. The average gross price achieved from the sale of copper was $4,994 per tonne compared to $5,336 per tonne last year.

C1 cash costs were around $0.43 per pound compared to $0.60 last year (why we can’t have these in per tonnes I really don’t know). The decrease was mainly due to the devaluation of the Tenge in August 2015 since when it has remained relatively stable. There was also very little in the way of inflation on the expenditure at Kounrad.

In Q4 the group materially completed its stage 2 expansion on schedule, ab out 30% under budget. This expansion will enable them to start leaching operations in the Western Dumps in Q2 and in doing so, has extended the life of the operation to beyond 2030. The devaluation of the currency played a significant part in the reduced capex against budget but they also secured some cost improvements based on revised engineering solutions.

The pre-tax loss at the Cooper Bay operation was $799K, an increase of $71K when compared to last year. The team has demonstrated that there is a project worth $34.1M based on a copper price of $3 per pound. Given the current uncertainty with regards the near and medium term expectations for the metal, the board has recommended that the project remains in the development pipeline while they review their options.

In November they signed a framework agreement to acquire an 80% effective interest in the Shuak copper exploration property in northern Kazakhstan which has the potential to host significant copper oxide mineralisation to which they can apply their experience from Kounrad. They intend to start field-based exploration work in Q2 and during the 2017 exploration season, they plan to implement a 1,800m trenching programme and to undertake 22,000m of drilling. The exploration budget is about $1.3M.

Following the receipt of the regulatory approvals required for the Kounrad Stage 2 expansion in November 2015, management has extended the useful economic lives of certain property, plant and equipment. The original estimate of ten years of useful economic life has now been increased through to 2034 which represents the end of the subsoil user license. This change was applied from the start of 2016 and has resulted in a reduction in the depreciation charge.

At the year-end the group was owed $2.8M in VAT receivables. Since the year-end an amount of $238K has been paid and the group are working closely with their advisors to recover the remaining portion. The planned means of recovery will be through a combination of the local sales of copper cathode to offset the VAT liabilities and by a continued dialogue with the authorities.

In December the group signed an agreement to sell its entire interest in Monresources in Mongolia for a cash consideration of $100 and deferred consideration depending on future events. Following unsuccessful attempts to dispose of the Ereen project, the group has taken the decision to exit its position in Zuunmod. After the period end, under the terms of the Shuak framework agreement, the group reduced its interest in Shuak to 80% with 20% being held by local partners.

Going forward the group has a cooper production target of 13,000 to 14,000 tonnes. Leaching from the Western Dumps is on track to start in April and the Shuak exploration programme will commence in Q2. Over the coming years, the proportion of copper that is produced from the Eastern Dumps will fall as production from the Western Dumps gradually increases.

This will result in slightly higher electricity consumption and additional labour to manage the Western Dump operations. After completing the stage 2 expansion capex programme the group are now fully invested at Kounrad with only annual sustaining capex at a cost of about $2M going forward.

At the current share price the shares are trading on a PE ratio of 12.8 which falls to 9.8 on next year’s consensus forecast. After a 24% increase in the total dividend, the shares are yielding 6.6% which increases to 7% on next year’s forecast. The net cash position at the year-end was $40M compared to $42M at this point of last year.

On the 4th April the group released a Q1 production update. Copper production was 3,357 and sales were 2,839 tonnes compared to 3,207 tonnes and 2,550 tonnes respectively in Q1 2016. During the quarter the group carried out a piping modification that allowed the operation of a hybrid intermediate leaching circuit, enabling a higher overall recovery of copper from the covered winter block. The impact of the PLS grade into the SX-EW plant was positive and resulted in a record copper output for the month of February of 1,074 tonnes.

The renewal of 850 cathodes in the EW facility as partial replacement of the circuit inventory was undertaken during the quarter. A further 1,400 pieces are expected on site in July and will be fitted shortly afterwards, thus completing the first five year replacement programme of all anodes and cathodes. Full preparations were undertaken on the Western Dumps pipeline and pumping system in readiness for commissioning of the stage 2 expansion in April. Taking seasonal variations into account, the group is on track to achieve its 2017 copper production guidance of between 13,000 and 14,000 tonnes.

Overall then this has been a good year for the group. Profits did rise but this was really only because of a deferred tax credit and otherwise they would have been flat. Net assets increased, however, and the operating cash flow grew with generous amounts of free cash being generated. The average price obtained for the copper wasn’t great, a $4,994 per tonne but the fact that it is now around $5,730 bodes well for this year. The production and sales of copper both increased during the year.

The stage 2 expansion seems to have been completed without a hitch and this should be the end to the high levels of capex being spent on Kounrad which should enable to group to move on with some other projects. Looking at the wording being used, the Copper Bay projects looks fairly unlikely to go ahead at the moment but the Shauk project looks to be progressing. The Western Dump costs will add a bit to the operating costs but while the Tenge remains devalued, the cost levels are actually very good here. I continue to hold.

On the 5th July the group released an operations update for the first half of the year. Copper production was up 2% to 7,027 tonnes with production in Q2 of 3,670 tonnes. In April the group begun irrigating the Western Dumps and during Q2 about 1,300 tonnes of copper cathode have been recovered. In the first half the group saw sales of copper cathode increased by 8% to 6,870 tonnes.

They have been undertaking geological mapping and is nearing completion of a TEM-FAST geophysics programme, which has been designed primarily to ascertain the depth and extent of the saprolite weathering horizon. The 2017 drilling programme of about 4,700 metres has recently started together with an initial 7,000 metre CHT drilling programme.

As of the period-end the group had net cash of $41.7M and they are on course to achieve their full year production guidance of between 13,000 tonnes and 14,000 tonnes of copper cathode. All seems to be ticking along OK here. Following the recent price reduction I am tempted to buy some more actually.