Central Asia Metals has now released its interim results for the year ending 2015.

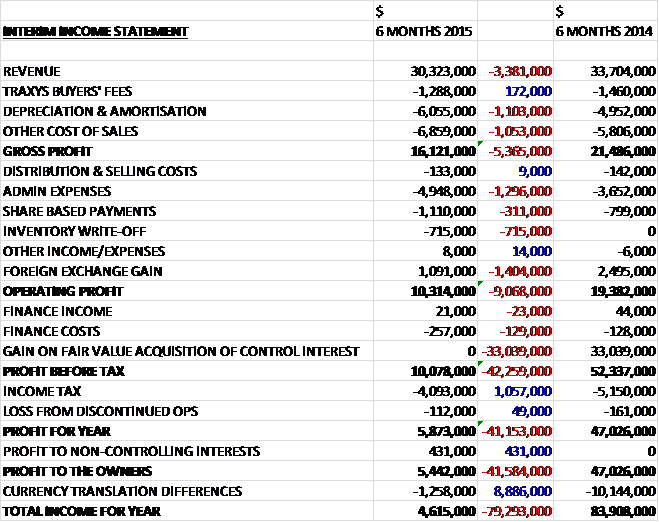

Revenues fell by $3.4M when compared to the first half of last year and both depreciation and other cost of sales increased year on year to give a gross profit some $5.4M lower. Admin expenses increased by $1.3M, the foreign exchange gain was $1.4M lower than last time and there was a $715K inventory write-off so that operating profit fell by $9.1M. There was no gain on the fair value acquisition of the acquired assets but tax was somewhat lower to give a profit attributable to the owners of $5.4M, a decline of $41.6M year on year.

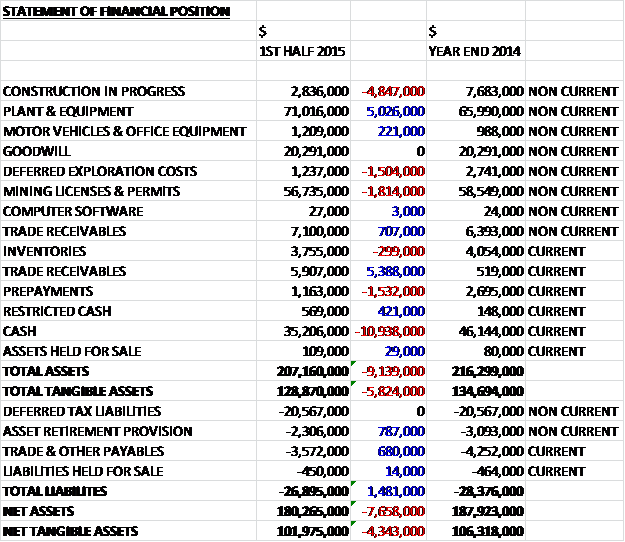

When compared to the end point of last year, total assets fell by $9.1M driven by a $10.9M decline in cash, a $4.8M fall in construction in progress, a $1.8M decrease in mining licenses and permits, a $1.5M fall in deferred exploration costs due to the re-measurement of the Copper Bay valuation and a $1.5M decline in prepayments, partially offset by a $5M increase in plant and equipment and a $5.4M growth in trade receivables as a result of $4.5M owed for the sale of copper for June deliveries which was received in early August. Total liabilities also fell during the half year due to a $787K fall in asset retirement provisions and a $680K decline in payables. The end result is a net tangible asset level of $102M, a decline of $4.3M over the last six months.

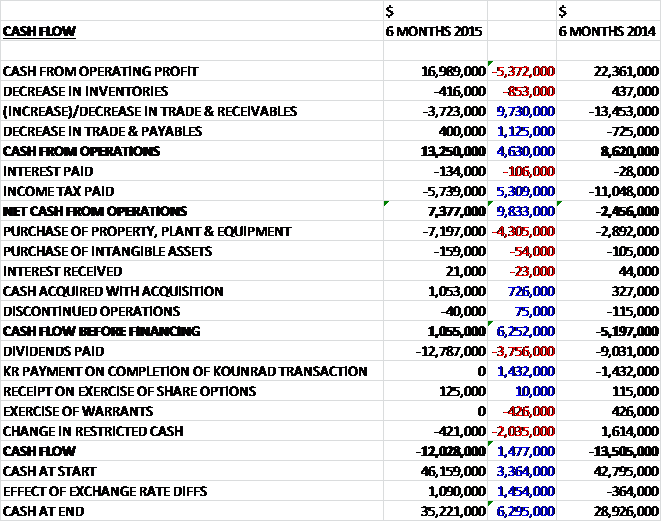

Before movements in working capital, cash profits fell by $5.4M to $17M. Although receivables did increase, they did so much less than during the first half of last year and we also see the amount of tax paid almost halve so that the net cash from operations came in at $7.4M compared to a net outflow of $2.5M at this point of last year. The group then spent all this cash on property, plant and equipment ($7.2M) and intangible assets ($159K) so there was not really any free cash. The group then paid out a lot in dividends so that the cash outflow for the period was $12M to give a cash level of $35.2M at the end of the first half of the year.

The total copper production in the first half of the year was 5,444 tonnes, an increase of 7% year on year. Total copper sales increased by 9% to 5,120 tonnes with an average price achieved being $5,936 per tonne compared to $7,049 per tonne in the same period of last year. Towards the end of August the copper prices had declined close to $5,000 per tonne. C1 cash cost of production was $0.75 per lb compared to $0.72 per lb in the first half of last year with the fully absorbed unit cost being $1.87 per lb. The guidance for the full year is now 12,000 tonnes of copper despite the incident reported previously.

The increase in copper production was largely due to the expanded boiler house capacity at the plant resulting in higher solution volume treatment rates during the winter months. As previously announced, an incident occurred on site towards the end of June which resulted in about a third of the organic inventory being lost to the dumps within a very short time frame. On inspection it was identified that the weir plate system had failed in the recently commissioned SX mixer settler, allowing some of the organic inventory to escape from the circuit via the raffinate system and on to the dumps.

The failure was rectified but the loss of inventory and the subsequent lead times to replace it resulted in the revision of the 2015 full year production target from 13,000 tonnes to 12,000 tonnes of copper. At the end of August all of the organic inventory had been replenished and the plant was gradually being ramped up to capacity levels. The incident cost a total of $700K arising from the write-off of the lost organic inventory. Shortly after the period-end the group experienced their first major accident on site. The accident resulted in injuries to two employees who are being given support to make a full recovery.

The extended SX-EW facility was commissioned ahead of schedule in May. The programme included construction works and equipment installation, all undertaken by company personnel. The extra mixer-settler tank has increased the plant’s solution treatment capacity by 33% to 1,200 cubic metres per hour, and the additional 24 electro-winning cells have increased the plant’s daily plating capability by 42% to 50 tonnes of copper. The infrastructure upgrade also included the installation of an additional 10MW transformer substation. The stage 1 expansion and additional 5.6MW boiler capacity installed towards the end of 2014 have increased the plant’s name plate capacity from 10,000 to 15,000 tonnes at a cost of approximately $13M against a budget of $15.5M. The application to the relevant authorities for the required permits to allow copper extraction from the Western dumps are in progress and approvals are expected to be received by the end of 2015. The stage 2 expansion therefore remains on track for production in 2017.

At the period-end, the group subscribed for 135,621,610 newly allotted shares in Copper Bay ltd for $3M which increased their shareholding from 50% to 75%. Following this investment, management has reconsidered the accounting treatment of the initial $3.2M investment in 2013 and have fully consolidated the Copper Bay group at historical cost. An intangible asset of $3.2M recognised in 2013 equal to the cash consideration paid for the initial 50% shareholding has been reduced by $1.6M. The feasibility study has now commenced and a project manager has been appointed. It will work towards providing more accuracy and confidence regarding all aspects of the project. In Mongolia, the group continues to hold for sale the assets it owns.

In May the company completed a court approved capital reduction scheme which resulted in $67.1M being transferred from the share premium account to distributable reserves. A condition of the capital reduction scheme was to set aside an amount into a restricted bank account which would cover certain creditors as of the effective date of the capital reduction. The balance of this restricted bank account is currently $400K.

At the year-end, non-current receivables included $7.1M relating to the amount owed to the group by the Kazakhstan government for VAT. The group is in the process of appealing to the authorities and the outcome may not be known until early 2016. A portion of the outstanding balance is being recovered through the offset of VAT liabilities on local sales of copper cathode.

After the period-end the Kazakhstan government transitioned to a free floating exchange rate of the KZT allowing the market to set the price. As a result during the month, the rate of the KZT depreciated approximately 37% compared to the end of the first half of the year. This will impact the results and net asset position in future reporting periods. For example, a 30% devaluation impact on the net assets of $73.5M denominated in KZT is a reduction of $22M. The immediate impact of the change is positive, however, as about 60% of the cost base is denominated in KZT and copper is mostly sold in USD.

At the current share price the shares yield an impressive 7.2% but this reduced to 5.2% on the full year prediction. There is no debt so the net cash currently stands at $35.8M compared to $46.3M at the end of last year.

Overall then this was a difficult period for the group. Profits declined, along with net assets and although operating cash flow improved year on year, this was only due to a smaller increase in receivables than last time and less tax paid with the underlying cash profits declining. Although both copper production and sales increased the reason for this sluggish performance is due to the average price obtained per tonne of copper falling from $7,049 to $5,936. What’s more, this has since fallen even further to about $5,000 per tonne. Also, the loss of some $700K-worth of organic inventory hasn’t helped.

Going forward, the increase in production enabled by the upgrade does bode well and with the feasibility study at Copper Bay starting, there could be some uplift from this too. The strong decline in the Kazakhstan currency should reduce costs but it will also reduce the value of the local assets so I am unsure as to the effect of this development. With a dividend yield of 5.2% there is some value offer at this high-quality producer but with the Copper price continuing to struggle with an uplift difficult to envisage at this time, I do not think I will be jumping in here just yet.

The chart still doesn’t look that inspiring.

The copper price chart certainly doesn’t – the recent recovery seems to have been short-lived.

On the 5th October the group released a production update covering Q3. Production in the year to date has reached 8,410 tonnes compared to 8,432 tonnes during the same period of last year; year to date sales were 7,699 tonnes compared to 7,055 tonnes and there was a record monthly copper output of 1,216 tonnes in September itself. Production in Q3 pf 2,966 tonnes was lower than the 3,337 tonnes produced in Q3 last year due to the operational incident which resulted in a quantity of the organic inventory being lost. The impact at Kounrad was temporary, however, and the plant returned to capacity in early September. The guidance for the year remains at 12,000 tonnes.

On the 23rd November the group announced that it has received the regulatory approvals required for the Stage 2 expansion programme of its Kounrad solvent extraction and electro-winning copper recovery project in Kazakhstan with the Ministry for Investment approving an amendment to the project’s existing subsoil use contract. This approval gives the group the right, under the law, to exploit the copper contained in the Western dumps. The procurement of materials and equipment for the programme is now underway with the capital cost remaining within the $19.5M estimate. The construction works are scheduled to start in March 2016 and will be executed primarily by company personnel.

The second part of the year has seen an overall increase in production volumes and a record monthly production of 1,285 tonnes of copper has been achieved in October. This increase, together with an approximate 65% devaluation of the Kazakh Tenge against the dollar results in downward pressure on the unit cost of production which is lucky given the fall in the price of copper over recent weeks.

On the 8th December the group announced that Roger Davey had been appointed as a non-executive director. He has over 35 years’ experience in the international mining industry and is also non-executive director of a number of other companies in the sector such as Atalaya Mining, Orosur Mining and Condor Gold. Until 2010, he was Senior Mining Engineer at N M Rothschild.

On the 6th January the group released a 2015 production update. During Q4 the group produced 3,661 tonnes of copper compared to 2,701 tonnes in Q4 last year, which brings the total production for the year to 12,071 tonnes, an increase of 8.4% year on year. They sold 12,040 tonnes of copper cathode during the year, an increase of 880 tonnes. These sales were predominantly through off-take arrangements with Traxys, which has been retained as the group’s offtake partner through to the end of 2018 with terms that provide some cost savings. As of the end of the year, the group’s cash position was $42M.

In H1, the C1 cash cost was $0.74 per pound and for the full year this is expected to be between $0.65 and $0.70 with the reduction due to efficiency improvements, increased copper production and the devaluation of the local currency. The company is confident that 2016 C1 cash costs will be maintained within the 2015 guidance range of $0.65 and $0.70 per pound.

The company is now targeting increased copper production for 2016 to between 13,000 and 14,000 tonnes. Consistent monitoring and analysis of the copper leaching rate since production started in 2012 indicates that the recovery of copper from the dumps is taking slightly longer than originally projected but the company remains confident of producing the same total tonnage of copper from the Kounrad resource as previously estimated, thereby extending the life of the operation beyond 2030.

The SX-EW plant’s increased nominal capacity of 15,000 tonnes per annum is predicted on two inputs: the throughput of volume of pregnant leach solution to the plant from the dumps, and the grade of copper within the solution. The plant is now capable of handling up to 1,200m cubed of PLS per hour and this throughput was achieved in Q3 but due to the seasonal temperature variations at the site, the average annualised throughput is estimated at about 80% of design.

The combination of a longer leaching cycle, seasonal variations to the volume of PLS and a stabilisation of the long run PLS grade means that he company believes a production guidance range of between 13,000 and 14,000 tonnes of copper cathode is more appropriate to ensure sustained production over an extended period.

The cost discipline combined with the weakening of the Kazakh Tenge means that the board are condfident that they can continue to generate positive cashflows from the operations at Kounrad despite the current market headwinds which have seen copper prices drop to a six year low. The dividend policy of returning a minimum of the 20% of the annual gross revenues to shareholders therefore remains in place.

As previously noted, this is no doubt a quality outfit and one that I would normally wish to own shares in, but the recent collapse in the price of copper makes me reluctant to jump in here.