Safestyle has now released its interim results for the year ending 2015.

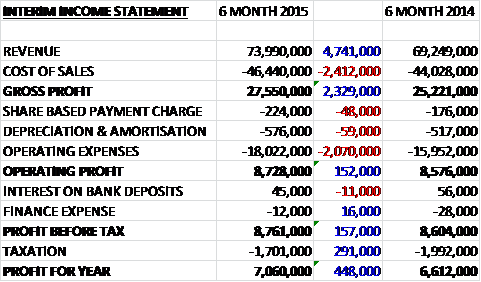

When compared to last year, revenues increased by £4.7M and after an increase in cost of sales, gross profit was some £2.3M ahead. Operating expenses also increased, mainly as a result of an increased spend on TV and digital marketing, and a small fall in bank interest received was broadly counteracted by a fall in finance expenses so profit before tax was £157K higher which, after a decline in tax, meant that the profit for the half year came in at £7.1M, a growth of £448K year on year.

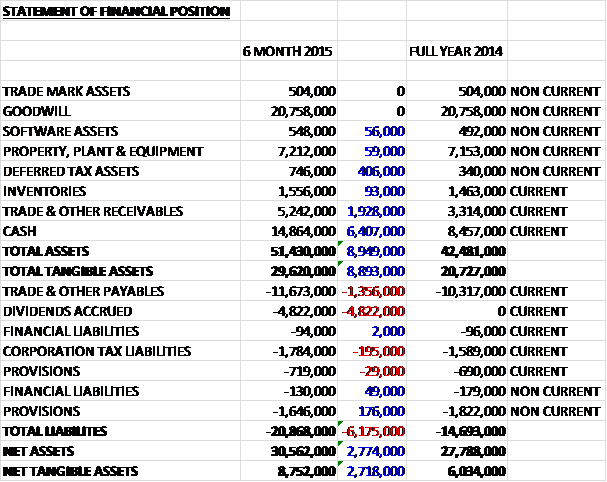

When compared to the end of last year, total assets increased by £8.9M driven by a £6.4M growth in cash levels, a £1.9M increase in receivables and a £406K increase in deferred tax assets. Liabilities also grew over the past six months due to a £4.8M dividend accrual and a £1.4M growth in payables. The end result is a net tangible asset level of £8.8M, an increase of £2.7M over the past half year.

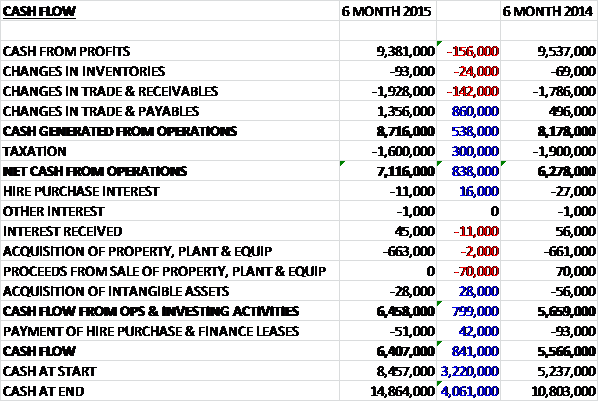

Before movements in working capital, cash profits fell by £156K to £9.4M when compared to the first half of last year. An increase in receivables was not entirely offset by a growth in payables, which was higher than last year and after a slightly lower tax payment, the net cash from operations came in at £7.1M, a growth of £838K when compared to the first half of 2014. There was not much in the way of capital expenditure, with the £663K spent being very similar to last time and relating to the investment in manufacturing equipment as part of the five year programme, along with £28K spent on intangible assets, half that of the first half of 2014. The cash flow for the period as a whole was an impressive £6.4M to give a cash level of £14.9M.

The market in which the group operates contracted by another 10.1% by volume during the first half, with further deterioration evident in July and August. These figures are rather surprising given the generally favourable consumer economic conditions and the order trends seen with Safestyle and I have to say I am a bit sceptical.

The group’s enhanced range of consumer finance offerings are proving to be attractive to their customers and provides a competitive advantage that helps the group increase market share, up from 8.5% to 9.5% in the period. This does have a knock-on effect of increasing costs and therefore reducing gross market for the year as a whole, however. In addition, they have invested in additional marketing expenditure during the period and it is expected that this increase in advertising commitment to continue in the second half.

The conservatory refurb programme was launched in April and early order intake was apparently encouraging, with installations increasing in volume in the second half. It is expected that this product will support growth next year, contributing for a full year.

The total volume of frames installed increased by 3.8% to 141,712. Leads generated from media and online marketing grew by 12% and the average unit sales price was up 2.8% to £517. The price list increase implemented at the start of the year was secured, with the frame prices increasing steadily through the first half of the year as the 2014 order book was installed. As well as an increase in prices and volumes, gross margin also improved during the period due to the price increase and a reduction in PVCu costs as a result of lower resin prices which was partially counteracted by the introduction of mandatory insurance backed guarantees in June 2014, the increase in glass prices from August 2014 and the increased subsidy costs as a result of the continued transition to promotional finance offers.

During the period the group opened a new sales branch in Watford. Order intake since the period end has been buoyant, aided by the improved customer finance offer which was launched in June, and the recently introduced conservatory upgrade product which is gaining momentum. The board remain confident of delivering a year outturn in line with market expectations and expect the market contraction to slow.

After a 9.7% increase in the interim dividend, at the current share price, the shares yield 3.6% which increases to 4.2% on the full year forecast. At the period end, the group had a cash position of £14.9M, an increase of £6.4M during the period.

Overall then this was a decent half year for the group. Profits were up, net assets increased and operating cash flow grew year on year, but this was only due to the larger increase in payables than large time and cash profits actually fell. The group did generate copious amounts of free cash, however. Despite the market contracting by 10%, Safestyle increased both volumes and price per frame and going forward the consumer finance offering along with the new conservatory refurb business is expected to drive further growth. With not debt and a full year forecasted yield of 4.2% this looks like a decent investment to me.

On the 22nd October the group announced that it has issued 2,367,143 shares following the exercise by Zeus Capital of its warrant over new shares in the company granted at the time of the IPO. The warrants have an exercise price of £1 per share and as a result of the exercise, the company will receive cash proceeds of nearly £2.4M. The total number of shares in issue will now be 80,242,143.

On the 9th November it was announced that CEO Steve Birmingham purchased 40,000 shares at a value of £87.3K and now owns 4.9% of the company. The share price had been slipping a bit recently so this looks to be timed to try and halt that – still, a nice vote of confidence from the top man.

On the 25th January the group released a year-end trading update. The company has continued to trade well, with revenue for the year increasing 9.5% to £148.9M. In addition, pre-tax profit has shown good progress and is expected to be in line with consensus market expectations of £17.6M as the expected strong performance in the second half of the year saw double digit growth in both sales and profit.

Against the backdrop of a weaker market in 2015, the rollout of the group’s enhanced consumer finance offer helped to drive growth in the year, particularly in the second half. As expected, operating margins will show some decline in H2 as a result of the additional subsidy costs related to this offer, however. They have continued to increase market share, up from 8.48% at the end of 2014 to 9.46% at the end of last year within an overall market that contracted by 6.6%.

The number of installations increase 4.3% to 60,134 and the order book at the year-end was up 1.2% on the prior year. The board have seen a strong start to 2016 and they are confident of building on the progress made in the last year.

Overall then, this seems like a strong update although the order book growth does seem quite modest. I will continue to hold.