Wentworth Resources has now released its final results for the year ended 2016.

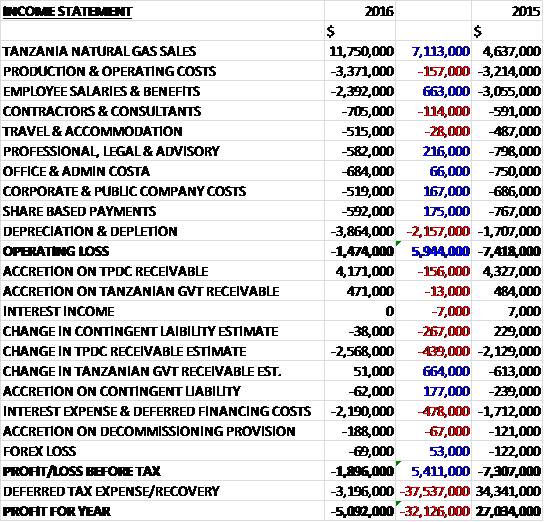

Revenues increased by $7.1M when compared to last year due to the start of gas sales to the new pipeline in Q3 2015. Staff costs declined by $663K and professional fees were down $216K although some may have been capitalised following their appointment as operator of the Rovuma block in Mozambique, but depreciation and depletion grew by $2.2M to give an operating loss $5.9M lower than last time. There was a $267K increase in the contingent liability estimate, a $439K decline in the TPDC receivable estimate relating to the lower gas demand projections and hence the slower receipt of the receivable, and a $478K growth in interest expense, partially offset by a $664K increase in the Tanzanian government receivable to give a pre-tax loss of $1.9M, a positive movement of $5.4M year on year. There was also a $3.2M deferred tax charge to give a loss of $5.1M for the year.

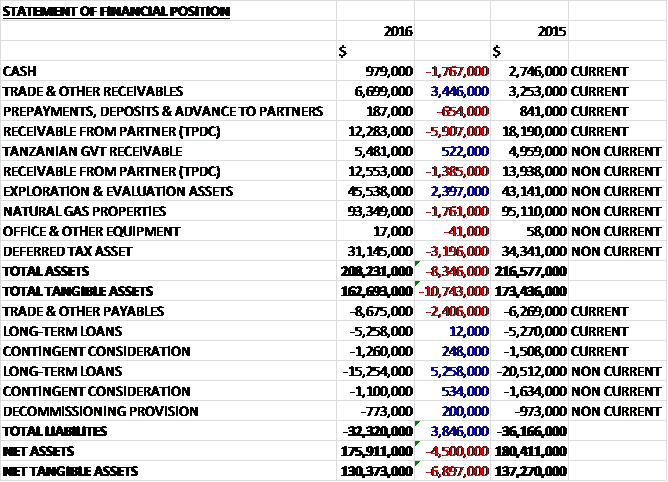

When compared to the end point of last year total assets declined by $8.3M driven by a $3.2M fall in deferred tax assets, a $7.3M decrease in TPDC receivables, a $1.8M decline in natural gas properties and a $1.8M decrease in cash, partially offset by a $2.4M growth in exploration and evaluation assets and a $3.4M increase in trade receivables. Total labilities also declined during the year as a $5.3M fall in long term loans was partially offset by a $2.4M growth in payables. The end result was a net tangible asset level of $130.4M, a decline of $6.9M year on year.

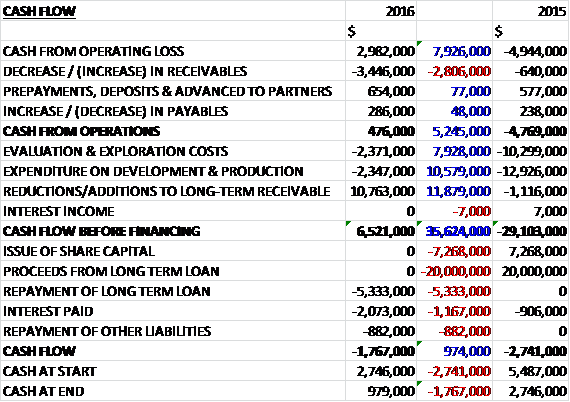

Before movements in working capital, there was a $7.9M positive swing to a $3M cash profit. There was a cash outflow from working capital due to an increase in receivables so there was a $476K cash flow from operations. The group spent $2.4M in exploration, mainly relating to operator overheads and exploration drilling in Mozambique and $2.4M on development and production mainly relating to the field infrastructure connection work in Tanzania. They also received $10.8M from the outstanding receivables to give a free cash flow of $6.5M. The group had to pay $2.1M on interest and $882K on other liabilities and then repaid $5.3M of loans to give a cash outflow of $1.8M and a cash level of $979K at the year-end.

The pre-tax profit of the Tanzania operations was $1.5M, an improvement of $3.3M year on year. The Mnazi Bay field achieved average gross daily gas production of 43MMScf per day compared to 15.7MMscf in 2015. The expansion of the liquid separation units and gas processing facilities was ongoing during the year with commissioning expected in Q2 2017.

Gas sales to TPDC increased by 203% to 3,551,575MMBtu at a price of $3.01 per MMBtu which was broadly the same as last year. Gas sales to Tanesco fell by 4% to 200,259MMBtu at a price of $5.36 per MMBtu, also remaining the same. The total production volume represented a 166% increase to 3,667,482Mscf with costs falling by 60% to 92c per Mscf.

During the year gas was used to fuel three power stations located in Dar es Salaam: Kinyerezi-1, Symbion and Ubungo-II. The group had initially expected gas demand to be between 70 and 80MMScf per day but certain events impacted the ability to reach these volumes. During July, operations at the Symbion power plant were suspended as a result of a dispute with the government, effectively eliminating 20MMscf/d of gas demand. Also during July the government began allocating 15MMscf/d of demand to industry competitors in order to commission and operate the new Songo Songo processing facility. Throughout the year downtime was experienced at the Kinyerzia and Ubungo power plants too due to commissioning, repairs, maintenance and overhaul works. As a result they were operating below maximum generation capacity. All major works were completed by the year-end.

During the year work continued on the expansion of the processing facilities at Msimbati and it is expected to be commissioned and fully operational during the first half of 2017. Primary processing of the gas is required at Msimbati to knock out free liquids before the gas enters the sub marine pipeline that connects the Madimba GPF. The expansion of these facilities completed all the necessary field infrastructure work to enable the delivery of up to 130MMScf per day to the Madimba processing facility. When combined with the five existing wells, with an average production rate of 20MMscf/d per well, the concession will be able to deliver significantly higher volumes of gas without the need for any more capex.

The pre-tax loss of the Mozambique operations was $395K, an improvement of $243K when compared to last year. The group received government approval of a two year appraisal programme for the Tembo gas discovery and increasing their interest from 12% to 85%. They have completed reprocessing of about 1,000km of 1984/1985 vibroseis data which represents all the existing regional seismic over the Tembo appraisal area. They have also finalised the design details of a new 2D seismic survey of about 700km data. This will further their ability to identify a suitable appraisal location for a well in 2018.

It is expected that the work programme will be funded through a combination of internally generated cash flows and a possible addition of one or more industry partners.

As of the year-end the Mnazi Bay partners were owed thirteen months of invoices for gas sales made to TANESCO with $2.2M owed to the group, $488K of which was received after the year-end. In addition, two months of invoices worth $3.2M were outstanding from TPDC, $1.5M of which was paid after the year-end. Receivables of $1.3M for filling and packing the transnational pipeline during Q3 2015 were also outstanding but $877K was paid after the year-end and they expect to receive the full payment in 2017.

In addition to the receivables for current gas sales to TPDC, a long-term receivable of $27.2M is due. The group currently receives a significant proportion of TPDC’s share of gas sales to reduce the receivable but there is a risk that future production may not be sufficient to settle the receivable, although the group expect it to be paid by Q2 2018. Also a long-term receivable of $6.5M relating to their disposal of transmission and distribution assets is receivable from TANESCO.

The group has payables of $16.8M due within the year consisting of $8.7M of trade payables, $6.9M of loans and $1.3M of other liabilities. To counteract this, the current portion of the TPDC receivable stands at $12.3M. In February 2017 the group made some amendments to the repayment of their credit facility. They need to repay $3.3M this year followed by $5M in 2018, $6.7M on 2019 and $1.7M in 2020 with the terms of the facility being extended by a year. There is also $4M outstanding on the other credit facility with $2M due for payment in 2017 and $2M in 2018. At the year-end the group had just $980K of cash on hand.

The Tanzanian government published a new finance bill that came into effect in July 2016. It introduces measures aimed at reducing tax evasion and plugging loop holes for tax avoidance, to create new sources of revenue in order to increase revenue collection and to control unnecessary expenditure. The bill introduces a number of changes to the tax regime which impacts the oil and gas sector. The group has ongoing discussions with industry participants and the TRA to better understand how these new changes will impact them.

Going forward the group expect gas sales to average between 40 and 50MMScf per day during 2017 and the working capital facility combined with the proceeds from gas sales to TPDC are expected to be sufficient to meet existing near term obligations. As there was a loss this year the PE ratio will be meaningless. The group is also forecast to make a small loss in 2017 too.

Overall then this has been a decent year but one that did not turn out as well as expected. The pre-tax loss improved when compared to last year due to the full benefit of gas sales to the new pipeline and there was some operating cash generated (as opposed to consumed in 2015). This was nowhere near enough to cover capex, however, and net assets also declined. The group seems to have a bit of a precarious cash position and a lot of payables due shortly so hopefully there are no more surprises this year.

The main issue is that they planned for sales of between 70-80mmscf/d but only got 43. The reasons for this are the ongoing Symbion power plant dispute which shows no sign of resolution, the fact the government used a competitor’s gas instead of those, I am not sure if this is an ongoing issue, and some downtime in the other power plants which have now been rectified. This coming year they are only expecting between 40 and 50mmscf/d which is unlikely to be enough to radically alter the fortunes of the group. I am not rushing in to buy here quite yet.

On the 10th April the group released an operational update. Demand for the gas from Mnazi Bay is firming up with current gross volumes being maintained within the previously guided range and Q1 production averaging 43MMscf/d. As expected, TPDC started gas delivery to a new industrial customer, Goodwill Tile Factory, in the quarter with further demand growth from the industrial sector expected to increase as Dangote Cement begins using gas for power generation.

So far this year TPDC has settled the November and December invoices that were outstanding at the year-end and has also settled a 2015 invoice for line fill gas volumes. In addition, they have received payment from Tanesco for five months of outstanding invoices. Combined cash receipts totalling $4.9M have been used primarily to settle outstanding amounts that were due to the operator.

In Mozambique the group have completed the reprocessing of about 1,000km of existing seismic data, interpretation is being finalised and results from the discovery well have been fully analysed. They are now working on advancing a farm out process with a view to securing an industry partner to jointly drill an appraisal well in 2018.

On the 16th May the group announced its intention to conduct a private placement with institutional investors and certain existing shareholders to raise gross proceeds of about $5.5M through the issue of up to 16,953,496 new shares at a price of 25p per share, a discount of 7.7%. The new shares represent about 10% of the issued share capital and the proceeds will be used in order to advance the Tembo appraisal programme in Mozambique as well as provide general working capital.